Hello all.

Another difficult week in the markets and in geopolitics. Meanwhile, we are still shareholders of businesses.

As a reminder, JD.com is one of the big e-commerce companies in China, with 700 million active customers and a market capitalisation of less than 40 billion USD!

But first, a word from our sponsor: Rebound Capital.

10 AI-proof SaaS Stocks for 2026

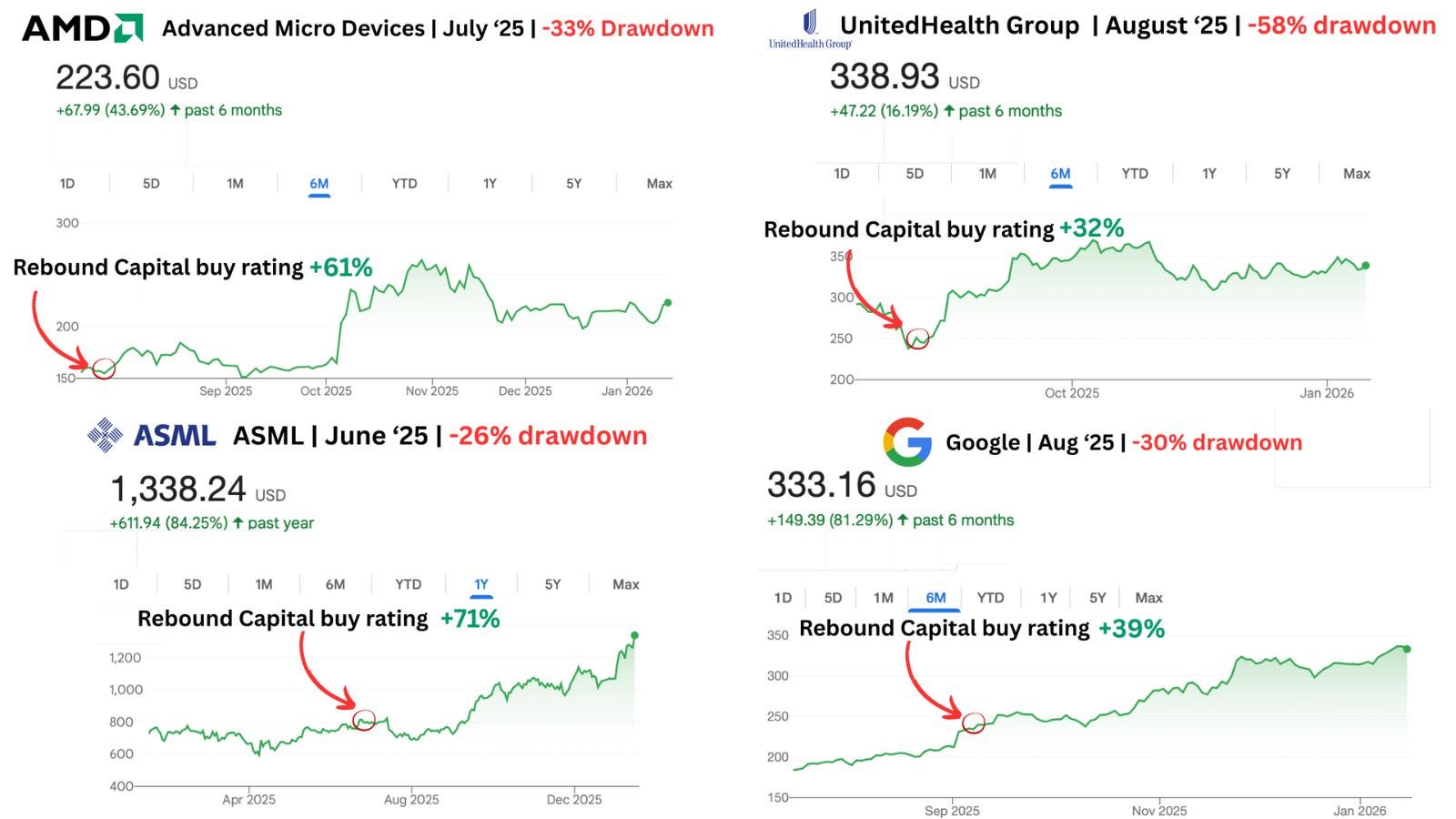

Meta once dropped 70%. Netflix: 50%. Amazon: 40%. Every investor had ruled them out, citing “the companies were done”.

