Newlat foods. Another quality stock at a cheap valuation

Updated: May 24

For the first time on my blog I will present a developed market stock, based in Italy.

I do not expect people to have a portfolio of 100% emerging markets, and I am the same, just for balance between economic cycles, I have some stocks in developed markets close to where I live, in Europe.

EDIT 24/05:

1-Error or issue in the FCF calculation: The line IFRS 16 Capex was not deducted in my calculation. During the q1 conference call, it was clarified that this is not real Capex as I thought, but its corresponding to rental expenses which should be deducted. As a result the real FCF is now lower at 22+- for a market cap of 290 and makes the stock less interesting.

2-The company is ramping up a baby food contract in one of their factories that will push the utilisation rate up and the margin.

Presentation

Newlat foods is an Italian food stock with 50% of sales abroad, selling at an estimate 9-10 times FCF to equity owners, with imminent acquisitions that should increase FCF from the first year.

The company sells Pasta, Bakery, Milk, Cheese, etc. What I like about it is that it seems

like quality products with a mass premium positioning, and abroad, a premium due to the packaging and Italian heritage. We can all admit that Italians are serious about their food.

It is family controlled and grew by acquisitions.

Business Characteristics

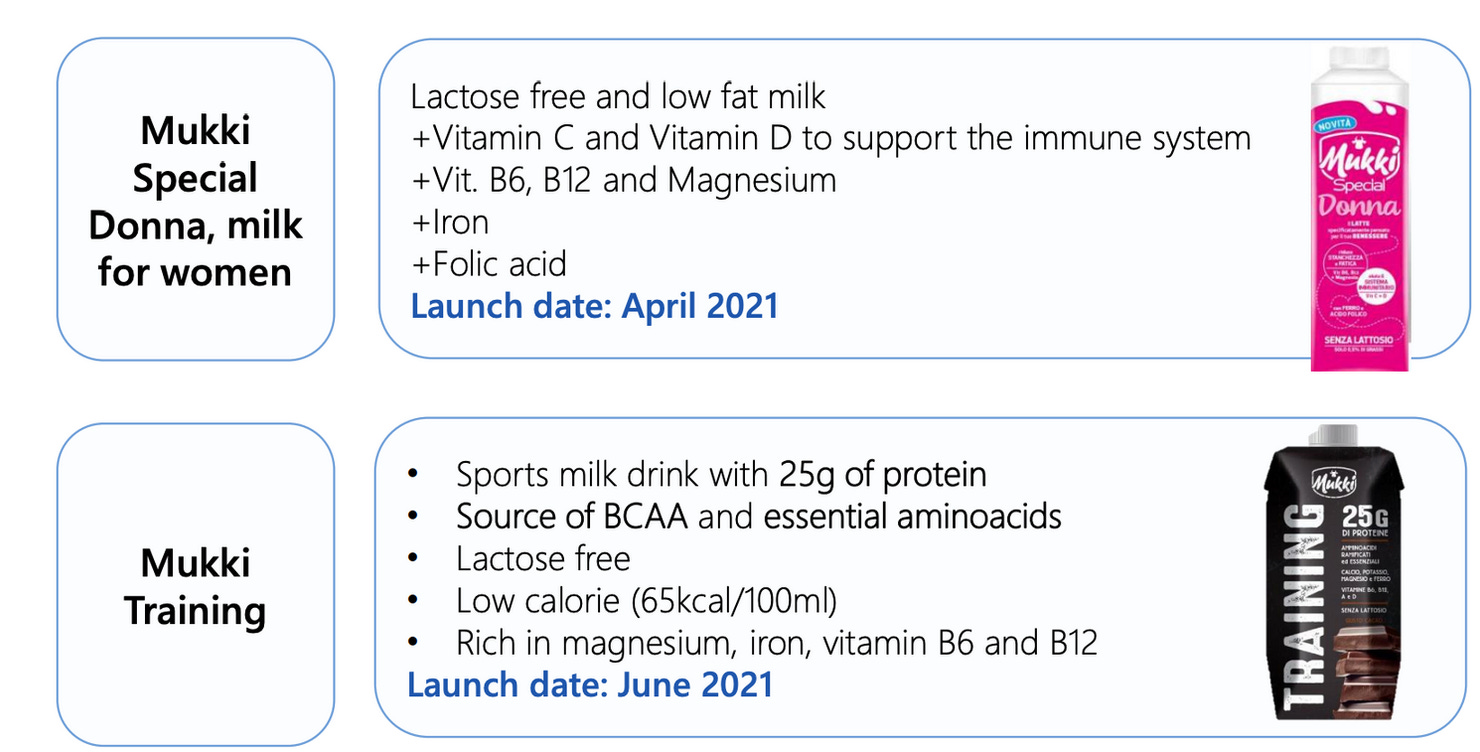

They are innovative on products and launched in 2020 "“BIMBO” infant milk", or as they wrote: "Delverde (Pasta) was successfully launched more than 7 of the biggest retailers in Germany"

Two milk based drinks are set up for 2021, as you can see with slick branding.

Last year, it did an important acquisition;

a 60% "Controlling Interest in Centrale del Latte d’Italia (“CLI”)·" Latte means milk in case you do not go to Starbucks! They bought it for 7.3x EV/EBITDA post synergies, which is good.

With synergies such as procurement, product cross selling, administrative costs and factory utilisation, managed to increase its EBITDA margin from 3.6% to 10%. It seems too good to be true, but it is.

It is important to understand that Newlat's management is a team of builders and not just asset buyers or financiers. For this purpose you can consult the powerpoint on CLI's acquisition, which details a clear synergy and product centric strategy: https://corporate.newlat.it/en/download/centrale-del-latte-ditalia-acquisition-presentation/

Figures:

2020

Revenue: 519 M

EBITDA: 51.4 M

FCF 24.8 M ex working capital.

we can estimate that 2 M are representing the corresponding non controlling FCF interest in Centrale del Latte (4.7 M fcf), we have the full 2020 FCF at 23 M.

