JD.com is a bit like a little Amazon in the Chinese e-commerce landscape.

JD.com: NYSE/HK

Market cap 49 Billion USD

Well, not as good as Amazon, but close, and I will explain it below.

Of course, I am not an expert on China. but I am a big picture analyst.

Specialists of China had been telling us for years that PDD group buying is the future, that tier 3 cities are the only thing that matters, and that Alibaba was outdated.

Result: They missed a large rally on Alibaba (I only exited Alibaba with a 50% Gain for a better opportunity at the time - as for me Alibaba does not have the highest quality for me). Why? Because value investing works. It is very different to buy Alibaba at 20 times versus at 7 times earnings.

Also there is something that they missed. The behaviour of oligopolies:

The Chinese e-commerce market, as all e-commerce markets, is an oligopoly. It means that a low number of firms share the market. All with big resources.

Therefore, it is unlikely that one company only will take over the market. One company innovating in one way, will be copied within weeks or months by the other companies, especially when the innovation is as easy as a few lines of code and some change of T&Cs and contracts.

You have people saying that company X has more of sellers like Y and Z or more buyers with characteristics like A, B, C and that it is a moat. This is not a moat. Network effect is a moat, but currently it is not sufficient enough in general E-commerce. It is a stronger moat in niche e-commerce segments.

The only moat there can be is physical infrastructure. Because you cannot code it in 1 month. Who has the infrastructure?

A company called JD.

JD operates more than 1,600 warehouses, approximately 19,000 delivery stations and service outlets, and employs over 370,000in-house delivery and operation personnel. It also has over 100 warehouses outside of China.

Another thing that they missed: The long term view. The short term view is thinking “where is the trend this year in Chinese consumers - let’s interview 10 people”. This is is for traders, and even with this information, short term shares movements are unpredictable (Unless everyone is bearish and writing that investing in China is dead, then it’s a bottom like February 2024).

The long term view is where will Chinese consumption be in 10-20 years?

If you go by long term trends, it will be:

Richer

Older

Robotised

AI enabled

The 2023-2024 recession China will be long forgotten. The emerging market will be a well established developed market, richer than the US, with a declining but huge population.

Brief History of JD

It was founded in 1998 as Jingdong by Richard Liu. It was a offline retail chain until 2003, when it evolved to an online store.

In 2007 it launched in house logistics.

In 2014, it did a US IPO

In 2020, it listed in Hong Kong.

In 2020 and 2021, it listed subsidiaries JD health and JD logistics in Hong Kong.

In 2023 it started its first cash dividend.

In 2025 it entered a price war on food delivery (more on that later).