But they all rebounded - Meta: 690%. Netflix: 540%. Amazon: 153%.

Every world-class company suffers deep drawdowns. Rebound Capital identifies high-quality companies undergoing drawdowns to capitalize on their eventual rebound.

Just last year, they identified ASML (up 58%), Google (up 40%), and AMD (up 61%) as ideal rebound prospects.

And now, SaaS is in peak pessimism due to AI-led disruption.

Rebound Capital has identified 10 AI-proof SaaS companies with deep moats in steep drawdowns.

Emerging Value readers can now unlock their exclusive 24-page AI-proof stock report for free!

Thanks for sponsoring Emerging value with adjacent research.

Back to JD.com:

Since I wrote up JD.com in summer, the Chinese e-commerce Giant has accelerated the food delivery war in China and has increased losses.

JD.com: scale economy shared

JD.com is a bit like a little Amazon in the Chinese e-commerce landscape.

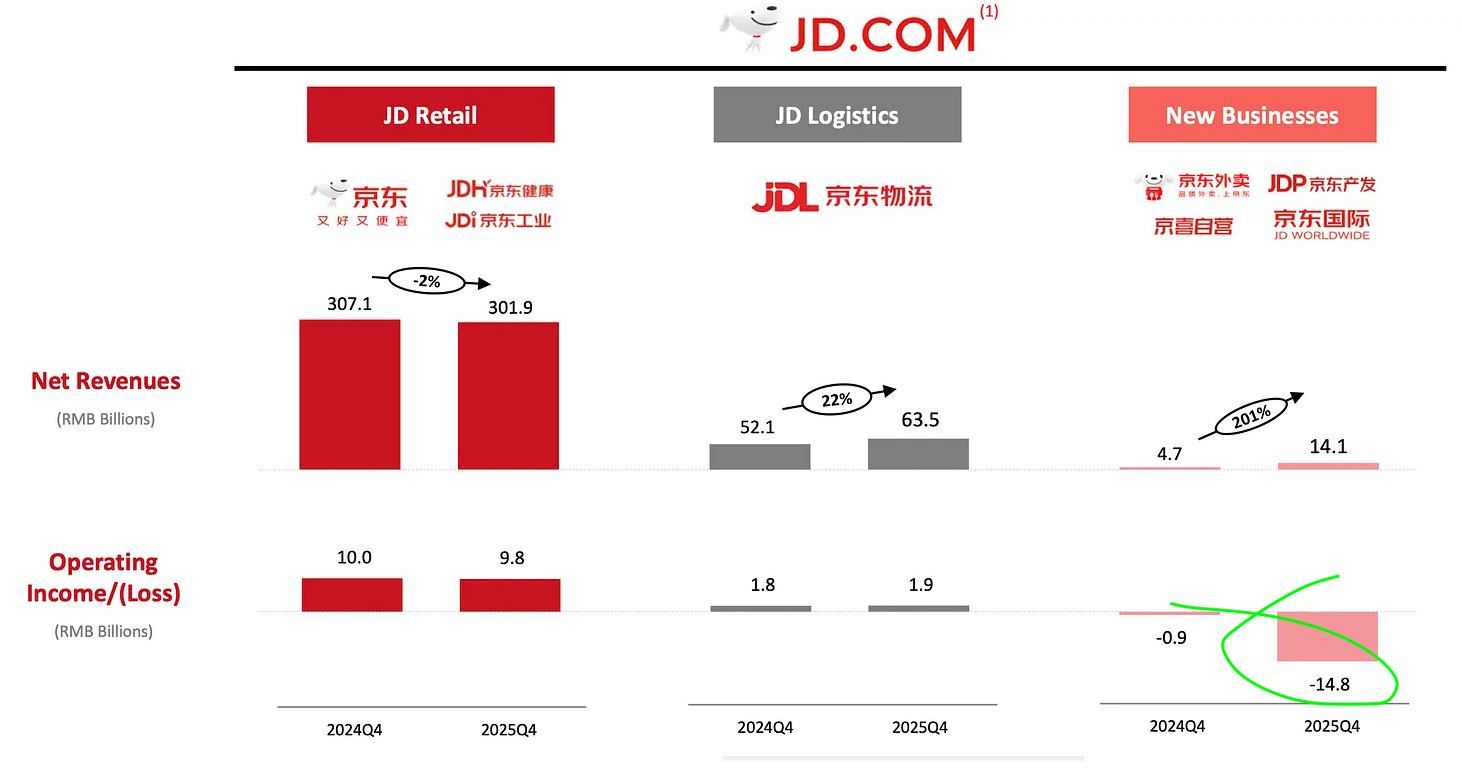

The JD core business keeps executing as normal.

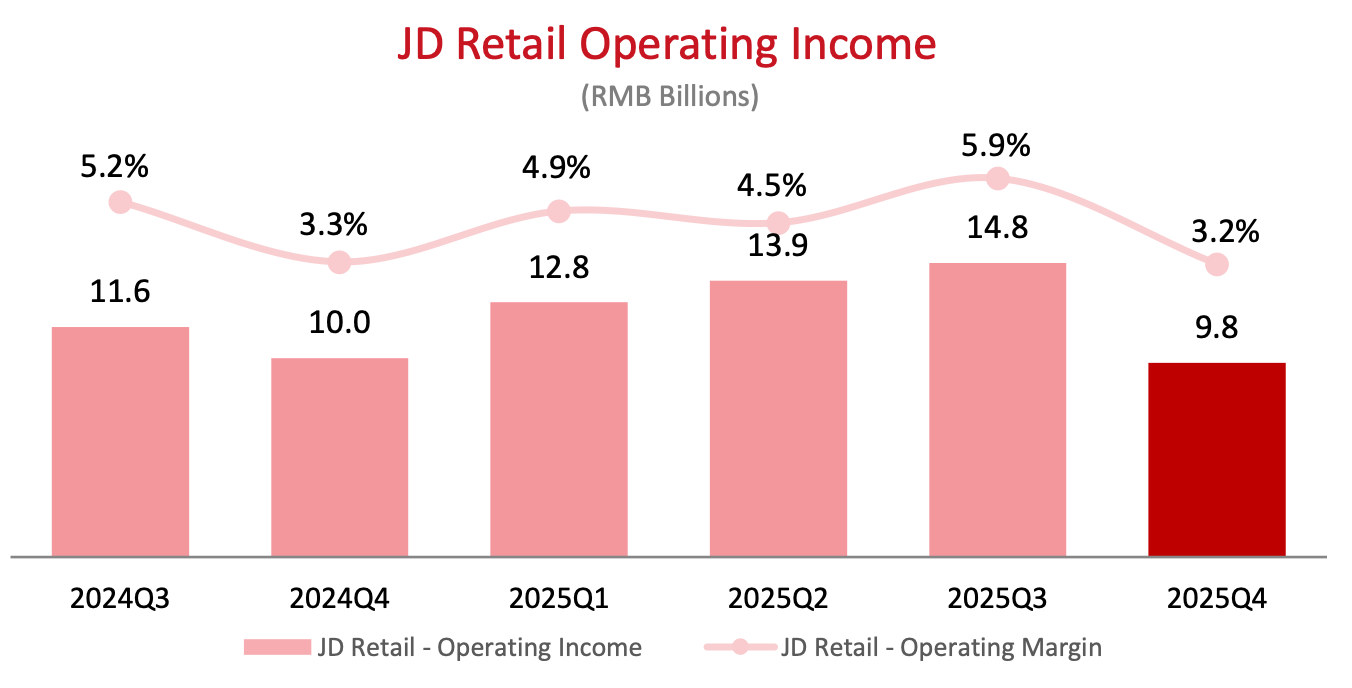

Q4 profits were null, as the new business (food delivery) caused major losses, compensating all the earnings from the rest of the business.

