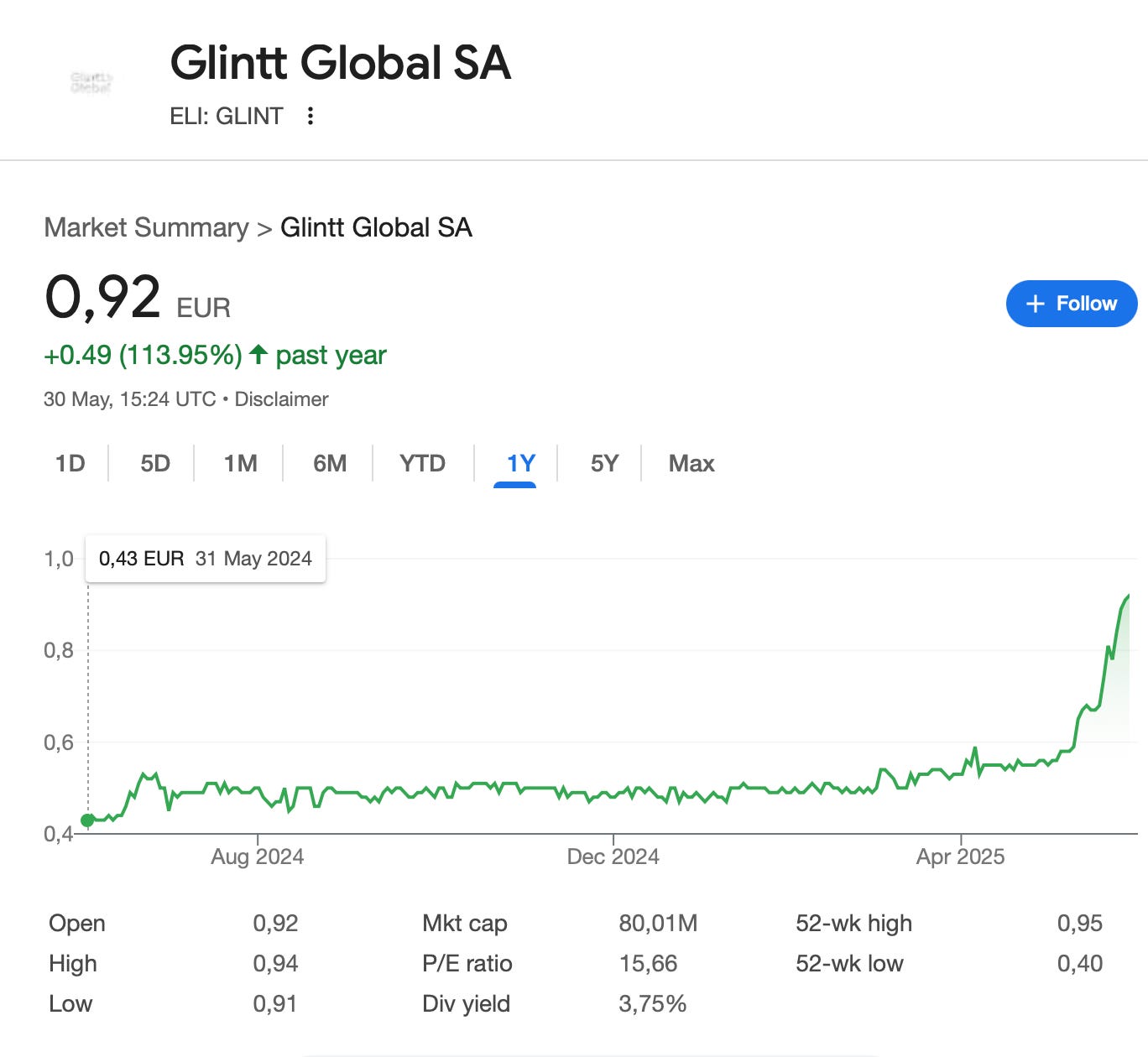

Update on Glintt after +143%

Glintt was my Portuguese pick and it’s now up over 143% + dividends in my portfolio. The stock price was growing slowly because I kept the name private for my subscribers, and there was no hype - no fintwit, nothing.

But another newsletter discovered the company in May, and I guess enough people discovered the stock, so it went up. This, along with good results. It really shows the hype cycle in some small caps. But it could be due to Portuguese retail buyers, I don’t really know.

This is the kind of value you can find in my premium portfolio.

If you do the work to:

look at more stock markets

more countries

more companies,

You do find sometimes some crazy value. Not all with the same results, but some. Glintt joins the baggers list.

