Tensquare Games: Let's go fishing

Quick value article

<10X P/E mobile game developer with sticky games catalogue, pipeline, and large dividend. But uncertainty on future game success and management not fully aligned with shareholders.

Hello, let’s first talk about the market. The benefits of geographic diversification for European investors are really showing in this energy crisis. But a good European portfolio can still do fine over the long term as long as the companies are strong and growing. I find many opportunities at the moment and even some in the USA, I think that this has to stay our main focus. I find some through fintwit/substack and some from my monthly reviews of watchlists.

This is a mobile games developer out of Poland. Usually when I see mobile games developers I am cautious because these things come and go out of fashion. However, Tensquare Games has some advantages in this regard.

It looks like I became a growth bros but when we will go to the valuation part, you will see that I am a value brother that likes cheap growth. Un frère de la valeur.

History & Business overview

The company was founded in 2011, “from a 3-person project in a 10-square-metre room back in 2011 in the country’s leading university city and innovation hub Wrocław”. It started with “let’s fish”. There was “Wild hunt” in 2017, but the sales only took of with “Fishing clash” released in 2017.

It got listed in 2018.

Then in 2020 they released “Hunting clash”.

in 2021 they acquired RORTOS, an Italian flight simulator company for mobile phones. This is under the idea that the “Investment hypothesis assumes that flight simulator segment has significant potential comparable to fishing and hunting”. So far this is not the case but we will see. The price paid was not particularly cheap.

They acquired 25% of Gamesture in 2022, a company making RPG like games.

But if you look at the plans for 2022 on that chart, already two games are cancelled: Football Elite and Magical District. So it’s not like we can expect huge growth just by adding games. It does not work like way and the games have to be successful.

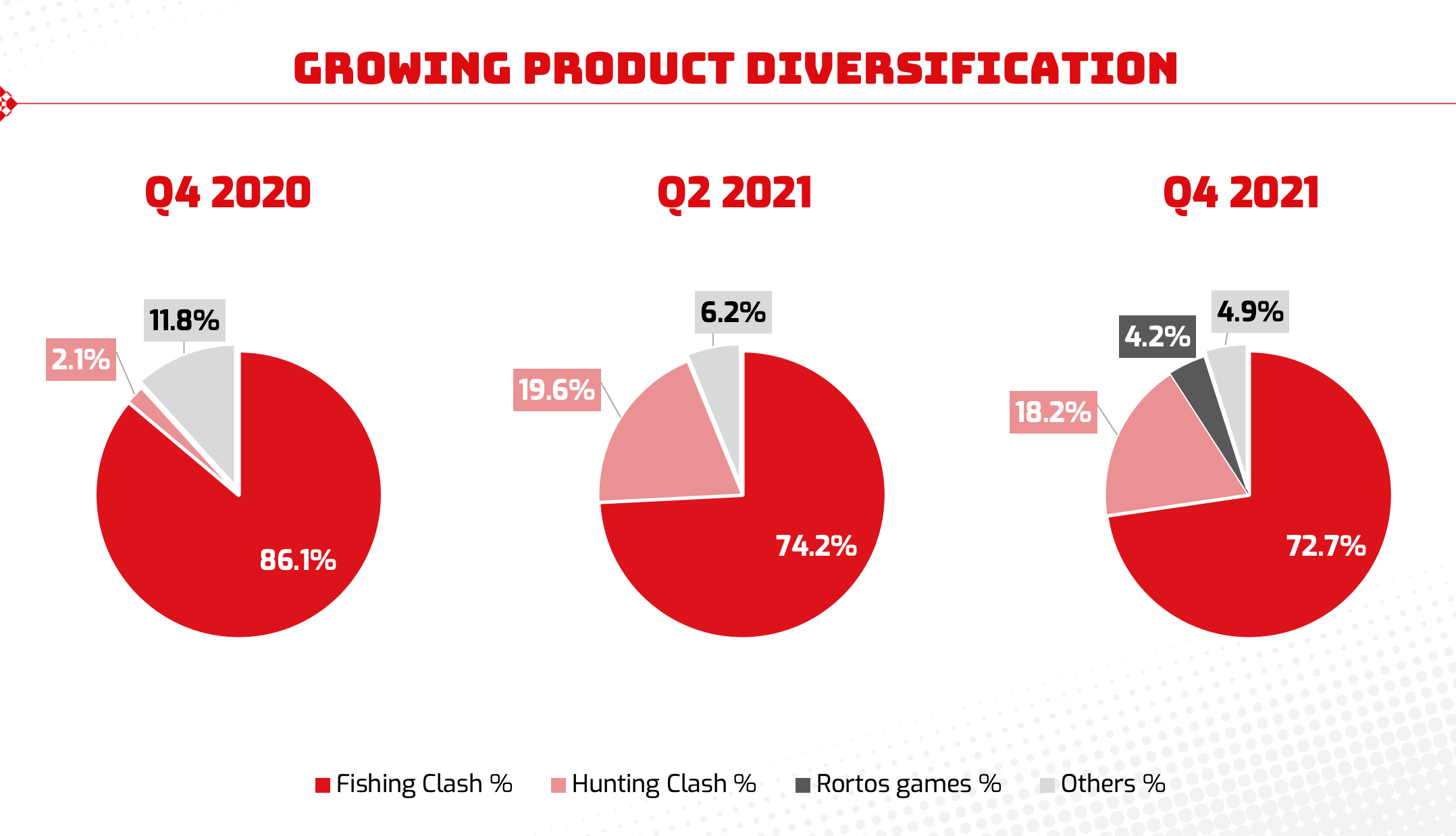

So the company derives 85% of profits from two games and 65% from one game.