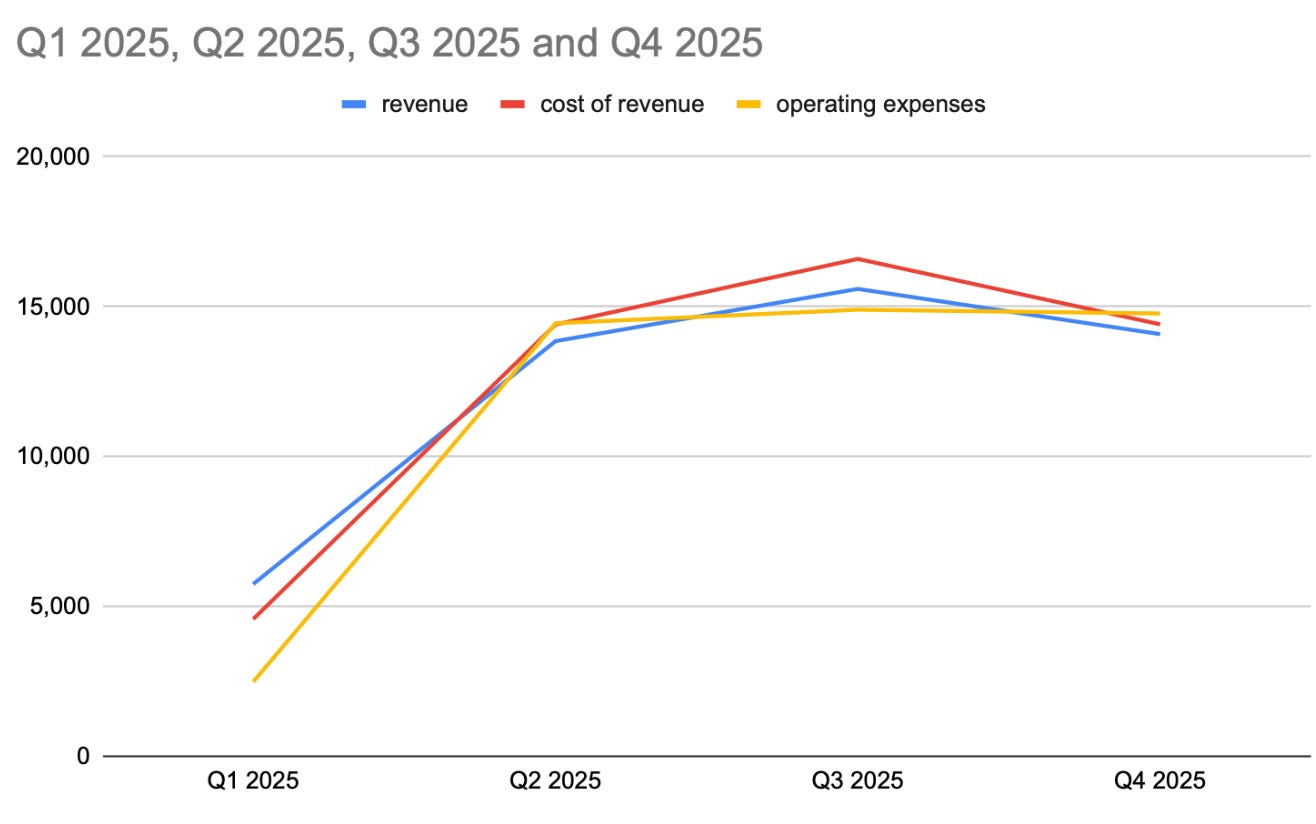

The food delivery business has losses equaling revenue, because of cost of revenues matching or exceeding revenue (selling items at a loss), combined with operating expenses equals to revenues.

