First a word on the markets. The markets are too cheap for value and way too expensive for darlings. Cheap valuations make no sense. So fellow value brothers and sisters, pound the table, back up the truck, hold the ship tight in rough seas. Focus on what the portfolio brings: earnings and dividends. When valuations make no sense, they balance each other out the next year or six months. We are in 2021 again.

Edit: See a comment for a correction on the dilution.

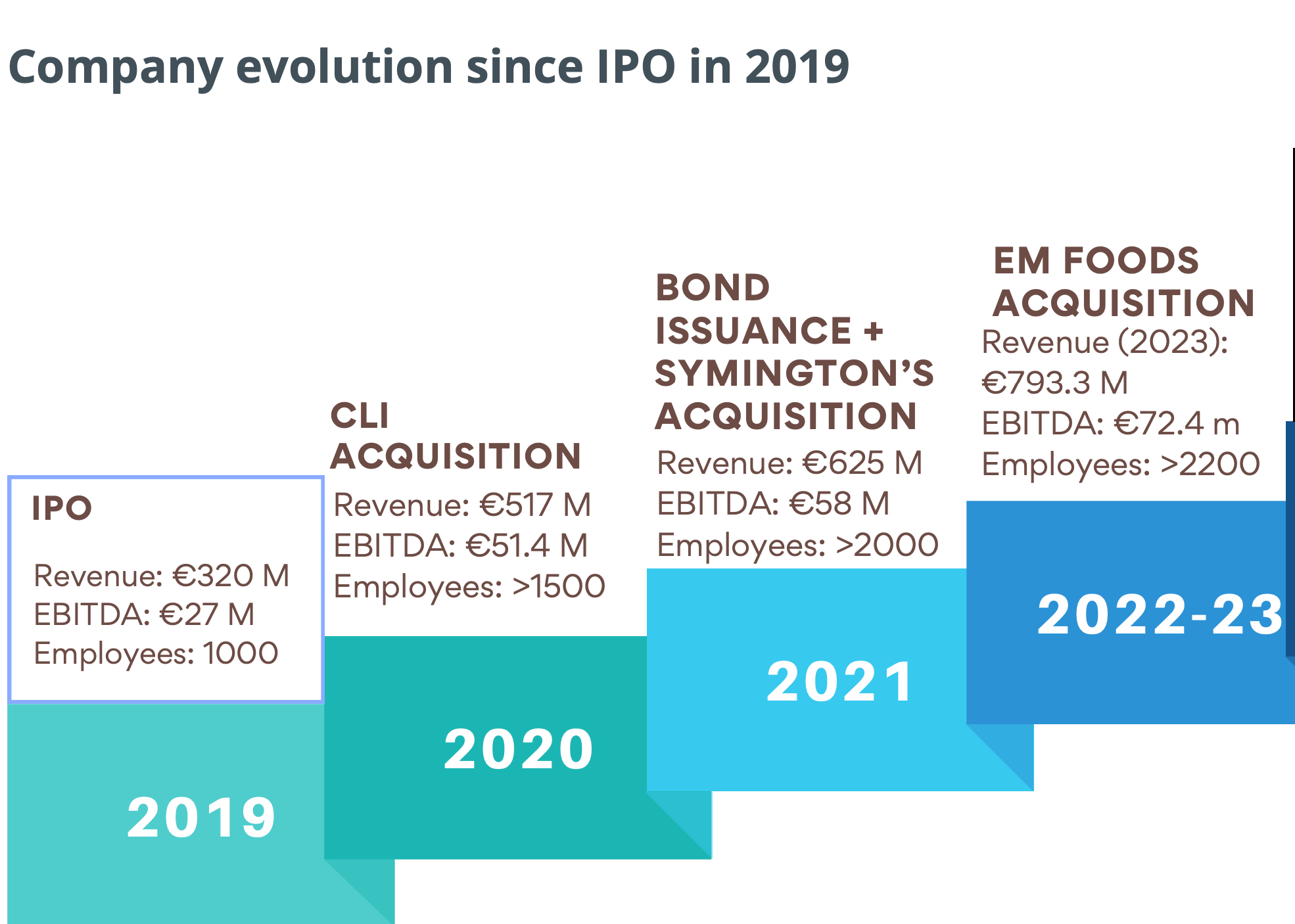

Newlat foods

Exchange: Milan

Stock price: 10.36

Market Cap: 445 millions.

EV/EBITDA 8.