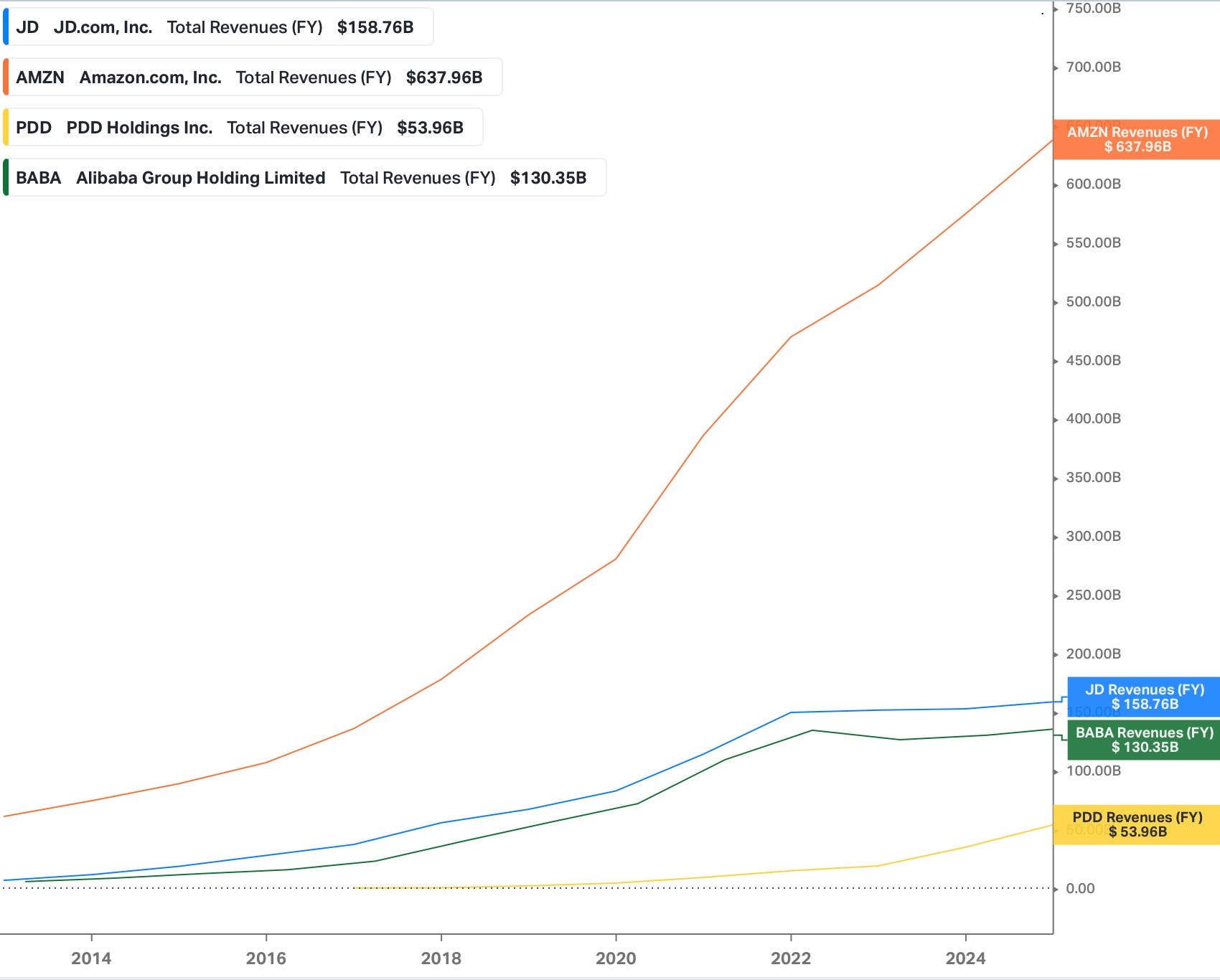

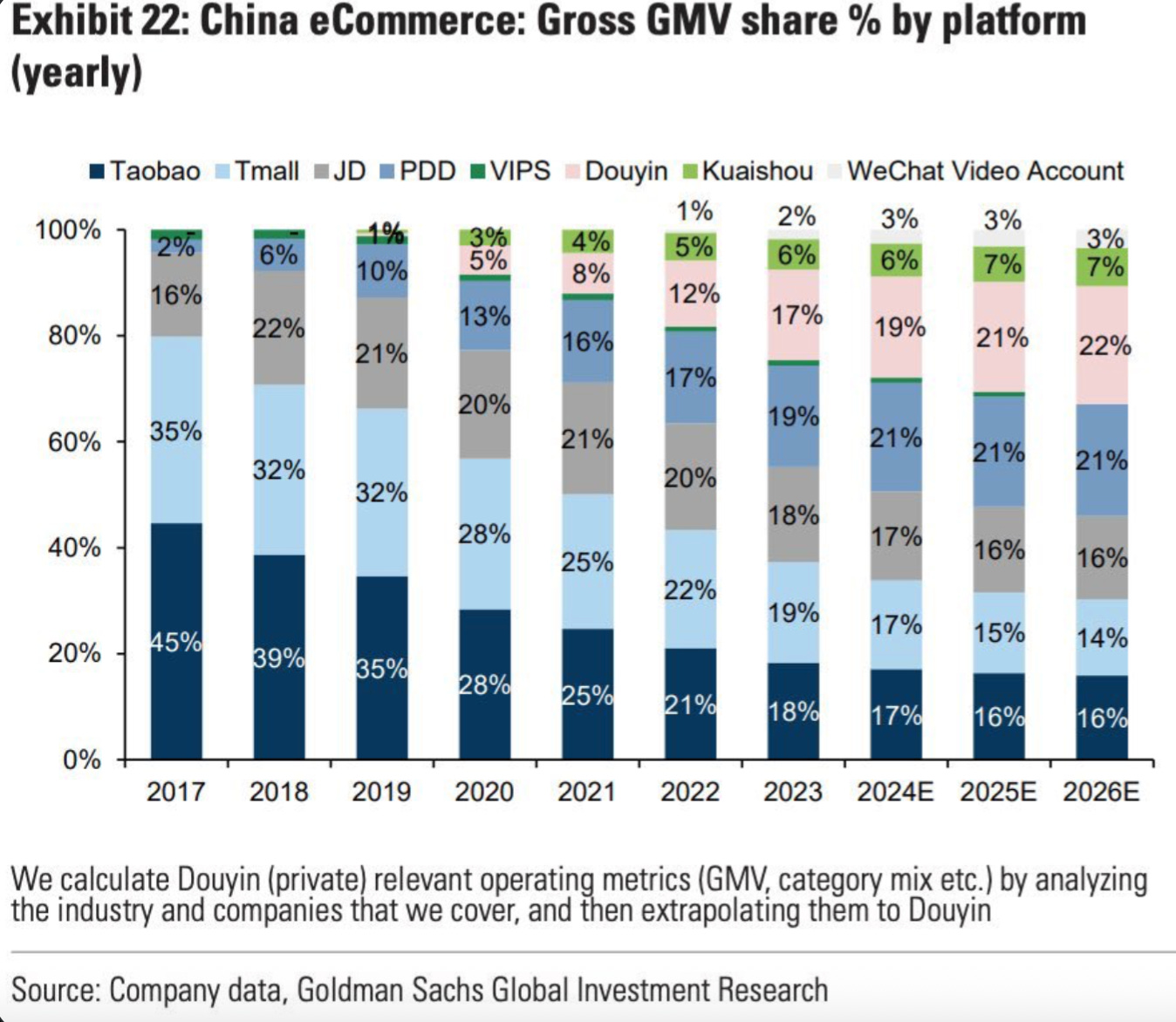

JD and competitors sales development:

JD stagnated, PDD is growing very fast. Alibaba sales numbers are not comparable because it’s 3rd party sellers, but I included it for reference. It is interesting to compare it to Amazon.