New business

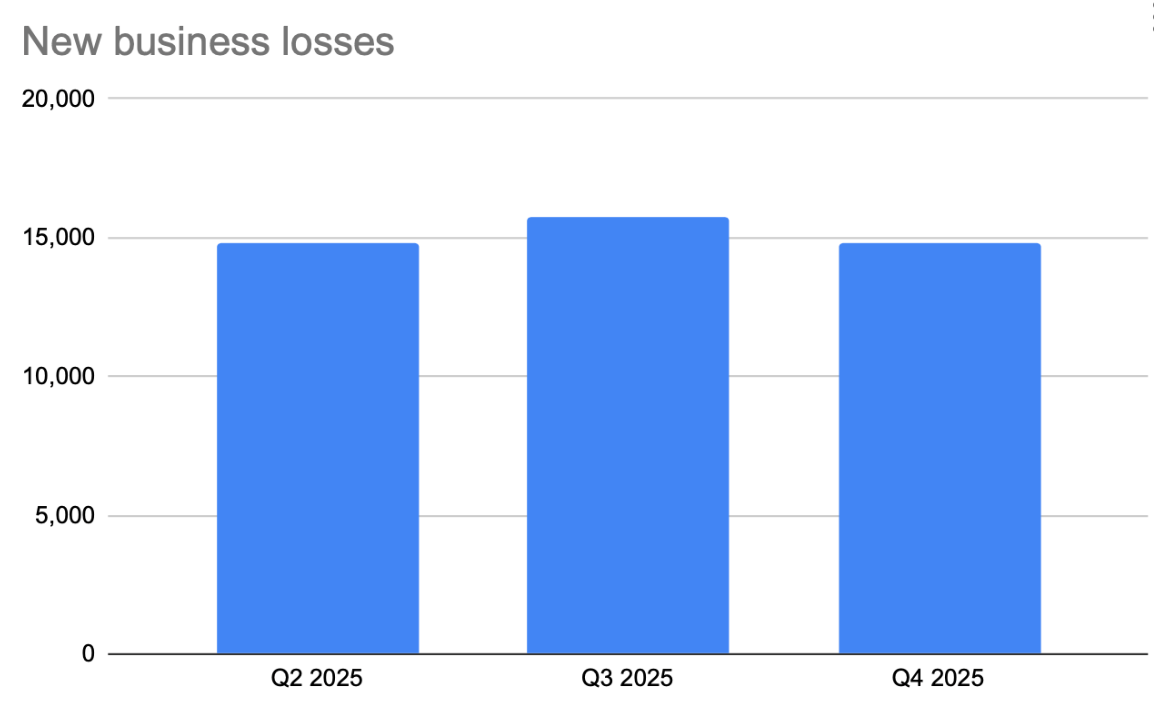

Contrary to what the management says, new business losses are not really narrowing, they decreased in Q4 but not compared to Q2.

While the management talks about loss reduction from the last quarter, it is an exageration as shown in the chart above. The reduction is insignificant.

The government stepped in in January 2026 to reduce unfair competition towards restaurants and shops: https://www.chinadaily.com.cn/a/202601/09/WS6960d0e7a310d6866eb32f68.html

The office highlighted that food delivery platforms have increasingly engaged in aggressive subsidy campaigns, price competition and traffic control practices, triggering widespread concern among businesses, workers and consumers.

These practices have intensified internal competition within the industry and placed pressure on brick-and-mortar merchants, it added.

The company says that food delivery investments will reduce next year.

Delivery will continue to prioritize healthy volume growth while improving its unit economics at a greater level. We expect investment efficiency in food delivery to improve further this year compared to 2025 levels.

JD communicated the 2026 targets for food delivery:

As we enter 2026, our priority for food delivery remains to drive healthy order volume while deepening synergies with our core retail business. We believe investment in food delivery has peaked in 2025 and will trend downward this year if market competition trends towards becoming more rational

Seriously? They have no idea if investment has peaked. I take a wait and see approach to 2026.

Looking at this year, 2026, we'll continue to strengthen our capabilities and onboard more quality merchants and products and enhance user experience. At the same time, we'll begin generating revenue through offering merchant services, achieving an orderly and rational monetization.

It remains to be proven. Over the long term, I am optimistic that this business will at least not lose money.

Active customers:

The yearly active customers grew a lot but it did not show much positive effect on JD retail:

Our totally active customers grew by 30% year-over-year in Q4, capping a year where we exceeded 700 million annual active customers.

While the management talks about increased active users and synergies from the food delivery business to the main retail business, we see no sales impact on the main business.

The active customer growth is surely from food delivery, and could include many duplicates.

