Market check: Emerging market tech on sale

This week I don’t really have a real update, but a reflection.

I was like paralysed and could not focus on writing.

The reason is that I am thinking a lot at the new opportunity set, as markets are changing.

If I am in deep reflections towards my strategy and the opportunity set, my priority is the portfolio. I know that I can take it to a life changing number I do the right choices.

This newsletter prides to be a shared journey or reflections and ideas rather than a product, which means it follows my investing journey. If I can achieve a good portfolio size, any newsletter income becomes secondary.

So, instead of making a list of opportunities this week or an earnings update, I will share my reflections on the opportunities in the market.

A few years ago you could find some hidden deep value stocks at 5-7 times earnings, wether in EMs or in DMs. These were not the best businesses, but solid. I oriented my portfolio towards this and most did well, while some did badly. Examples would be Jardine Matheson, First Pacific, Poulaillon, Grupo Catalana Occidente, Kulcs software. The last three were taken private. Some serial acquirers did well too.

On the other hand, some European or Japanese stocks that looked like good value and defensive in a recession, got hurt by unprecedented macro events in energy prices, inflation going up and rates going up, alcohol consumption down, trump tarrifs. This, combined with the fact that small caps have generally weaker margins and customer bases than large caps, and often bad managers, created some deceptions. (Bastide Le confort: high rates, Intrum: management not aligned, Berentzen: reinvestment in uncertain growth instead of dividends). These three are still very cheap by the way but with these negative developments.

In 2022, we had excellent large businesses like Meta or Spotify or Mercado Libre trading at discounts and they rebounded very well.

In 2024, Chinese technology stocks traded very cheaply but I did not buy hard enough, despite buying a little bit. The reason why is because I felt, correctly so, that I had other opportunities, as cheap as they are. But it could have been better to sell many investments and buy a lot of Meta or Alibaba at the right time.

These large businesses are incredible, and proved so during the following years, with a strength increasing each year. It looks like Cloud and AI is only increasing the dominance of these businesses and giving them extra earnings streams, or allowing them to reduce workforce in proportion to revenues.

Most of the time, these global tech businesses traded at very high valuations compared to value businesses.

But things are changing.

Interestingly, many high profile tech companies in Emerging and developed markets have been sold off. And they are dominant technology companies with good long term prospects:

Mercado Libre, the dominant platform in Latin America, flat over 5 years and -40% in one year.

Sea Limited, the dominant platform in South East Asia: After a bubble in 2021, it is now down 64% over 5 years, despite a good rebound since 2024 levels.

Tencent, the dominant social media and payment company in China.

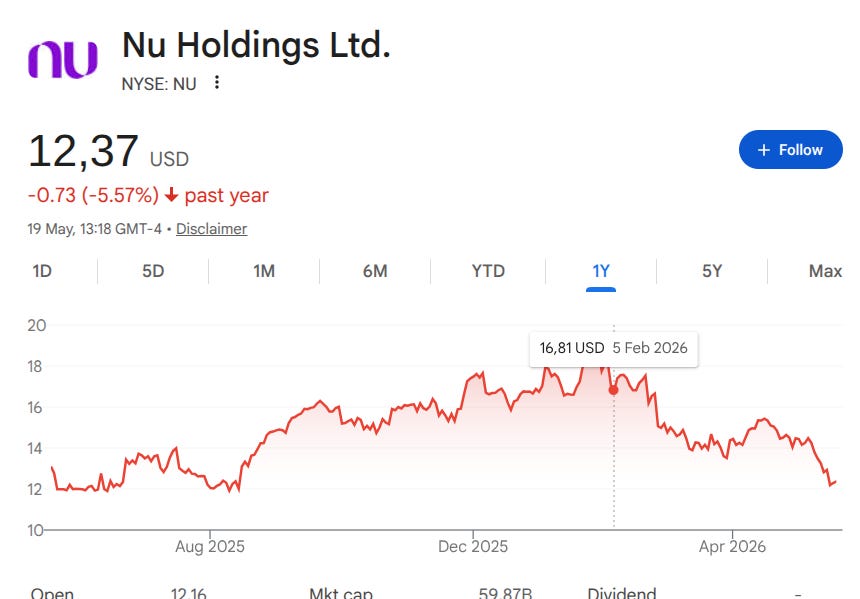

Nu holdings, Latam largest fintech (online bank), was flat over 5 years.

Meta, the dominant social media company in the world, with 1 year stagnation in stock price despite growing profits and revenues.

And there are more.

Some valuations are getting interesting, as you could see in some of my investments recently.

Rise of AI:

In my private and professional life I saw how AI became much more “intelligent” as it was able to guide me very intelligently to handle for example public administration processes, or SQL query analysis and creation, and mind map creations. This is real and we are at the beginning of a productivity cycle in online businesses.

To summarize, these businesses proved stronger than regular businesses, and are only getting stronger and now getting cheaper.

Maybe these collectively represent a unique opportunity.

Maybe it is time to sell some value/quality businesses and pound more on this?

something like this? (AI generated)

It makes it hard to buy anything else that is low growth, even if it is relatively cheap at 12-15 times earnings. These dominants businesses have the advantage to compound revenues for long period of time and at high rate, making that you can truly set and forget.

Portfolio movement:

As a first step, I sold one of my names that was cheap and a good business: Doccheck, a German tech company in healthcare that went from 10 times to about 14 times earnings, and Entered into Meta with the proceeds. Doccheck is really cheap but is a blackbox.

I don’t like Meta capital allocation, but the business is too strong and they can cut the spending when they want to. I feel like every long term investor should be exposed to these monsters that are eating the profits in this world: Meta and Alphabet.

Meta trades at 18 times forward, can run with little staff, and has AI opportunities as well as opportunities to monetize Whatsapp with mini programs and AI.

I also used my latest dividends to reinforce Sea limited, that I entered this year.

Sea limited trades 1.5 forward sales, which with a 10% net profit margin (easily achievable) would be 15 times earnings for a leader in South East Asian commerce.

These examples require very little deep thoughts. They just require to place capital at good valuations and to be patient.

New Focus:

Right now, nearly all my focus for the emerging value portfolio will be on these EM tech companies going forward, and following up on existing holdings outside of these areas.

The Dividend growth portfolio remains secondary and not my main focus. It has performed well so far.

I know that I am not the only writer following these global businesses.

The difference that I change my focus between deep value, tech, and quality based on market opportunities, instead of only focusing on online businesses, regardless if they are good opportunities or not.

I timed the China tech buys well, even if I did not weight it well, and I avoided the popular em tech names like SEA and MELI and others due to valuation concerns.

I think that it’s a good time to focus on all these EM tech names at the moment.

I build a document of further companies to cover and maybe buy. It contains only one non tech name as a priority.

I am thinking of selling some companies that reach fair value if tech names continue to go cheaper.

This article and comments are open and I am looking forward to your comments. How do you view this market environment and opportunities in EM tech, and do you think of increasing your allocation to the sector?

I do have some more hidden tech and non tech positions in emerging markets and if you want the full breakdown, subscribe to the premium tier. I have the archive of other EM and European businesses articles available.

back to research.

Any thoughts on Grab? 14-15x current year EBITDA and 7x 2028 EBITDA based on management's guidance.

You make a very compelling pitch. Does Coupang fall into the same basket?