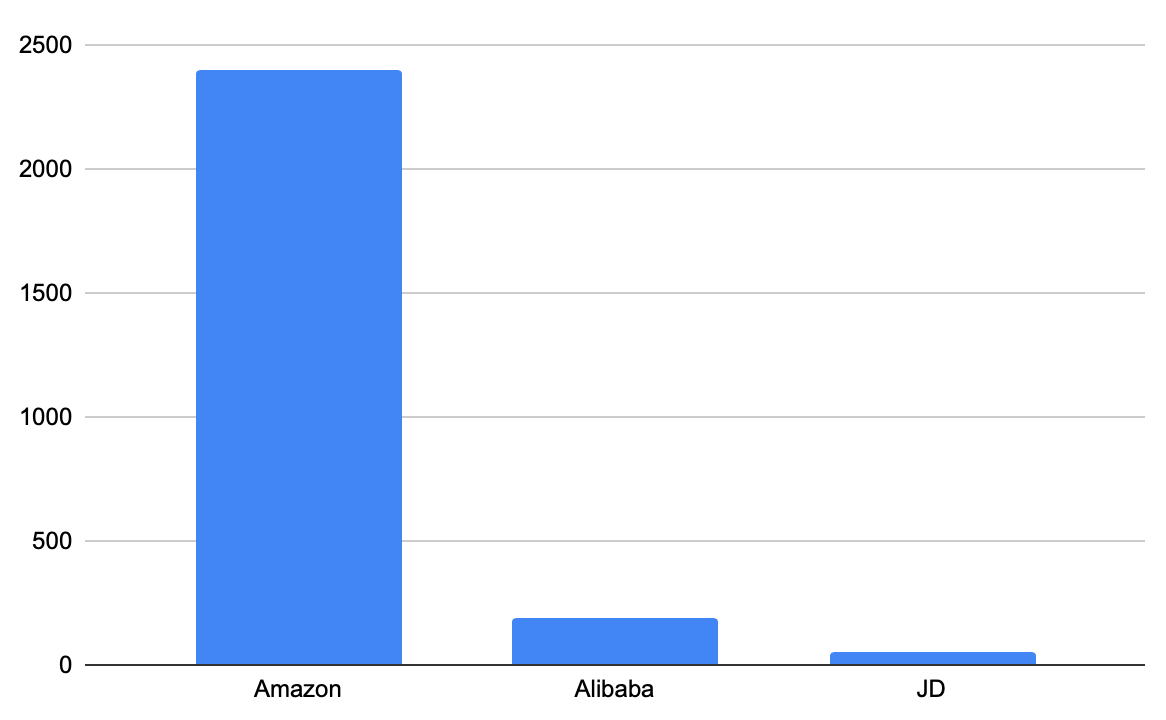

Let’s do basic maths.

Amazon, with 637 Billion of sales in USD, trades at a 2.4T$ valuation.

JD, with 158 Billlion of sales in USD, trades at a 0.05T$ valuation (50 Billion USD valuation).

Amazon is worth 48 times JD in the stock exchange. Let’s visualise this:

If you look at China vs USA gdp per capita, it is 12,614.06$ in China versus 82,769$ in the USA. (google search overview).

All the difference in sales numbers between Amazon and JD/Alibaba, and more, is explained by the lower GDP per capita of China.

Not by competition, lower market share or stagnation.

This means that in the future we can expect JD/Alibaba to reach the Amazon sales numbers when GDP per capital converge.

You can buy JD 48 times cheaper. And I don’t think that Amazon is really overvalued. It is true that AWS is the cloud segment of Amazon and has nice margins, something that JD does not have. Well, JD has some high margin businesses, and growing too, like JD Health.

Due to competitive pressure and the fact that it has no AWS, it is different and not as good as Amazon in terms of revenue growth. The market structure is different. But it is building its business in a similar way.

The market structure:

JD in Grey is losing market share. But this is because the market is expanding with new consumption methods.

