First an Ukraine update.

The least I could do is sell my Russian stocks at a loss overall.

Luckily I sold one of them at a win when Putin started recognizing independence of the Donbass republics.

Then I sold the others with a large loss, due to a bias, not wanting to sell something with a small loss the same day I sold the other at a win. That is a bad bias to eliminate.

It was a big mistake from me to think that they were a good hedge. They were against inflation, but were not an hedge against a Russian war. Putin went crazy and destroyed the Russian economy, capital markets and many lives and families with his aggression of Ukraine.

Ok.

Let’s continue with my article that I had started writing before the invasion, and conclude with my favorite tech stocks covered in the series.

I will complete our world tour with some not as frequently talked about tech stocks in the rest of the world. These are not geographically in one single region, but simply are the weird bunch of value tech companies I am looking at.

A.Baidu (HK - $45-50B market cap).

It is the Chinese online search leader with roughly half of the market cap in cash. It has a PE of 15, ignoring all the cash. if we discount the cash, it is much cheaper. This also does not count Cloud, iQIYI, Autonomous driving and AI where they are tremendous on technology, but not yet profitable. Baidu is investing a lot in new products using AI, it is depressing short terms margins in the process, but it is still cheap despite this.

Baidu is using some of the cash to buyback shares.

This is very cheap for the leader in Chinese Search (ex shopping on Tabao - Alibaba). It could get hurt with the real estate troubles in China on the advertising front, but not on the cloud and others (21% of revenues and growing 76% y-o-y in q3).

Baidu already makes revenue with pure AI products, for example:

Baidu releases end-to-end AI cloud solution, powered by Kunlun AI chip and PaddlePaddle deep learning framework, to help financial services firms digitize and automate their operational processes, enlisting leading customers like China Life and Bank of Jiangsu.

Baidu ACE smart transportation has been adopted by 24 cities, tripling year over year, based on contract amount over RMB10 million.

Apollo L4 has accumulated over 10 million test miles, up 189% year over year, and has received 411 autonomous driving permits, reflecting Apollo's broad geographic coverage and wide-ranging test scenarios.

They don’t hesitate to raise money at good valuations for some of their startup businesses. I think that the capital allocation is really good.

more details like this at https://ir.baidu.com/news-releases/news-release-details/baidu-announces-third-quarter-2021-results

I think it is good value right now

B.Tencent, HK, (HKD 4,5 B market cap)

Tencent is the leader in social networking in China with Wechat, and in payments tied with Alipay with Wechatpay.

It also has a large mobile gaming segment.

The revenue is well split between social, gaming and payments at about one third for each segment.

When I calculate the net profit excluding “other gains” I get a PE of 29.

It has a large investment portfolio, including Sea limited and Tesla, and I am not a fan of this. It does not even communicate about it in the investor presentation, which is not good at all. It shows to me that they do not know why they have an investment portfolio for and what do they want to do with it.

Investments in associates 369,441 RMB.

In their investment portfolio, they seem to buy and sell with no regards to valuation like selling Sea limited now after the stock crashed, and buying fully into the 2021 tech bubble, or buying Tesla. So I cannot give much value to an investment portfolio that has no strategy, and is not sound in terms of allocation.

I do not see exceptional growth or valuation that makes the stock appealing, with operating profit up 7% YoY.

Technically the stock is cheap due to the investment portfolio that should be discounted from the valuation, but I cannot feel comfortable with this particular investment management.

C. KASPI (Kazakhstan, listed in London) (11B USD market cap).

It was discussed a lot on twitter. Kaspi is like the Alibaba+alipay+uber eats of Kazakhstan. I expressed a mix of admiration and skepticism on twitter over this company. Kazakhstan recently had a revolution attempt.

What I am more concerned about is size. it is extracting $1B in profits out of a $180B economy. It is a $10B market cap for a 19 millions population. Kaspi charges over 30% on interest on its loans. The take rate on market place is 8.5% and on payments it is 1.2%. I think that is is too powerful and earning too much, and I fear pressure coming on margins from competition, regulation or both.

But on the other hand, the moat due to the super-app and the network effect is huge. The payments take rate is reasonable, and marketplace, while high, is ok. They are excellent operationally by adding new services to the platform.

It is a great company and there are some risks, like the revolution, the seismic real risk for the industrial centre Almaty. There are also some opportunities because Kaspi is in a country benefiting from Oil and Uranium. What I like is that Kaspi is now active in international expansion with the acquisition of a bank in Ukraine. Yes, Ukraine is at war, but will not be forever, and Kaspi will also expand to other countries like Uzkbekistan with $50B GDP, or Azerbaidjan. It is true that none of these countries match the GDP of Kazakhstan. Having the technology, they can bring their services quickly to the rest of the world.

