Boreo - ex compounder

Finland serial acquirer

Hi everyone, I have been reviewing this company as I saw that it had a low price to sale ratio and an interesting strategy.

Boreo is a struggling serial acquirer.

It had a period of hype in 2020-2022.

Thinking about it, it’s crazy to grow the share price so much, so fast. Irrational hype is costly to the investor. It’s better to focus on value or quality investing.

Serial acquirers had a big hype in 2020-2022, when all that was needed was to acquire companies to get growth. Boreo was a normal company until it transformed into a serial acquirer “compounder”. And inexperienced investors bought the hype of well crafted capital markets presentations and talks. At the end, business matters more than words and strategies.

Boreo aimed for a ROCE or return of capital employed of 15%.

However, what happened, was that some earnings acquired were not as reliable as others. Acquiring cyclical companies only works well when the cycle is positive. Boreo’s legacy businesses, owned before the transition to a serial acquirer, were also cyclical.

When the economy and industry goes down, the earnings go down with it.

This is why I always warned of the Teqnion hype. If you do not know Teqnion, you are kind of lucky. It was hyped by financial social media because of very appealing and exciting compounders hypewords type communication by the management.

But buying cyclical businesses does not protect your company from downturns, even if you have the best managers reading the best compounders history guides.

However, now that the downturn materialized, are some of these companies like Boreo interesting now at 15 Euros?

Business

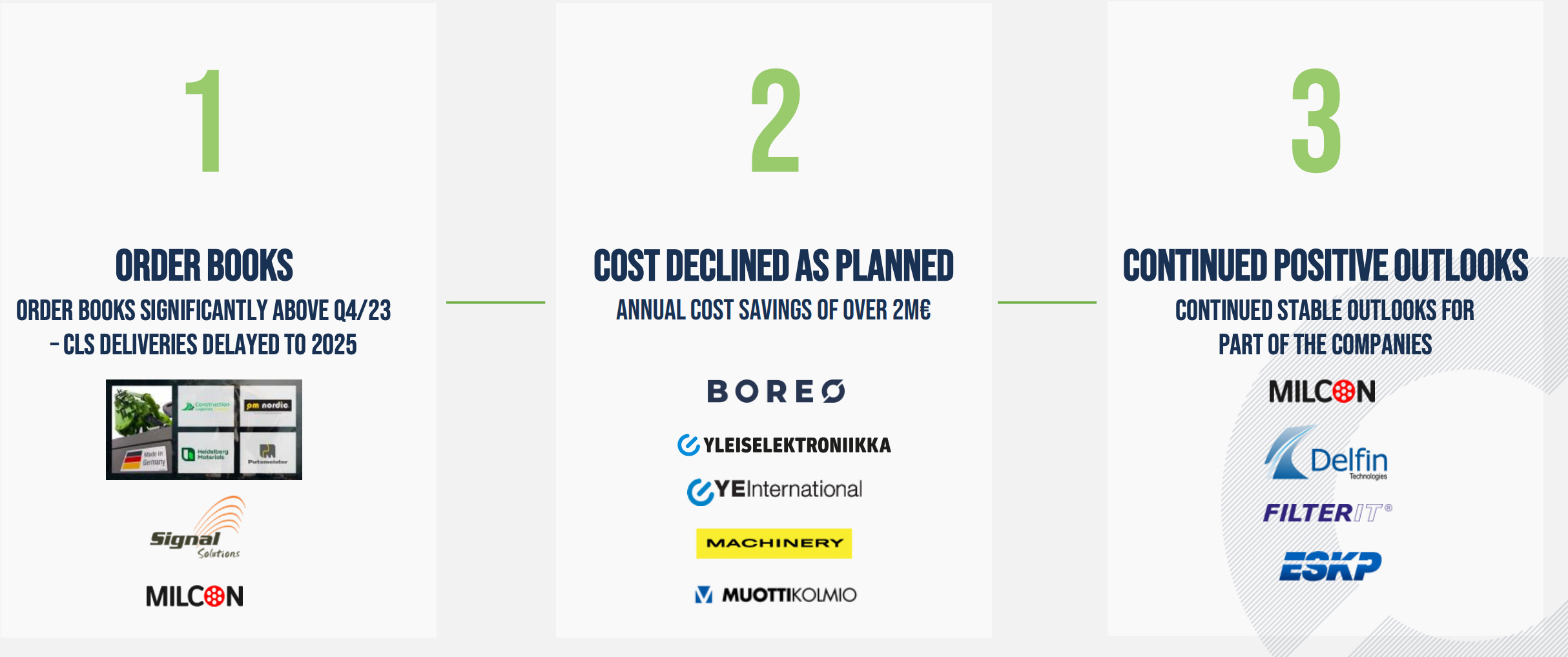

Boreo has two main business segments:

1-Technical trade:

Its companies act as representatives of well known principals and serve, for example, the mechanical engineering, construction, process, forestry and concrete industries in Finland, Sweden and Estonia.

I like that they are trading companies, with low capex, but they are cyclical.

2024 sales are down mostly due to Putzmeister, a German company in the construction and mining segment.

The EBIT margin is really low.

2-Electronics business area:

This segment resisted better to the tough economic conditions, and is stable year on year, even showing growth in Q4, with higher margins than the trade segment.

The company commentary for the full year notes that the

“Defence industry demand creates a positive outlook going forward for Milcon with a growing orderbook.”

Milcon Oyj specializes in military and other harsh environment products and systems.

The good thing is that the sales are within the EU to Finland and Scandinavia, reducing the risks of Tariffs for Boreo.