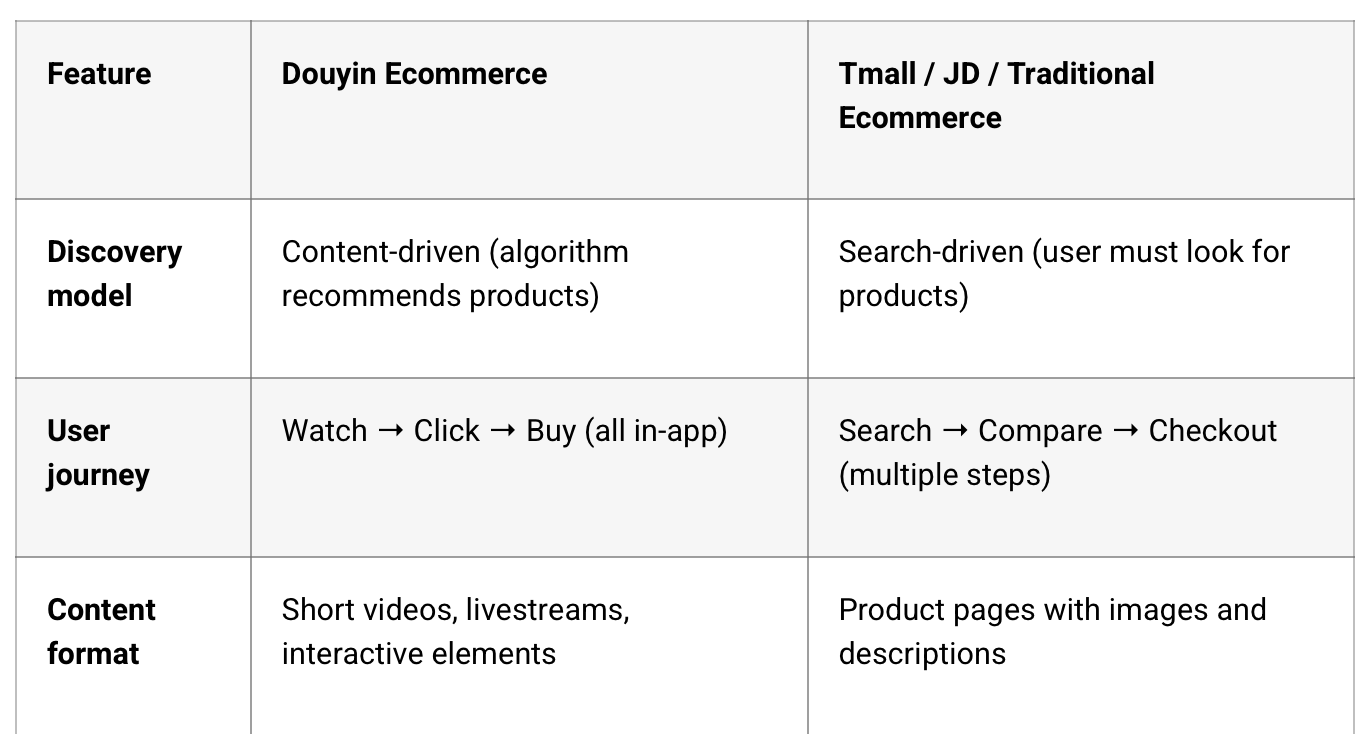

To simplify, in China, we have Alibaba, the main ecommerce holding company website with Tabao and Tmall. Alibaba is like a better eBay. Third party sellers with third party delivery, many items, fast shopping. I double checked with Qwen, Alibaba’s AI. I also like Alibaba.

Douyin is TikTok shop. My understanding is that it is taking market share by generating impulse buying that would not necessarily happen otherwise (expanding the market). You browse, see some product in a video and shop.

PDD (Pinduoduo) is gamified shopping and group buying, but also regular shopping. what is Pinduoduo. I also like PDD, but I want to invest mostly where the puck is. (The richer, older China above). However PDD can still work, because they will adapt.

