For some reason, there is a crowd of momentum investors that like to bid up stocks “momentum” and later get disappointed and move on, and sell regardless of valuation.

This has been true in European serial acquirers, especially in the Uk.

For example: SDI PLC:

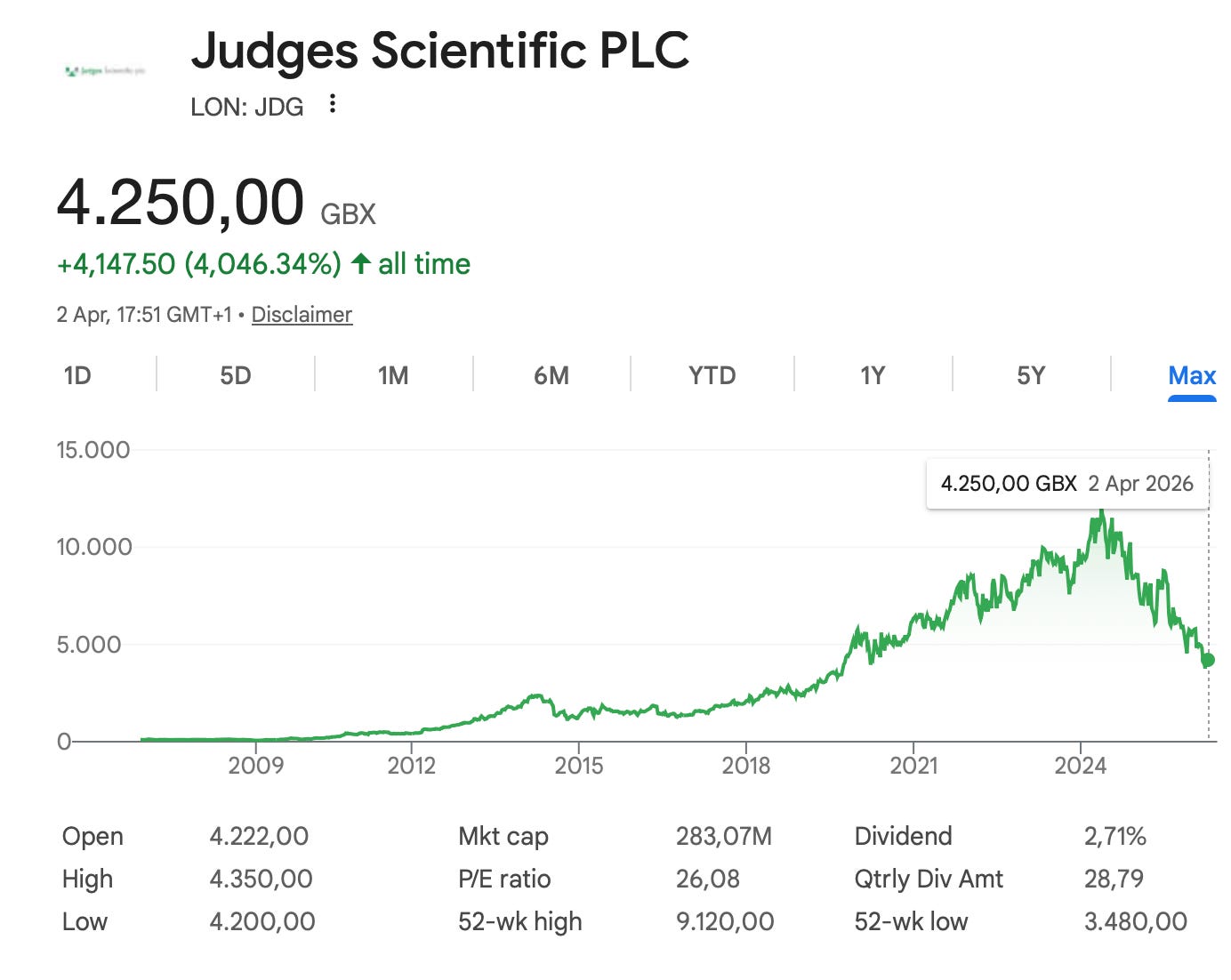

Judges Scientific:

(note that these P/E ratios are incorrect and the stocks are much cheaper than these).