Glintt pitch was a IT service and software company in the healthcare sector.

The valuation was attractive. The sector is more defensive than the rest of the industry.

P/S 0.35

P/FCF 5

EV/EBITDA (4.5)

it was a no-brainer.

The problem: What should I do when there is a high and fast price rise? Hold or fold? Historically I have been keeping some outperformers like Terravest (+467%) because..something good may happen with good management. And also taxes. Taxes are a big reason.

I also Kept Newlat (+250%) due to still low valuation. But often, the next place for new capital is new undervalued ideas.

But not all companies deserve this special treatment.

Here is the unlocked article below.

Before you click, in the intro I mentioned:

While it has not worked in the past two years, buying higher shareholder yields than the market yield is historically proven to outperform, so I keep repeating the process like an idiot.

This was more of a market anomaly due to inflation and sentiment than anything. Value always comes back, and I am expecting more to come back. Even without mentioning my paid subscription, I would encourage you to have a look at my public company thesis because there are still some with similar potential.

So Glintt is a IT service and healthcare service company from Portugal. It also does some pharmacy design in Portugal as it is a subsidiary of Farminveste, owned by the association of pharmacies in Portugal.

What I really want to see after this rerating is how recurring is the business? The company made 122 million euros revenue in 2024. Of which:

6.6 are sale of software licences

20.9 are sales of goods (Equipment and automation, physical design)

49.7 are services of implementation: it would mean new projects

32.2 are manutenção: It would mean maintenance.

Then we have 12.8 million of pharmacy remodelling.

Compared to 2023, it is almost exactly the same sector ventilation.

We can see that most of the sales are “Mercado Interno” or Portugal. There is a big opportunity in Spain, as Spain has 4 times the Portuguese population.

Services are also broken down between healthcare (61 million), and others (27 million). Within healthcare, its very diverse also, with Support services, Healthcare solutions, Equipment and automation, Physical design, Farmatools).

Ultimately we do not learn too much about the recurring and growth nature of the company, and there is very little information online.

The 2024 results

The profit is 5 million of Euros - 25% up.

But the sales were quasi flat at 122 million.

What improved the bottom line is a lower tax rate, exceptionally high in 2023 at 40%.

The 2025 Q1 results:

We saw a good increase in revenue with an increase in national sales of 9.3%, but also international sales of 22.6%, where there is more potential. It was mostly due to Spain where the growth was in all areas.

The next profit increased 23% to 1.8 million Euros.

They conducted a small acquisition: Prologica, a company focused on healthcare and data. However, the revenue is only 0.6 million Euros. But: The acquisitions are used to cross sell competencies, not just to add revenue.

In 2025 they have integrated CS&M inside of Glintt life, which is not an acquisition but an integration of a previously acquired technology. It will allow to create the biggest pharmacy software distributor in Spain and offer better services.

Glintt is heavily innovating in R&D with several projects.

Valuation

In terms of 2024 Free cash flow we are now at 10 times free cash flow as I have calculated 7 to 8 million in Free cash flow versus a 80 million Euros market cap.

In terms of Price to sales it is 0.65

Main risks listed by the company

Competition with new products.

No adoption of the new service platform for hospitals. I actually view that as a positive as it shows that the products have new features constantly, meaning a need to upgrade for clients.

A quite saturated portugese market, as they mention, with limited growth. Spain will be key for future growth.

Delayed decision making by clients on ordering.

Market and Perspectives

We know that the healthcare IT spending in Portugal and Spain is large (However it’s difficult to find information about it online, as the articles mix up different non related products under Healthcare IT). There are big opportunities in Spain (four times the population of Portugal) and a focus on Latin America where they “are convinced that our technology can help them”:

AI implementation would also be a tailwind.

The will be increased strain on services caused by the aging of the population in Spain and Portugal.

For 2025 - Glintt expects to increase sales, EBITDA and net profit. They are looking at acquisitions (mostly Spain) due to their good debt ratios.

By my own calculations, their net debt to EBITDA is 2.5, which is not that good. I would prefer that to go lower as not all their business is recurring.

Glintt announced an increased dividend to 0,04 Euros, or a 5.4% yield now or a more than 12% yield on cost for me.

Conclusion

I would not call the company a buy now. I would hold and stay attentive to new acquisitions, or a higher valuation. I think that the company needs better reporting with more details as well.

For buys, there are better options out there, I go for either deeper value or higher quality. For this, I refer to my past articles and portfolio reviews. (the 6 month portfolio review coming soon).

Meanwhile, I will keep looking for deep value or cheap growth.

Please share the work:

Subscribe or upgrade:

Thanks