Newlat food is an Italian food company that grows through acquisitions, repays debt and continues to acquire more.

I wrote it my last update in July that the company was trading at a P/FCF of 9 and had a war chest for acquisitions. Newlat has now pulled it’s most ambitious acquisition to date.

This propelled the stock from 6 to now 11. In this event and catalyst driven market, it is a bit strange that no one wanted a food company at a P/FCF of 9, but the price is now readjusting to bigger company with bigger earnings going forward.

Newlat is finaly acquiring Princes Limited.

Newlat made revenues of €793.3 million and EBITDA of 68.1 million. The business is highly cash generative with underlying free cash flow of 20 millions (despite heavy growth capex):

We can see below that there are growth investments indeed:

Newlat has proven an ability to grow from acquisitions and to get good commercial development and cost saving synergies in the past:

The acquisition

The company is buying Princes limited, a UK company with some let’s be honest So-So brands in “Canned foods, oils, Italian, fish, drinks”. These are not exciting brands, but they produce free cash flow.

The multiple paid is 7 times EV/EBITDA, funded by 650 million of Pounds in cash and 50 million of shares. The share dilution is an issue but was necessary for the acquisition, and is not massive. The rest will be funded by debt and existing cash.

The good advantage with food companies doing acquisitions, is that the Margins, even if relatively small, are stable across the cycle and avoid the cyclical debt blowup that an industrial acquirer can endure. The debt itself will bring the leverage to a quite elevated level, as the following extract from the press release states:

“Net Debt/EBITDA ratio of 3.28x, while the Net Debt/EBITDA ratio is expected to be below 2.5x at the end of current fiscal year”

There will be many synergies (at least 36 million) that I find interesting, like economies of scale, cross selling, and internalising the pasta production in Italy. But let’s ignore them for now.

The company will be called New Princes Group and will do 2.8 Billion Euros of revenue, 188 million of EBITDA and 31 million of Net Profit. Compared to the current market cap and will the dilution, it is not cheap on the net profit (already near 20 times) but the net profit is irrelevant with D&A of this acquisitive company.

The Operating cash flow minus maintenance capex is key here. The company expects an “annual Free Cash Flow of over € 100 million between 2024 and 2028”.

Valuation:

I have a new EV of approx 1180 million Euros post acquisition, including a market cap that I estimate at 560 million Euros post dilution.

The P/FCF would still be around 6, according to the company projected free cash flow of 100 million Euros per year.

EV/EBITDA makes it hard to clearly value companies across various industries, but it gives an indication.

The EBITDA pre synergies being 188 million, after the current rerating, EV EBITDA is still cheap at 6.5-7.

We have some upside with synergies and margin improvements.

Furthermore, as debt is paid down back to nearly zero, the EV will decrease by about 100 million every year, leading to further value creation, and a lower interest cost each year.

We can still have an upside over 3-4 years of at least 100% as debt is paid back, which would make the company a 4 bagger.

Risk:

There is some execution risk if the management teams clash between the UK and Italy.

Is it a buy now? Probably, but it was a clearer buy before the acquisition, because there is more execution risk than before.

The bottom line:

I am a deep value and Growth at a reasonable style investor.

I am open to other styles, and my analysis of quality investing podcasts and readings leads me to the conclusion: When companies are developing well operationally, we should not sell them in order to capture potential upsides (It is true that it is more valid for top quality companies). Selling winners too early is also a mistake.

So I don’t plan to sell Newlat and will see how they develop, and hold for the long term.

After a few years of deleveraging, there will be a time for further acquisitions to reach 5 billion euros of revenues.

If you want to discover more value ideas, please consider the premium membership.

Supporting the publication gives access to:

Over 25 write ups

Full portfolio with diversified 50+ mostly EM/small value ideas with short pitches.

Watchtlists in Koyfin with over 200 Emerging and Hidden champions stocks (free with Koyfin).

Correction by "Stock Forester" on X. There will be No dilution. Even better.

"

Was looking at your NWL write-up and I also have been long quite some time.

I do think you made one critical error.

Newlat Group is selling some of their shares as part of the deal

To be clear: Newlat Group is the company owned by the Mastrolia family and the largest shareholder of Newlat Food.

Really like your investment style!

Yesterday, 1:55 PM

Oh thanks, so even better, no dilution right?

Yesterday, 3:30 PM

1 new message

Correct, no dilution for current shareholders.

The family will just hold a smaller portion. "