Another stock that I wrote up a few years ago is Newprinces SPA, formerly Newlat, a serial acquirer from Italy with operations in food and now distribution.

A few years ago, the stock drifted towards 8 times free cash flow because there was no exciting news, so some investors thought that dumping a good company at 8 times free cash flow was a good idea (Except for tax reasons).

Recenlty, the stock crashed from 20 to 15 Euros in a few days.

A serial acquirer, or a growth company cannot grow in linear fashion with great announcements every three months. Sometimes, things take longer. Sometimes, some quarters or even years will be intermediary transformation years where short term results disappoint.

Newprinces SPA is a food company with Italian roots that has expanded to the UK with the Princes acquisition.

The miscommunication around Carrefour

Newprinces decided this summer to pursue a vertical integration from a food manufacturer to a food manufacturer and retailer, with the Carrefour Italy acquisition with over 1000 stores mostly in the rich north of Italy.

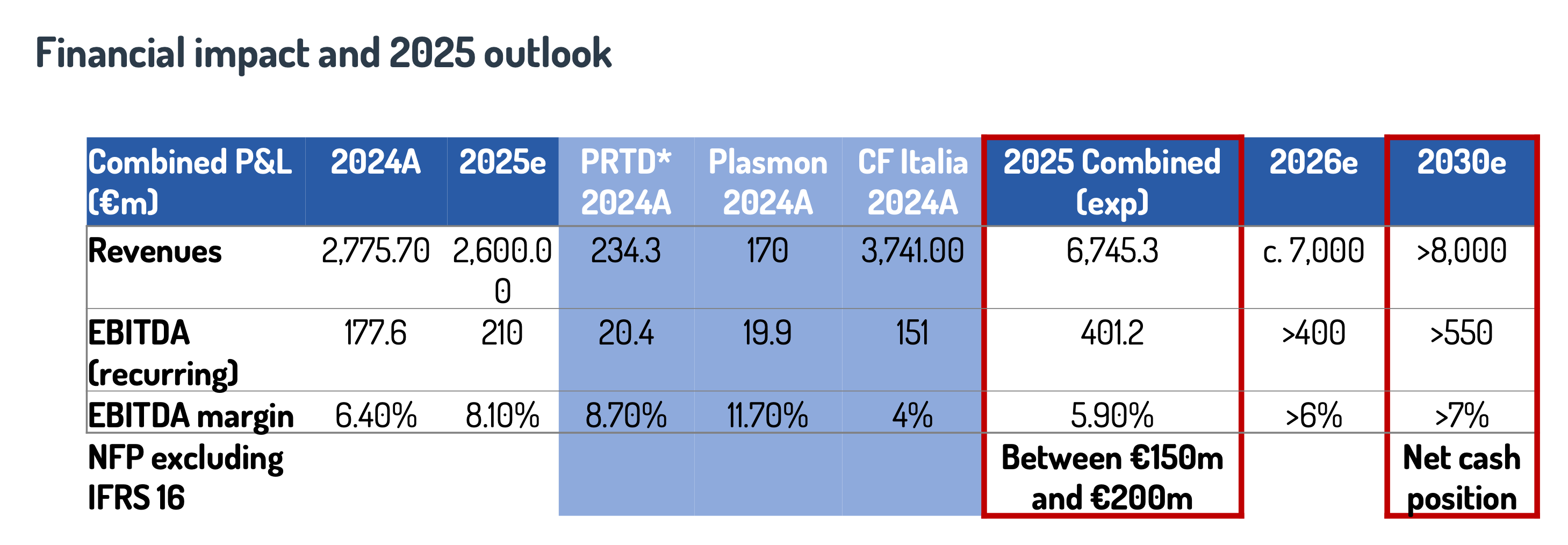

I wrote at the time that Newprinces added 115 million of EBITDA, probably only half of it translates to profit or 60 millions. This was communicated by Newprinces at the time: 115 million of EBIDTA.

The whole group was announced to do over 400 million of EBITDA as of December 2025

They also repeated it in December 2025 in another press release:

Acquisitions of Carrefour Italia and Plasmon are expected to contribute to an increase in EBITDA of more than €200 million in 2026, further strengthening the Group’s cash generation and financial position

But the problem is that Newprinces revised these estimates sharply downwards with the earnings release for Q4 2025 published at the end of March.