D.Vente Unique (France) (160m USD market cap).

It is an online furniture seller based around France and with European expansion. It is launching a market place.

The PER is 12, it pays a small dividend, but 2022 will be tough in terms of comparables and the company expects a decrease. It is somewhat cyclical because of furniture, but also a secular grower. I am just watching it without taking action and will see how it goes in 2022.

I saw a web conference by them in French and what transpires is that they are very focused, have an attention to detail and are serious about ecommerce consumer proposition.

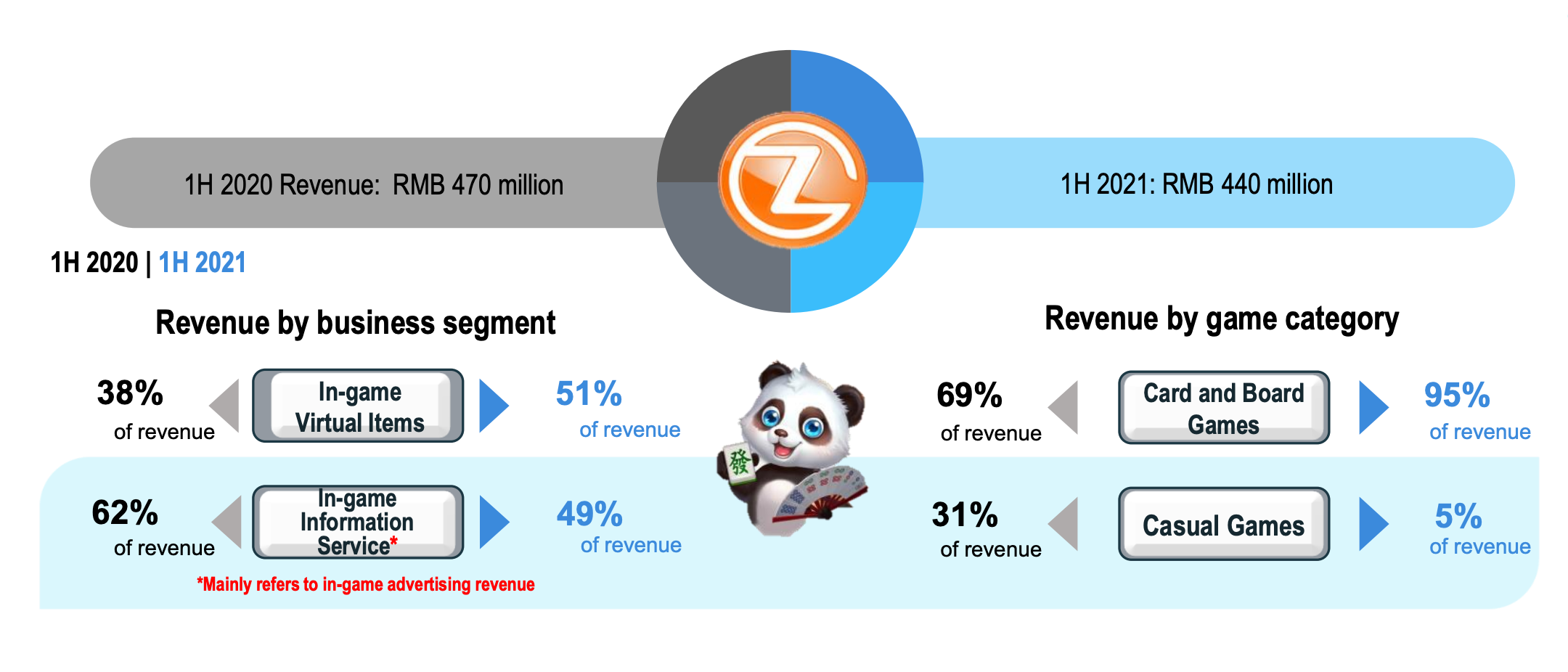

E. Zengame Technology. (China) (180m USD market cap).

It is a video game market selling virtual card phone games in China. Like Solitaire and such but Chinese games. The most popular one is called fight the landlord, a communist card game!

I have no idea what will happen, but it has net cash, pays dividends and a PE of 5. Card games are nice in that they are timeless. It is not like you finish the game and you stop playing the card game. It sells in game items and advertising. I do not really know how much more they can extract from their customer base. The Chinese government limiting new game releases is a good thing for their existing games. It is a bit of a black box, like many mobile gaming companies, and higher risk than normal. It just released a positive profit warning and rose, and the PE should now be 3!