2021:

Estimated capex will be 11 M, much lower as guided by management, because it is mostly maintenance capex, so the new FCF estimate is minimum 33 M Eur.

We will have also non controlling interest of let's say 3 M. so FCF of around 30 M Euro to the shareholder.

Market cap: 277 M at time of writing, so P/FCF 2021 is. 9.2.

(Edit, new figure calculated at the end of the article)

It is not totally accurate, because the company will have an higher interest cost since it raised 200 M Euro at 2.625%, or 5,2 M annually. However, I do not want to consider this in the valuation.

These are not operating costs, but funding to do acquisitions. At this rate, any acquisition using all the funds will be immediately accretive to earnings. The company has many acquisition targets. Also, some of the other interest income in 2021 should be lower with debt paydown.

Risk:

1-Is it over earning due to Covid? Not likely as stated in this quote from the annual results:

"Extraordinary Covid-19 positive impact in March and April 2020 was fully offset by the reverse Covid impact in the period of June–August."

2-bad acquisition: In defensive consumer goods, there is not much that can go wrong, aside from overpaying. As long as the earning yield is higher than 3%, due to the low cost of debt, it will be positive for shareholders.

3-no acquisition: I think that we can forget this risk given management track record, but a delayed acquisition, while carrying unused debt and liquidity would be a drag on returns.

Returns to shareholders:

The company is buying back currently 0.1-0.5% a month. It shows that they view it as a very good acquisition at these prices. No dividends are paid. I prefer a dividend, but if there is a constant buyback, I am happy, especially in a non cyclical business where I know that the money is not wasted at wrong times.

Outlook.

Thanks to current 60% of utilization rate of its production capacity, Newlat Food conserves huge potentials in terms of operating leverage and. growth without much Capex.

The company just raised 200 M Euros, and in total has 300 M of liquidity to do an acquisition and work towards their goal of reaching 1 Billion Euros in sale.

I think that it is a very good stock in a rock solid industry that should at least trade at 15 PE (minimum) or 60% higher pre acquisition, If they make a good acquisition it is an easy double. If there is no rerating, we can enjoy a 10%+ FCF yearly in the form of buybacks.

As a result, I made Newlat foods a big position that balances a portfolio with huge EM exposure.

Will there be an Update on this Stock?

There have been some write ups done by other writers.

The company did some acquisitions and created value. Margins were hit a bit by inflation.

still Long