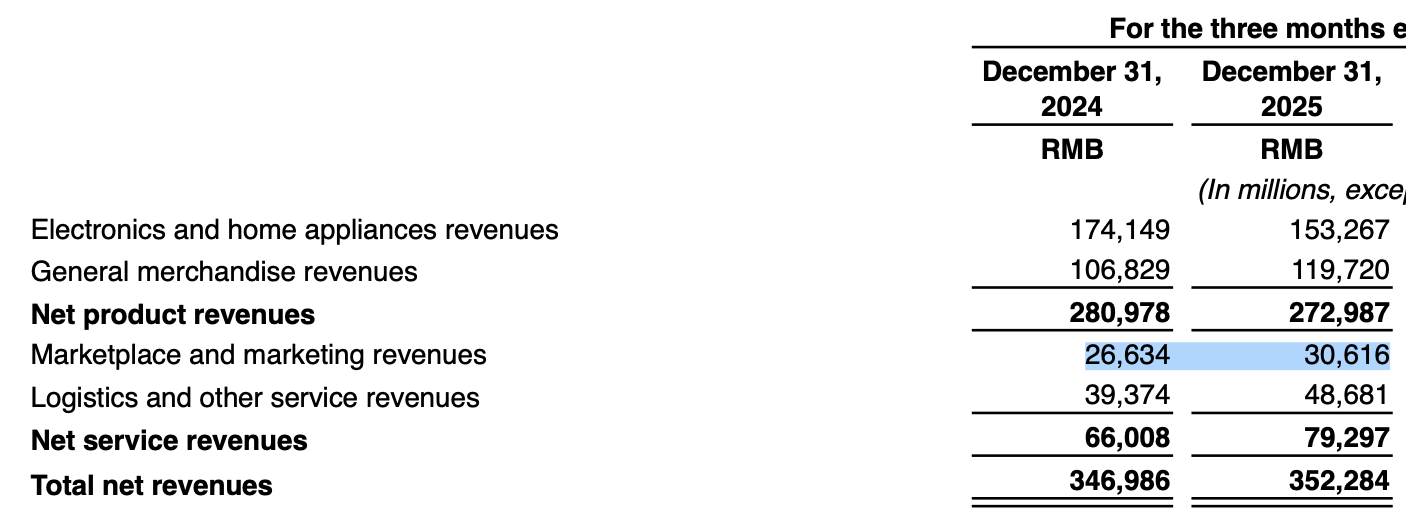

Main business: (JD Retail)

The main business is doing fine, but not showing a huge growth on par with a 30% growth in customer base.

The product revenue is down in Electronics and home appliances are down due to large public subsidies last year. Logistics and service, and general merchandise are well up.

Marketplace and marketing revenues are also well up. The flywheel continues well in the main business.

Q4 sales and operating income showed no improvement from last year and are worsening sequentially.

It is likely a seasonal issue with JD that is also validated in 2022 and 2023: The Q4 operating margins are lower. This is due to intensive retail competition and subsidies, hiring of temporary fulfilment staff, and larger mix of electronics.

Joybuy:

JD has launched Joybuy in Europe in March. This is an ambitious business.

Joybuy is JD’s push into Europe with 1-2 days delivery and local stock. This is the answer to Aliexpress and Temu.

This is done with integrated logistics within Europe and with good synergies since JD bought in 2025 the European retailer Mediamarkt.

Joybuy has received a very positive user feedback, especially on the performance side. Logistics experience will be a key differentiator for Joybuy. We are building our own delivery network in Europe, and JoyExpress has been launched recently. It provides same and next day delivery in major cities across the U.K., Germany, France and the Netherlands, along with services such as door-to-door delivery. We welcome all analysts and investors to try out our services.

We will see what happens. Capturing new large markets in Western Europe will take time and not be cheap, but JD is a very patient player.

Conclusion:

I remain invested in JD. This is cheap and has a lot of cash and cash Equivalents (EV of 26 Billion USD versus market cap of 37 Billion USD), as well as a dividend and buyback program (6.3% repurchased in 2025).

But I do not like the continued heavy spend in Food delivery. I thought that it would be over after Chinese regulators issued warnings, but I was wrong. The good thing is that JD could decide to stop these losses almost instantly.