Therefore, after an initial price boost, we saw some selling and the stock crashing to 15 Euros a share.

Newprinces SPA earnings update:

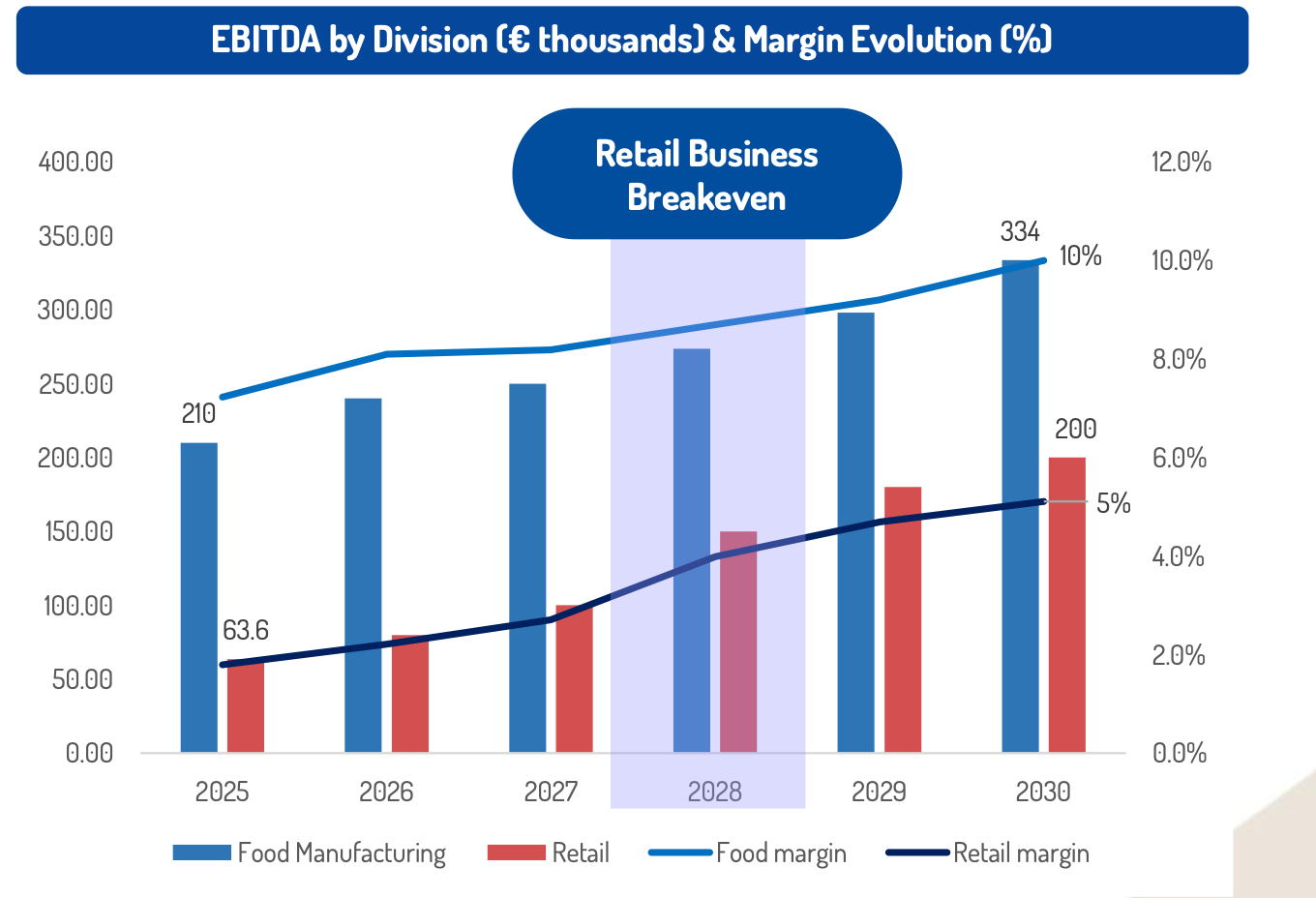

While Newprinces published earnings that were satisfactory and initially pleased the market, hidden in the earnings release was a slide showing EBITDA for retail only reaching 140 million and breakeaven in 2028, while 2026 is expected at around 70 millions.

