News and updates #2

Summary.

Newsletter update

Company updates

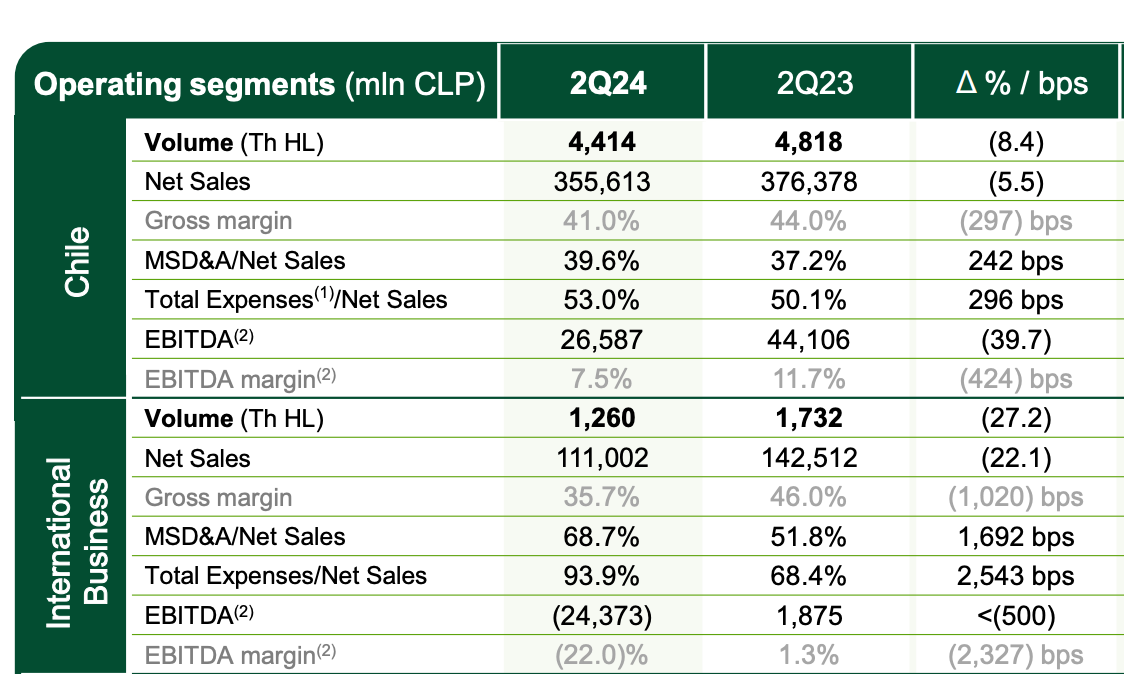

CCU

Ambra

Bastide le Confort

Write ups

Movements

Company updates, Members exclusive:

Text SA - After the crash

Polish and Vietnam nano caps start Buybacks!!

Thanks for the subscribers that have joined recently!! I follow my journey in investing in the 4 corners of the globe in undervalued and forgotten securities for the most part.

check the past ideas and the portfolio!

The portfolio is up 11% this year to date, and It’s as undervalued as ever. It’s quite disappointing but good in a way for buybacks and additions.

I am going to send a public email soon presenting one good EM company I will maybe enter and look for feedback, and one incredibly incredibly cheap EM company but probably non investible for people who don’t have balls of steel. And if you think you have balls of steel, wait until you see the company “write up” ;). This is going to be a funny write up. If someone is crazy enough to buy shares in the company they will get a complementary paid membership!! And please no one start arbitraging the price versus a subscription.

CCU breweries was getting killed on lower volume, especially Chile and Argentina. The stock barely moved, I guess that it’s due to a well shared understanding that these are temporary and macro related. We believe in Milei in Argentina! But I listened to a podcast on Argentina, and Milei needs to repay debt and it’s not easy. Well, they say buy at the darkest moment, and it is here.

Ambra

The Polish wine company saw EBIT declines due to conjonctural factors. On the other hand, the PLN currency rose a lot, so did my returns in Euros. Wage growth is now going to be a thing of the past for the rest of 2024-2025 as the economies are stalling.