Earnings estimates are likely too optimistic and I do not think that JD forward PE of 9.3 is accurate. I expect the company to earn very little money again in 2026, until Alibaba stops the fight.

A catalist would be a further drop in Alibaba stock price and hype on Alibaba AI fading away, causing investors to demand profit growth. Alibaba is the main company causing the food delivery war to stay at elevated levels.

The good news is that the food delivery war is not helping Alibaba.

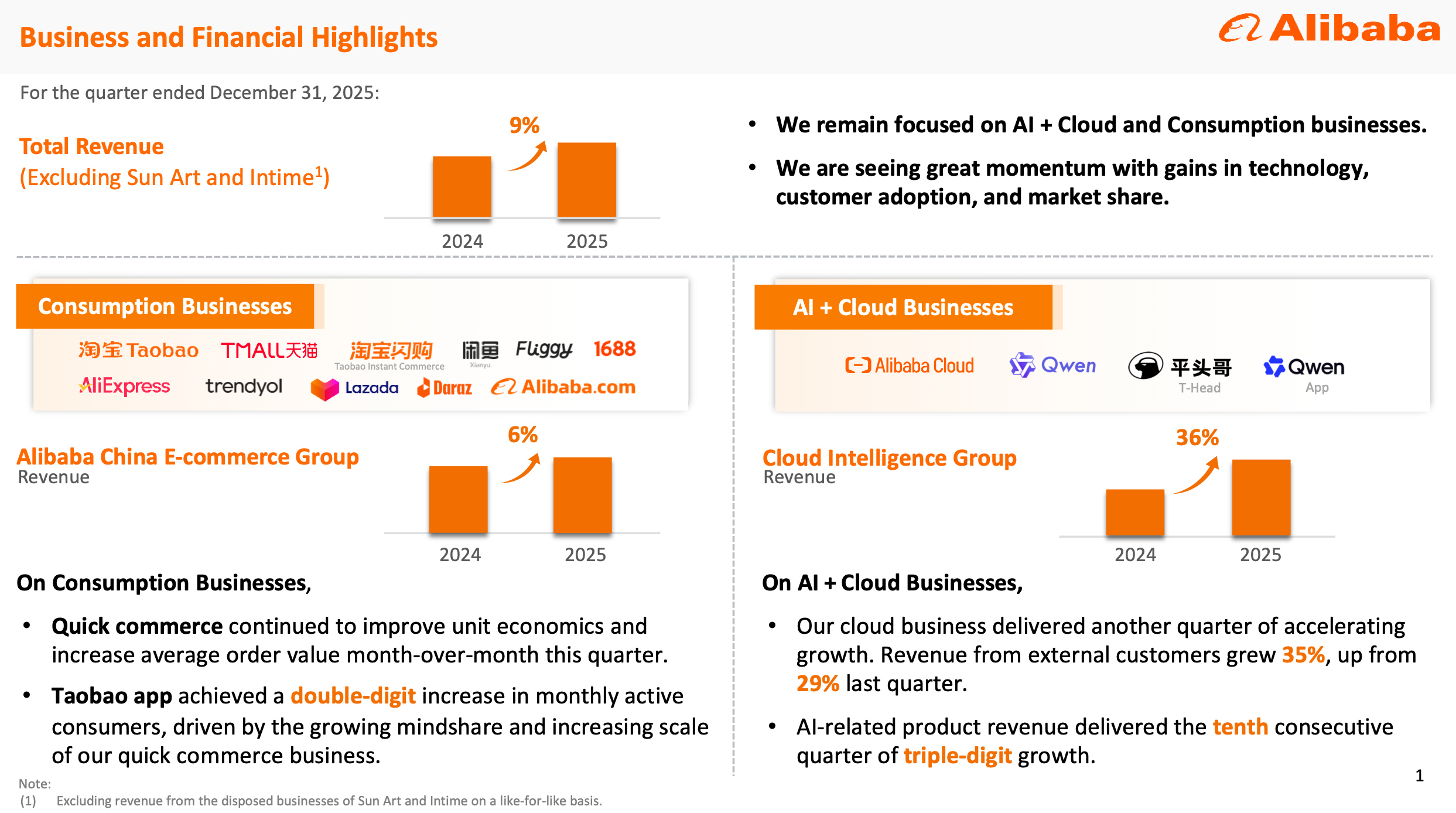

Alibaba is reporting revenues in their quarterly deck first page, cautiously avoiding to mention profits.