Strategy

This is the typical serial acquirer playbook, with strict acquisitions criteria, notably in terms of business model and valuation.

Capital allocation

Since 2021, operating cash flow and Hybrid debt has contributed to Acquisitions, some interest (quite high at 13.3 million), and relatively low capex intensity at 7.3 million. The problem was using too much debt for low margin businesses. The management gets a C.

Debt is elevated, but well structured

The company is heavily indebted. 2,8X net debt/ebitda is not very high in absolute, but with a cyclical business and low margins, the ratio can get very high in a prolonged downturn, simply with EBITDA going down. But this leverage excludes the hybrid bonds, taking the full leverage in the 5x range. Way too high.

2024 Downturn

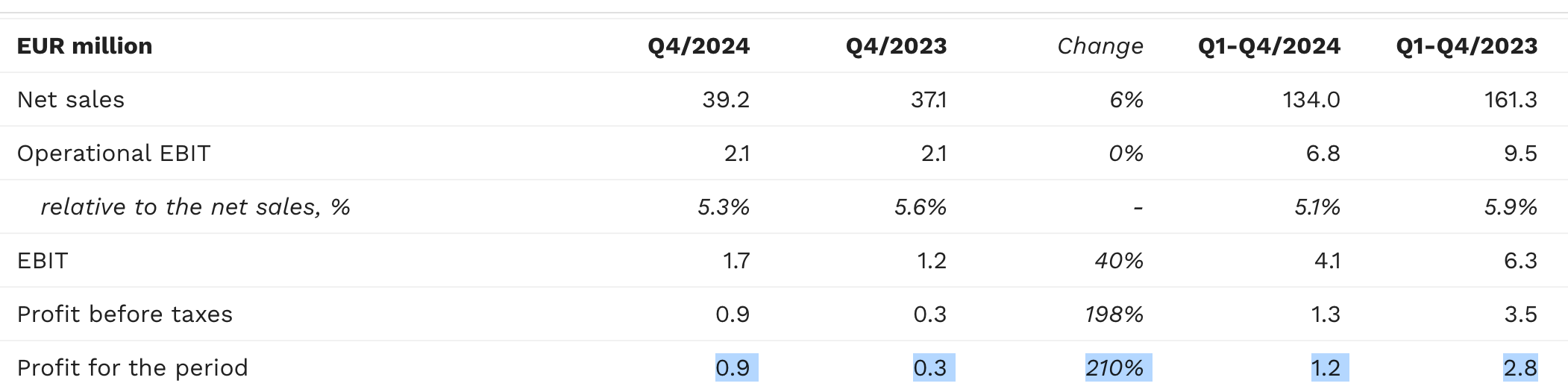

-Sales are down 17%. Ebit is down 28% due to operating leverage, at 6.8 million.

The biggest issue is that the company has 2.8 times leverage, ex hybrid bonds, making that the low margins are then eaten by interest costs, leaving not much profit for the investor.

Outlook:

The outlook is positive on the order book, according to the latest earnings release.

Financials:

In terms of net profit, the profit margin is low, therefore net profits are low, and if we annualize the Q4 earnings, we are at 10 times net profit.

For a serial acquirer, it could be that the free cash flow is higher than the net profit:

The free cash flow statement is not very clear to analyse, but I find no free cash flow in 2024.

All I could gather clearly, is that depreciation minus capex and leases repayments leaves a positive delta of 1.3 million Euros in 2024. Not a big gap. Therefore it explains why the company does not communicate about adjusted free cash flow like some serial acquirers. There is not much of it.

Latest acquisitions.

The company restarted with small acquisitions in 2024, that should not be very material to the earnings, with maybe 1 million of operating profit added. (remember that there are interest costs)

a distributor of welding and cutting products and solutions in Estonia

a leading European distributor of electronics, automation and measurement technology

The businesses acquired are interesting, distributors again with capital light models. The company buys according to the acquisitions criteria.

Conclusion:

The management and the strategy is simple, proven in other companies, it is the typical serial acquirer playbook.

A decrease in interest rates and a cyclical recovery could bring the valuation down to “cheap”.

We are at 10 times profit if we consider the acquisitions in 2025 and a margin of error.

The only analyst covering the name is estimating a low profitability in 2025 with a 17% PE ratio for 2025 and a recovery to a 10 PE ratio in 2026. The earnings are very unpredictable and the estimates have been fluctuating.

The debt is too high and eats the margins.

This is not exciting enough at the moment, due to the low profit margin, and the valuation is not depressed enough.

I am disappointed with what I found here, and I favour less cyclical or higher profit margin serial acquirers, therefore Boreo does not make the cut for me.

It was an experiment to write about prospects, but I think that I will focus on writing about my positions where I feel that the valuation is more attractive, or about interesting potential buys. I should have fully reviewed Boreo first and probably not write an article, but here it is anyway since I started it, and you may be able to find interesting information, and one day buy the stock if the company does a transformative change or reduces debt.

I could not write a fully detailed article when I saw that the opportunity is not really there in my opinion.

I will review more of the watchlist companies that are at Prices to sales of 0.1 and 0.2, but will only write them up if they are interesting.

In the past week, I reinforced an EM oil and gas stock as well as a EM finance company at at PE of 3. I continue with the deep value. That is what I find interesting.

If you want to know more about the other opportunities, I have released some free and paid articles about serial acquirers and other hidden champions.

Thanks.

Note: this is not financial advice, but my opinion on the company. Anyone should do their own due diligence to confirm a company thesis presented and form their independent opinion.