Update: Intrum goes down

The debt collection agency is plagued by it’s own debts.

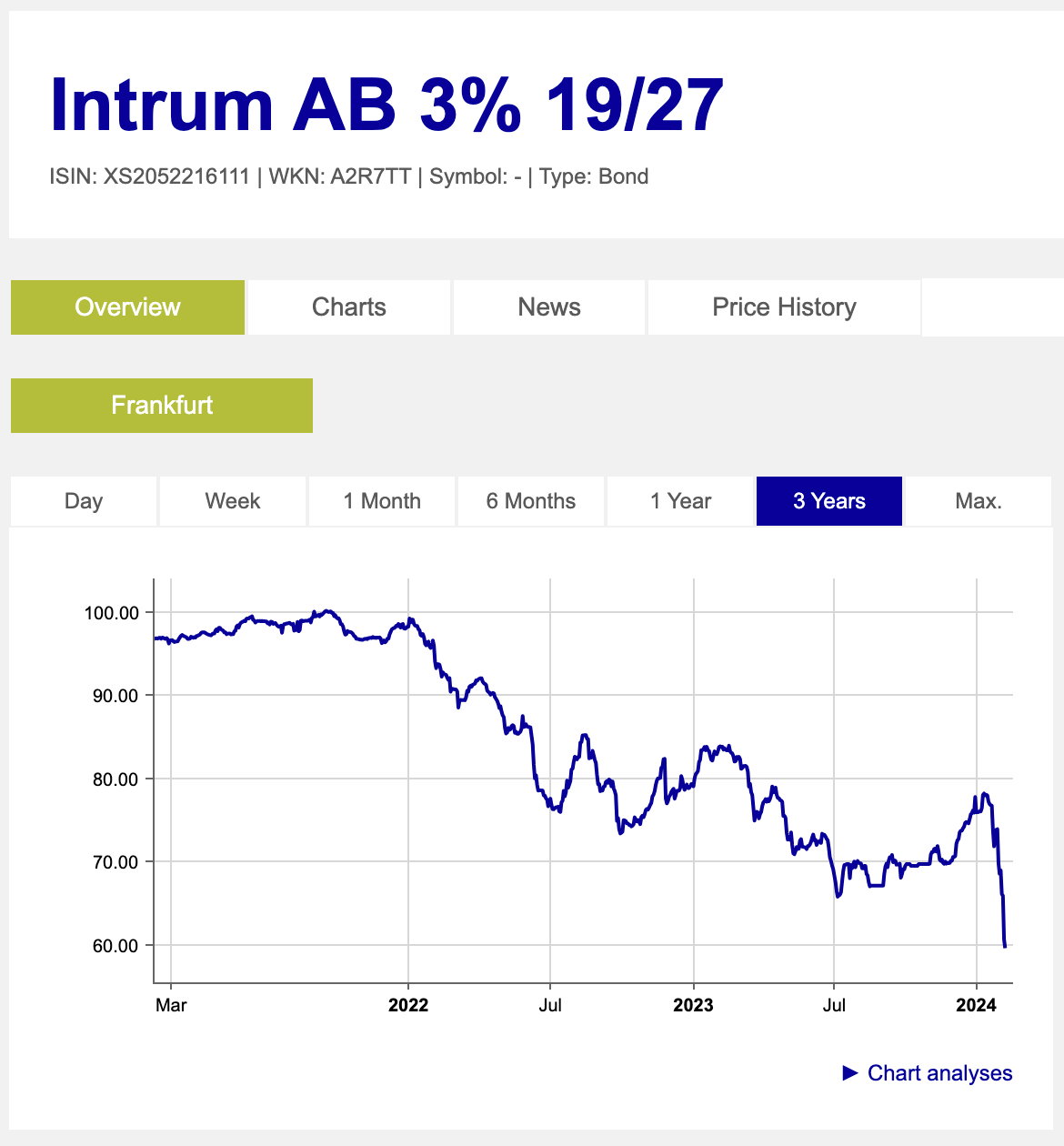

Since I published the write up on Intrum and bought a position, the stock is down by an enormous amount, so we can call this an error, at least for now.

What went wrong?

Intrum buys portfolios of debt to collect at a discount to par, and then collects the debt to make a profit. It is operationally good and is able to obtain a profit on the purchases.