This was four months after announcing 150 million of EBITDA for the retail business. A drastic change.

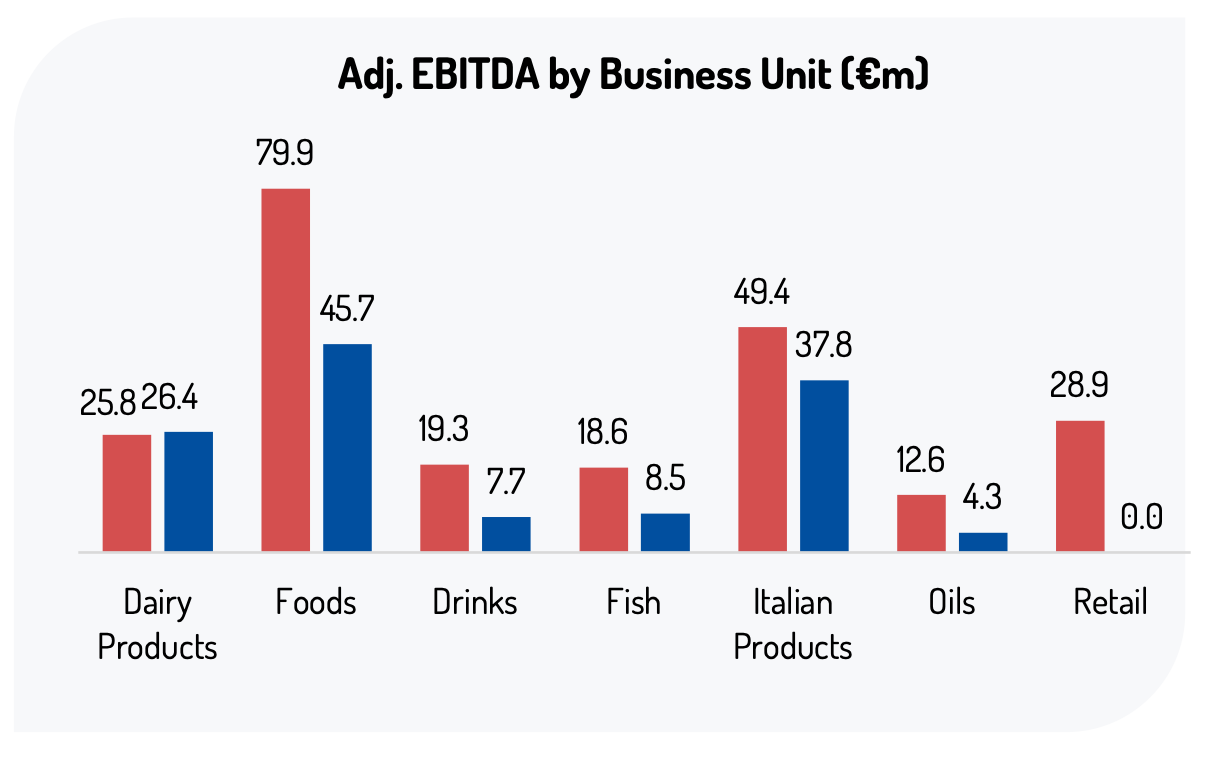

Which is strange since in Retail had 28.9 million of EBITDA in December 2025 alone.

In one month of operation, Retail did 28.9 million of EBITDA, but is expected to do 70 only in 2026? Something does not square. Maybe it was really good because it was December and Carrefour Italy sells also gifts, toys, and large items for Christmas.

How do I view the company and what is the real earnings power of the new combined business. This is what I cover in the rest of this weekly article.

The world is burning - the portfolios are hurting - therefore I have opened the 7 days free trial option: upgrade below for the full analysis and gain access to :

the emerging market focused portfolio and write ups history

the serial acquirers/hidden champions from Europe and DMs

the new dividend growth investing portfolio.

Keep reading with a 7-day free trial

Subscribe to Emerging Value to keep reading this post and get 7 days of free access to the full post archives.