Ambra increased investments to be more efficient and immune to energy price rises.

Ambra remains cheap, but the currency is not as cheap as during the time of my write up, pushed by the excellent Polish Economy. One thing that Worries me about Ambra is that Polish people don’t have kids anymore. Since the Pandemic, it’s strange but fertility is dropping like crazy worldwide. It could be due to inflation or due to... well. next chapter please. They will need to expand geographically.

Bastide le confort

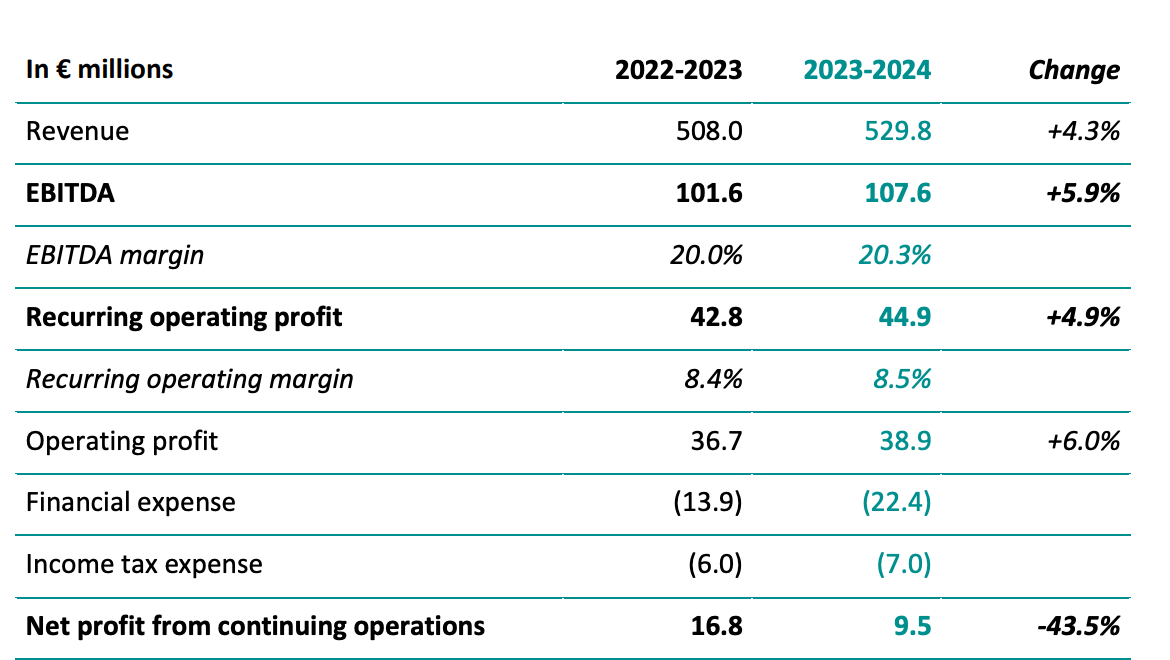

The French healthcare company, had annual results showing a decrease in leverage but stubborn high interest expenses. Organic growth is at 7%, and some sold assets are already discontinued but the cash is not there yet. Rates going down + Organic growth being like clockwork makes for an safe play but net profit are low. Management is good operationally but did not manage the debt well. Leverage is down but interest expenses eat most of the EBITDA.

Next year interest expenses should increase a bit before going down as the ECB cuts more. (I estimate them at 26m Euros under current Euribor). When we go under 3 times net debt/Ebitda, the debt conditions decrease the rate applied by 0.5 points, and by 1 point when we reach 2.

I wrote up Kaspi ($) and I am quite Neutral after great returns

A good reflexion on value investing and valuations.

Zero sales. I am going to continue never selling. Even if some stocks have lower growth.. they send dividends and I buy growth companies with it. If the low growth companies start having high valuations then I will maybe sell.

Added to a German serial acquirer, and an Emerging market finance company.. all very cheap. It is getting boring since I don’t trade much, but sometimes I open tracking positions.

Further companies updates below