Monthly portfolio update:

the Delivery hero takeover and the P/E 1 serial acquirer edition.

In this article you will find 3 new positions and two sales, and one big picture review of Coupang.

The portfolio is up 6.5% this year, despite provisioning capital gains.

I did not publish recent company related earnings and news, I was busy analysing the whole emerging market tech landscape and making these moves.

This is now done, so catching up with earnings and updates will be the next step and one update is coming soon..

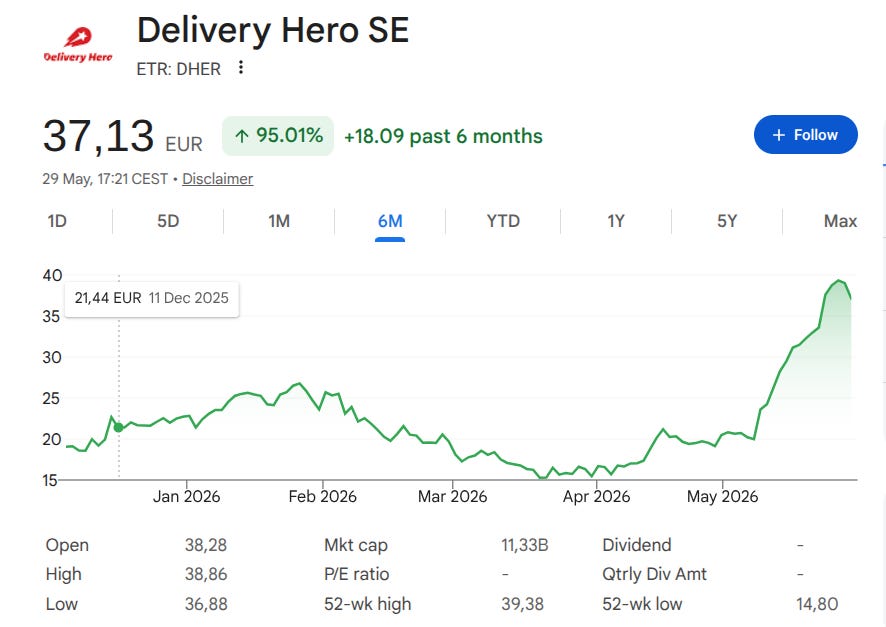

In terms of sales, I got a take over offer at delivery hero with forced a brutal re-rating and it made me execute a sell at 37.65, with my average cost from last year at 25, because it now it is more of a buyout speculation.

After my article on emerging market tech landscape I found some opportunities to reallocate capital in some names, which I will detail below.

I also decided to prune the portfolio a bit with Egyptian company IDHC with 72% gains ex dividends in a short time. It’s a good business but its probably the worst macro situation in the world.

I bought with IDHC proceeds a serial acquirer at 1 times earnings. You read it right. No, it’s not a net cash situation, it is that cheap. I have never seen this. The market thinks that there is a risk of fraud, or bad capital allocation, and it is very misunderstood. So far, there are no real signs of fraud, but it could happen. I decided that it was worth 1% of the portfolio. If it goes to zero, so be it. It could reasonably be a 10x if it’s not taken private like many small caps.

I will also reveal what I thought of Coupang long term potential with a specific big picture approach.

I will also detail my thoughts on Brazilian Fintech. While not having done a deep dive yet, I provide a balanced review of all the metrics discussed earlier (price to sale, active users, TAM, cyclicality).

Keep reading with a 7-day free trial

Subscribe to Emerging Value to keep reading this post and get 7 days of free access to the full post archives.