The issue is that requires a lot of capital to grow. So Intrum bought a lot of these “investments” by raising more and more debt. It was ok because EBITDA and net income were growing.

Here comes the increase in inflation of 2022, 2023, creating a double whammy effect for Intrum:

-Rates go up, so refinancing the debt becomes more difficult and finance costs rise.

-Inflation pushes more customer in arrears (good over the mid term) but makes debt more difficult to collect, pressuring earnings.

-Net debt/ EBITDA reaches 4.5, manageable but risky for a financial company.

This is temporary I thought, and I still think. But for these reasons, Intrum bonds became depressed, starting going down, this makes the refinancing even harder or even impossible in the bond market.

It looks like the bank financing pool in Sweden where Intrum is, is pretty small and not very supporting like say, the French equivalent.

So Intrum then decides to slash the dividend and focus on deleveraging. No problems.

Capital light

Then comes the capital light transition - Aka “The problem”.

Capital light sounds nice and modern, and allows you to get a higher multiple by the market. But it comes with some problems:

Investing its capital was a profitable way to grow with returns > > costs. If you stop, you don’t grow. Especially that the servicing business is about 20% of the business and the capital investment is about 80%. If you degrow, then your leverage ratio can increase.. of course you also spend less capital. But this is not sufficient.

It is unclear how fast and how big the capital light (servicing) business can grow, can it become big enough to support the rest of the leverage?

The company aims to maintain the investment business by bringing third party investors and collecting servicing fees. It is also unclear how much they will succeed.

The recession and inflation crisis will bring more servicing, yes, but will it be enough to compensate for less investment? Ultimately if not, I suspect the company will go back to increasing self funded investments, because these are just too good in terms of ROI.

What is risky would be to sell too much of the investment portfolio at a discount. According to the last conference call, it will not happen.

While in the long term this strategy can bring a high multiple and reduce leverage (similar to the IWG strategy), in the short term it can reduce earnings. Even more if the company does badly timed exits:

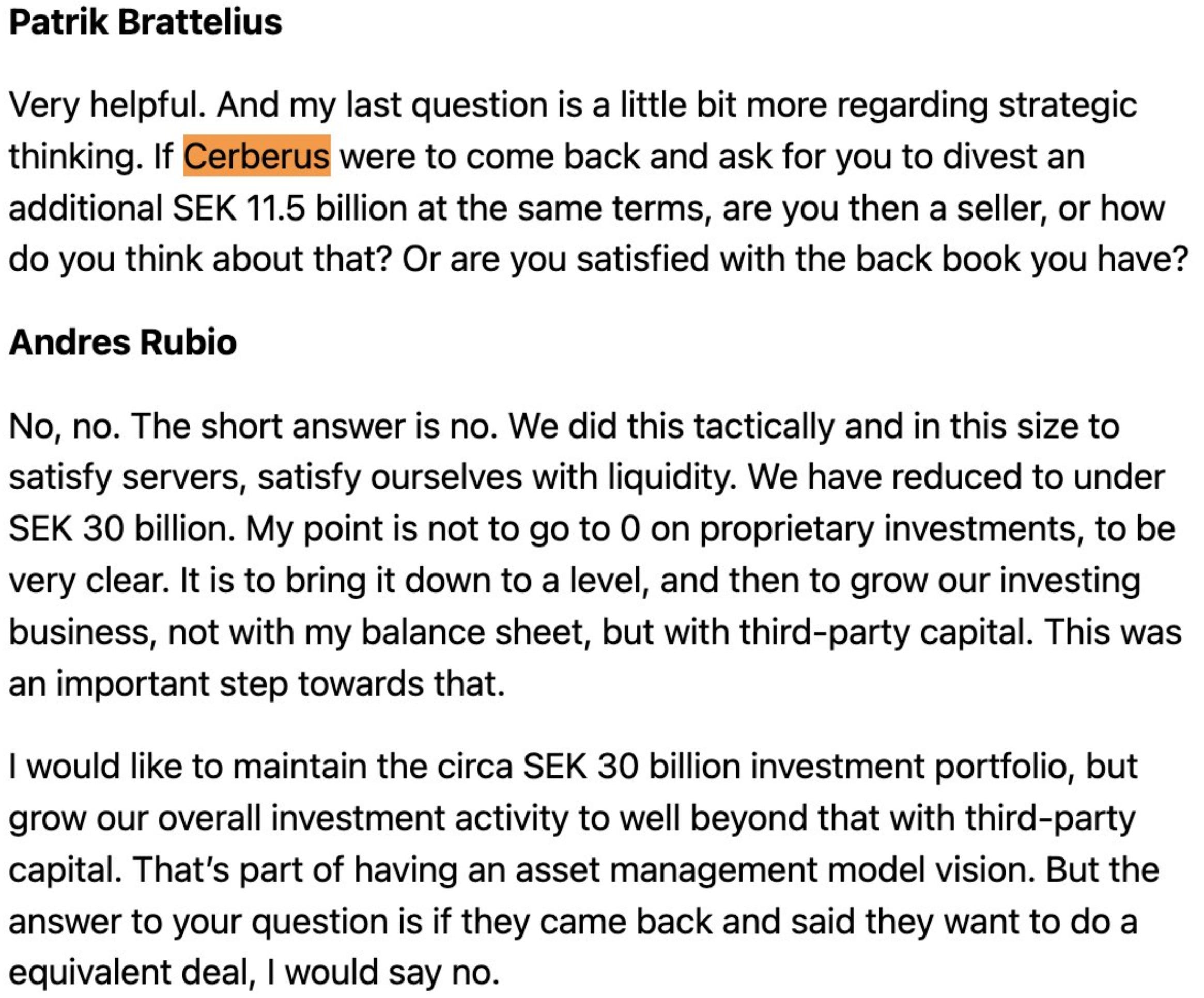

Dilutive sale of assets to Cerberus private equity.

Potentially dilutive exit of some smaller markets - typical bargain deals that large company offers to savy buyers, and this time, Intrum is the seller giving bargains.

When Intrum sold the assets to Cerberus at a discount, it increased leverage! The logic for Intrum was to get enough liquidity to avoid needing to refinance for two years, and also to pioneer the third party investor business model to attract future partners, as Intrum retains 35% in the acquiring entity and servicing rights. Ok, I get this, but it’s a tough pill to swallow, considering that Intrum was downgraded by S&P a few days later, bonds and stocks took another close to 50% fall.

The last part of the saga is on February 7, Intrum making a tender to buyback some of the depressed bonds. I believe this is the right way to go to deleverage at a discount but that it should be increased.

Overall, Intrum is now priced for bankruptcy and is incredibly cheap at less than one time EBITDA, but I don’t see a bankruptcy happening too much, due to the deleverage from the positive EBITDA. My opinion is that everything will recover - but as usual, and especially for a financial company, I could be wrong.

The risk is that the deleveraging does not happen because debt goes down but the EBITDA goes down as much (or more) due to the depletion of the investment portfolio which is like reserves, and that servicing does not grow enough.

Intrum has historically been very resilient, so I am quite optmistic.

However, the markets and bond markets are saying something, and while I love being contrarian, being against the bond market is something else, another level of stubbornness and risk taking. On the other hand, nothing has changed in the company for the bond market to crash;

It did not fall after the earnings

Not after the sale of assets

But it fell after a note from S&P downgrading the company, causing a flows of sales.

They did not analyse the company themselves, but sold on a notation.

In conclusion, I could maybe add one more time to the position because of the deep value. It trades at a forward PE or 3 and 2025 PE of 2, according to analysts.

In any case, money management has to be measured as to not buy too much into a potential value trap, and a potential error.

Let me know if you have an opinion in the comments.

Thanks to Daniel for discussing Intrum with me.

Supporting the publication gives access to:

All the write ups - aiming for 10 a year.

Full portfolio with diversified 50+ mostly EM/small value ideas with short pitches.

Watchtlists in Koyfin with over 200 Emerging and Hidden champions stocks (free with Koyfin).

Sponsorship - get 20% on Koyfin, the tool I use to visualize 15+ years of data

This is my personal opinion and not a buy or sell recommendation. Please carry your own analysis before buying shares.

$asps is arguably even in a worse place, I wonder where the vulture € are to be made in the next credit down cycle

Joint venture books, higher servicing volumes, lower own book & debt and tech investments further improving servicing business is strategy which can work. It is not too far fetched.