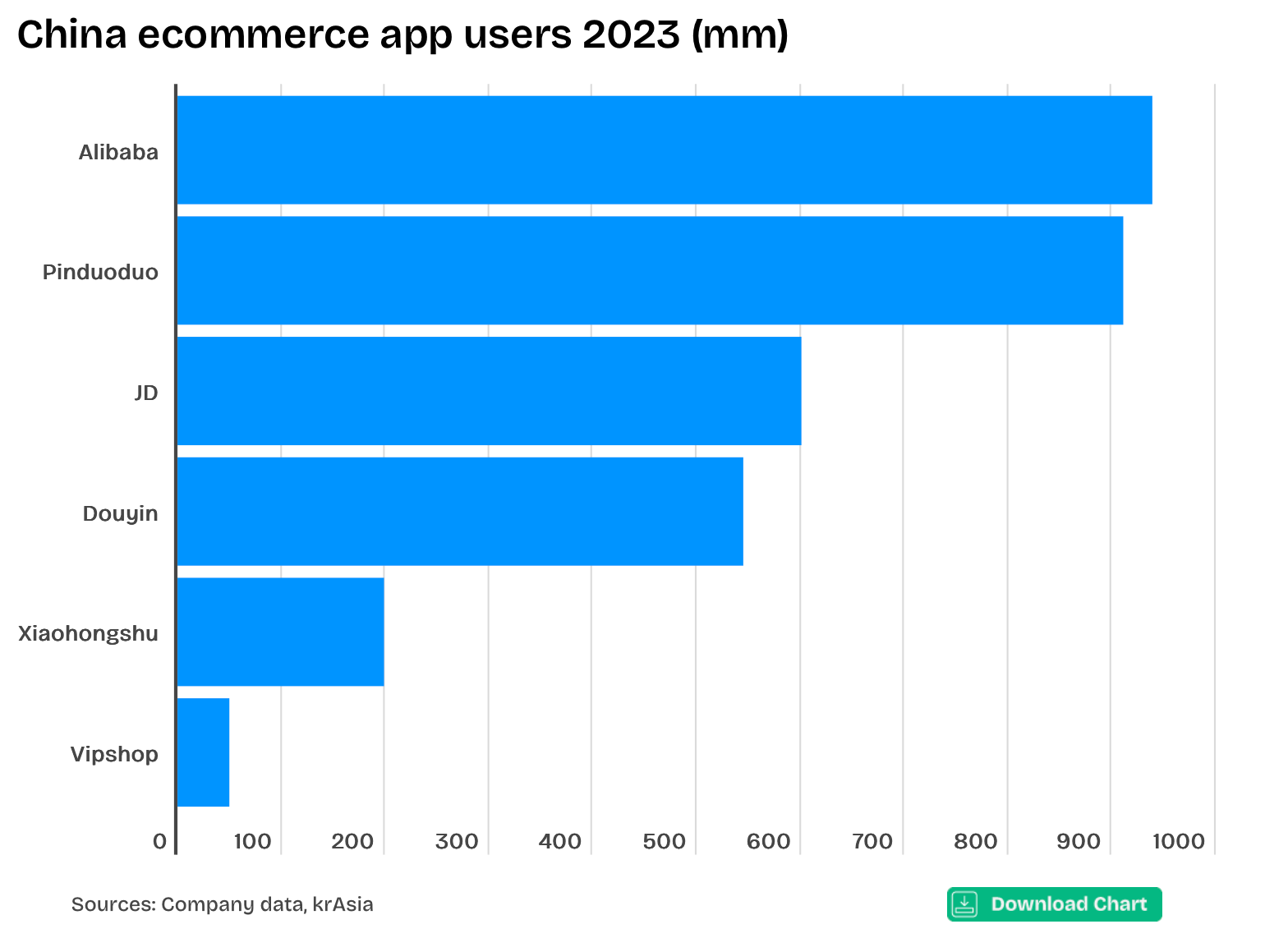

JD has 600 million customers and is behind Alibaba and PDD. Do I view it as potential? Yes, I think it can go to 900 million users.

I have been criticised for not understanding the revolution of gamified shopping and group buying or not understanding the Chinese. It’s true - I don’t. But in the end, I understand humans, lived in four countries and speak several languages. Humans are ultimately the same everywhere, from my experience.

Not on beliefs, but on most fundamental behaviour like … consuming.

And after a novelty period, humans always favour services that give them the less steps to validate, the less hassle or the lower price, or all of this combined.

Do I think that JD will take all the market? No, other companies offer convenient shopping. However, it is clear the JD is the play for a richer, older China while the other players are plays for a poor struggling consumer China. The Video E-commerce companies are niche for a richer China.

What is JD?

“JD primarily targets quality-conscious consumers who are willing to pay a premium for reputable brands, after-sales service, and quality assurance. JD is distinguished by having the most advanced eCommerce logistics network in China”

JD has integrated first party owned logistics with warehouses all over China and beyond. It is obsessive about product quality and customer experience (Like Amazon). It tailors to a niche of people who want the best service and verified products.