However, despite hiding it, non gap net income is down 67%:

Investors have noticed and the price is down in 2026.

A further crash in Alibaba shares would help rationalising this market.

Some key things for companies like JD and Amazon. They share profits with customers, and even in the mature phase, keeping margins quite low. They grow businesses with extreme patience and are ready to lose money on new businesses for years. This is also the case with JD.

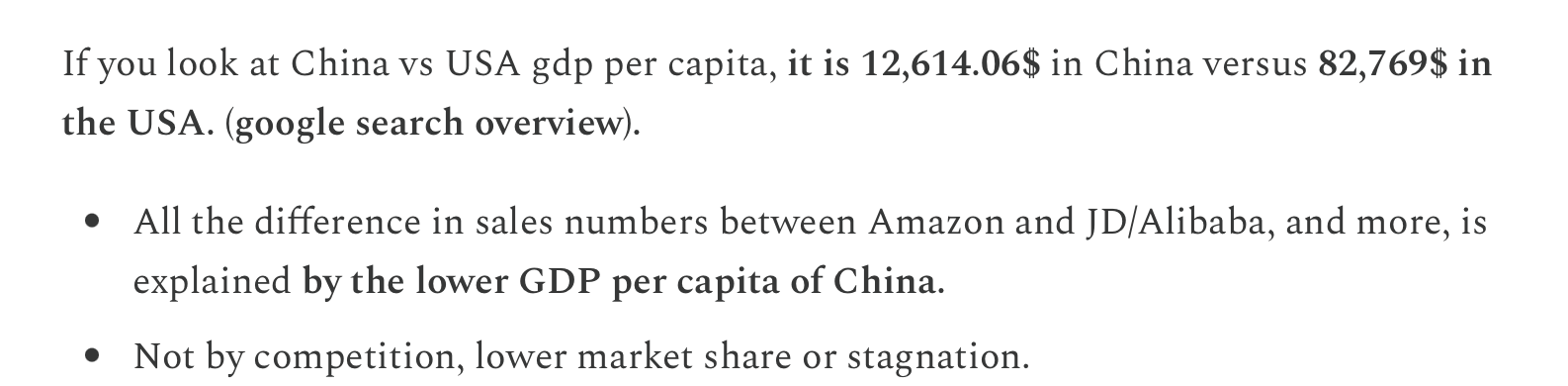

But one thing that is important to the thesis is also the catchup in China GDP per capita versus the rest of the world:

This is also core to my emerging markets thesis that I roll out over the years. GDP per capita growth and increased consumption.

If you want to focus on this long term theme, I recommend reading all the articles and portfolio reviews.

Thanks.

Hi, I live in Spain in an area of very high density with many restaurants within 1 mile. I have no idea about the United States. Food delivery here is popular with a certain demographics ie the people too lazy to walk or the young people who party and are drunk or stoned and just want quick fatty food. Unfortunately here, the options are very fast food based and not offering the culinary experience that I look for. I do get a fast food sometimes but without the premium price of food delivery. I see that it is popular because when I walk around I see a lot of delivery workers picking up orders. I know that I am in the 5% minority of people who have many pleasant food places at a walking distance, and my experience in other countries was much more favoring food delivery, like in the dominican republic or semi urban France.

I am old school and would call or text my favorite places to prepare me something and take a pleasant 10 min walk to pick it up, but this is off topic!

Thank you for the update on JD.com, a question comes to my mind : Is how is the food delivery business working out in the United States ?

-or-

What is the history of food delivery compared to Shopping online and picking up at the physical store?

From my own viewpoint BJs.com has that feature and appears to be working well, when I shop by walking around the store I see there employees filling out orders for customers to pick up.

-- Christopher

PS Thank you for any incites on this difficult question