F. Hepsiburada, Turkey, Nasdaq, $600m market cap.

$HEPS, listed on the nasdaq, is a ecommerce company from Turkey with what seems to be a good product. However it is not profitable yet. Worse, it is second in a market with challenging consumer demand, and intense competition. The leader got over a billion dollar funding from Softbank last year. In absolute numbers, $650 million is cheap for a large country ecommerce company. However the downside is also a big risk with unprofitable operations, strong competition and bad macro economic environment. Just keeping an eye on it, it should not be profitable for a few years.

G. Large tech quick opinions:

PayPal is in the buyzone in my opinion for a long term investor. see my previous article.

Alphabet is interesting, but I feel that 2021 H1 will disappoint.

For me, Meta does not have a guarantee of customer stickiness in the future, I do not know what will the customer do in 3 years, let alone 10 years. But it is value.

Alibaba is value but I prefer getting it at a discount with Softbank: Softbank which still has a lot of overvalued investments, which pose a risk to the Vision fund. Unfortunately I am not convinced with Softbank which is still marking up the valuation of its private investments, while the public valuations are falling, and the company has not shown yet that it can thrive in a post tech bubble of 2020-2021 world. Alibaba on its own has a lot of value but a lot of problems, being under regulatory and competitive pressure. It could be a buy but does not compare well to Kaspi which pays dividends and owns the payment system 100%.

Conclusion of the series

Ecommerce is getting more competitive in emerging and local markets. We see that with the battles in China, Russia and Turkey. I would stay away from Ecommerce when Ecommerce companies are not yet profitable or under pressure. We have to be cautious.

Japan and Polish tech appear to me to be the best deals. On top of that they also pay some tech dividends, small for Japan and large for Poland.

Chinese tech is generally good value on a metrics basis but comes with regulatory, VIE and governance issues.

My favourites: (Pre Ukraine War)

Livechat software (Poland) is still a very small company with long term growth ahead on Chatbots, ticketing and knowledge base. It also pays dividends. It is not the cheapest at a PE of about 20 but can show explosive growth with affiliate marketing and a software model. It went cheaper with the tech correction and it was never really overvalued beforehand. I cannot predict 2022 growth, but it is well placed for the future.

Baidu (China) has a stagnant high moat search business and an exciting AI cloud and autonomous driving businesses at a PE under 15 and much less if we discount the cash on the balance sheet.

Medical Net (Japan): Websites and web services in the medical industry + medical services. It is a high moat business at a PE under 15

Zholdings (Japan): High moat ecommerce, chat, payments, websites and search while building a very advanced fintech with already 45 million customers out of 126 million Japanese, at an EV/EBITDA under 15.

Zigexn (Japan): Websites and web services in the lifestyle industry and HR services. It is a high moat business at a PE under 15.

PayPal is starting to get interesting as it keeps going down. Good for buybacks at least.

I also like Vente Unique (France), and to observe it in a non covid year would be interesting. Woodpecker.co was sent to me by a Polish twitter user and I must say I also like this company, even if it is not yet on the Warsaw main exchange.

My favourites: new top 5 (Post Ukraine War)

Livechat software (Poland) corrected a bit.

Baidu (China)

TIM SA (Poland): The Electrical supplies e-commerce company was already value but cyclical. It will now benefit from increased defense investment by Poland and the allies due to the conflict. I expect large investments to support the economy for years to come as Poland is now a center point of attention, and infrastructure will continue to grow.

Kaspi (Kazakhstan): High moat e-commerce, payments, websites and fintech. The stock corrected a lot and is in value territory. Kazakhstan is set to possibly benefit from Sanctions on Russia with business and people moving there in my opinion. So far no sanctions are set up against Kazakhstan, and it is possible that some Russians use Kaspi to buy foreign goods as a gateway to e-commerce in the future, unless it gets banned. Kazakhstan is the biggest and most prosperous country still in Russia circle, but seems quite neutral. The risk is economic contagion, but Kazakhstan sells natural resources, so they are well protected.

Medical Net (Japan) : Same as above

Zigexn (Japan) : Same as above

PayPal (USA) : Same as above

After this tech series, I will go back to do quick value of individual companies.

2021 and 2022 showed me that super-detailled writeups do not really bring value for investors. Pure value stocks outperformed, simply due to multiples. So I will adapt to what the market taught us, I will to spend less time on the details and more time on the basics.

1-is it a good business

2-is it cheap

3-what is it doing with the profits.

4-Earnings news or developments.

After this, the investor can chose either to study one idea in full and get concentrated in the best ideas, or to get a diversified portfolio of value like I do. Always do your own research, but get ideas from others would be my advice.