It also has the fastest delivery time on general merchandise thanks to its logistics and drivers.

It is on the right side of the trend towards a wealthier, older China.

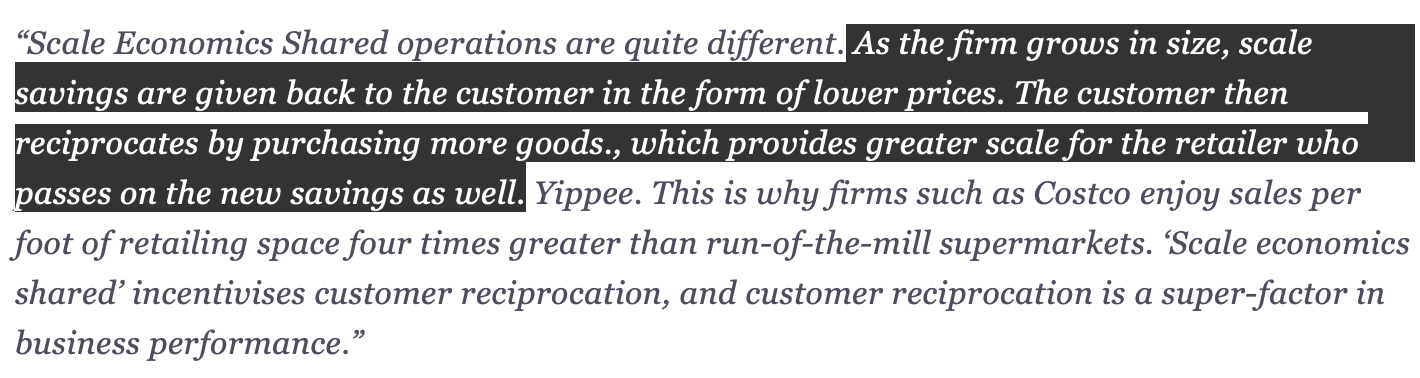

Nick Sleep scale economy shared

Obsessing over customers and building many distribution and logistics centres is key and was key in Jeff Bezos success at Amazon.

My thesis goes against every short term analyst. On the consumer side, I could simplify it to the max by saying “People end up choosing convenience and quality at good prices”.

But the most important is the business and value side. Having a more efficient network is key to offer better price and convenience.

What is scale economy shared?

Nick Sleep was a fantastic fund manager, that returned 20.8% pa during 13 years with his co manager Qais Zakaria. They ran the Nomad partnership. Then closed their funds.

He noted that companies that have economies of scale and offer low prices to customers (sharing the scale) tend to do well.

When they closed their fund in 2014 to pursue other activities, they have advised their investors to put their wealth into three stocks: Costco, Berkshire and Amazon. The performance would have been excellent. My performance would have been better too!

I have learned, and I correct. I now blend value with the best of quality and growth investing. Traditional quality investors often cannot do it, because they focus on past winners only.

And it is going to continue to give excellent results:

So how does JD fits the Amazon playbook? And how is the opportunity?

If you follow me, you will know that the valuation is often insanely cheap. And it is. There is no other word.

Let’s review the business first, the delivery price war, the Amazon playbook strategy and thesis. In the premium report.

Not yet a premium subscriber? You can upgrade below.

You will also have access to the best value and quality companies in emerging markets - the most complete coverage of EMs, as well as my DM picks with excellent defensive hidden champions. We are going to kill it.

A bit of luck, value investing and contrarianism made me buy it literally near the bottom. Now after a big rally and a price trending down again, and some rerating in other positions, I am again buying, and my position is up 15% only on average.

I don’t always catch the bottom, but sometimes close to it.

At month end I will also reveal my other new emerging market position with a new strategy and capital allocation policy. I also missed the bottom there, as some locals caught it, but the upside is big.

Keep reading with a 7-day free trial

Subscribe to Emerging Value to keep reading this post and get 7 days of free access to the full post archives.