Fishing clash.

Then comes Hunting clash.

Both of these games are free to play but you need to pay to get the best scores and features. The ARPU is between 2.3 and 3 USD per month with is reasonable, however it does not tell if its people stopping at level 2 of the game and giving up, or if they can get to a good level with these 3 USD. I haven’t tried the games.

They have some profit from two old games (let’s fish and wild hunt).

Then they have some profit from recently acquired games Rortos, which does Airplane simulators, but it is minimal.

The good thing about Hunting, Fishing and Airplane simulations is that they do not really go out of fashion and they are not a story game that you finish and stop playing. They are casual games that you can replay for years, which in theory should make for a growing profit stream as you add new games to your catalogues while the old games still generate sales. The problem is as they are pay to play games, the replayablity decreases as some players just give up and realise how much they have spent (app store reviews).

Fishing clash performance:

The launch of Fishing Clash in China has started. Apparently, China has many different app stores, so they are launching them one by one, since they need to get the app listed with the provider. The main one has been Huawei. Financial results are not showing great yet according to the company, despite over 4 million downloads and being in the top three in the sports category.

We can also use google trends to follow…the trends.

It shows a clear growth path, a covid boost, and a decreased following this, a slump in Q1-Q2 and a sort of rebound/stabilization recently.

Hunting clash performance:

Booking for these two games decreased further in Q2 overall but stabilized towards the end of Q2.

It shows that it is stable in 2022 after a drop in interest in Q1.

What is also interesting, is that their first game produced in 2011 still produces some profits. This is because Fishing or Hunting or Card games are timeless.

Strategy

Like any game developer the strategy is to put out new games, as well as put out new features to keep the existing games growing.

Many of the new games they develop end up being shelved or kept in the store but without marketing. This is because they do not take off. Most actually except Hunting Clash failed.

The acquisition strategy recently done does not move the needle in terms of profits, so either it is desperate, or they expect the acquired studio to have a huge success in a new game, notably Wings Heroes, a WW2 dogfight simulator.

Management

The company is 35% founder owned, but they don’t have control of the operations. They vote and one of the founders still sits on the board.

The CEO is Maciej Zużałek, joined in 2020 coming from a Private equity background. I cannot really judge the management to say if they are good or not. The business is fairly simple to understand and I am sure they do. The strategy will be judged on its success.

The Management is getting paid with a generous incentive scheme, about 30% of net income, which is excessive in my opinion. Worse, they reduced the business incentive targets when the business slows down in order to get the bonuses? That much Greed is bad and also explain why the stock is hated.

Because, unlike some forgotten stocks, this one is hated. There is a message board on Bankier.pl with dozens of daily messages, while some other stocks that I own get one thread a month. I think it has to do with Tech always attracting Geeks and mainstream investors. Anyway, back to management, I do not understand how all this share bonuses is not upsetting the two founders with their 35% of votes.

Risks

The big risk is that no new game makes a significant profit, and the two main games just decline let’s say 5-10% a year in revenue and profits.

Another one is an expensive risky acquisition.

Valuation

Well, there is little to no debt, and it’s incredibly cheap based on 2021 earnings at 6 times and a 10% dividend yield.

However earnings have deteriorated in Q1 to 25 million PLN or 100 million annualised, and will drop a bit more in Q2 to maybe 20 million or 80 million annualised. The company did some cost cutting as well in Q2.

This business is very cash flow generative as capex is very little.

The market cap is 737 million PLN. So less then 10 times bad Q2 P/E ratio.

As most companies I review, doing the valuation work is very easy. Thinking about the future business developments is the hard part.

Conclusion

I like this opportunity, because it is really value, even based on the last earnings, but I do not own it. Why? Because there is a bit too much of business uncertainty. It could go either way. And like I said I find many other value opportunities that are more conservative. I will keep it in my watchlist. I would love to hear your thoughts on this company.

Adding a romantic African touch to my publication

Hehe! Did someone expect this? That’s a surprise!

I am adding an extra page to the website, which is dedicated to some South African craft items that I have available. The long story is available on the substack. But the short one is that I qualified as a tech entrepreneur and I tried to list on the Nasdaq with 0 revenues at 100 times Total addressable market but my IPO failed and I went bankrupt. Don’t worry, I will never spam you about this but may include a pic or a link at the bottom of an email.

Until next time, thanks for reading!

Written straight to the point, without fluff and all the essential questions addressed!