French Bakery small cap at 3 times Cash flow- Poulaillon

EDIT: see my comment for update after your good feedback

Poulaillon is a stock I am very excited about, despite having lost money on the position. I had built the position slowly over some years. It has some debt, and with lockdowns in France getting repeated, I threw in the towel and gave up at the bottom. I simply had to protect the principal, Seeing the debt and profitability situation under these circumstances, I got out.

I was very frustrated with this, because I had the right company, the right price, I loved it, and I still lost money due to lockdowns political decisions.

Somehow, after a few semesters of covid, I noticed that they turned back to generate positive cash flows after interest payments, maybe with staffing downsizing, but not relying on handouts for this.

Then, following the vaccine passports roll out (which I disapprove on an ethical basis), I realised that the indoor part of the eateries would reopen for at least a long time,

increasing profitability again. Therefore, with a price near the bottom, I took some gains somewhere, and I got back in.

So now I describe a stock that is cheaper than when I first got in, It must be a great opportunity!

Poulaillon is a French very small cap, about 20 million euros. It reports only in French, and with PDF files. Sacrebleu !! I can already hear the silence in the room.

It has 3 main business lines:

1-Bakeries with eating in and takeaway.

Here we have various formats, some like cafes, some just like a bakery, some more like restaurants, A lot of the eating is sandwiches.

The locations are centered around Mulhouse and neighboring regions, In Alsace. It's very close to Germany and Switzerland, but all these town names in the below map are in France! What a diverse country it is.

Prior to covid they had opened some stores far away from the region, but they are closing them now due to costs or profitability. I think they will focus on a regional spread for now, for logistical synergies.

2-Food products b2b. (32% of revenue)

Here they sell the Moricete(TM) bread, a bread made with bretzel method, Moricete sandwiches. It goes to supermarkets, shops, highway shops, and pastries go for events, parties, companies.

They finished a bread production line expansion in Q1 2021.

They are expanding capacity

3-Mineral Water - 3% of revenue.

It is a new venture since about 2015, it is still losing money because they have not yet reached volume breakeven point. They also market the water in the restaurants a lot.

The problem is that the growth is quite low and it will take a few years to reach breakeven. However the losses are fully compensated by the two main divisions.

Financials:

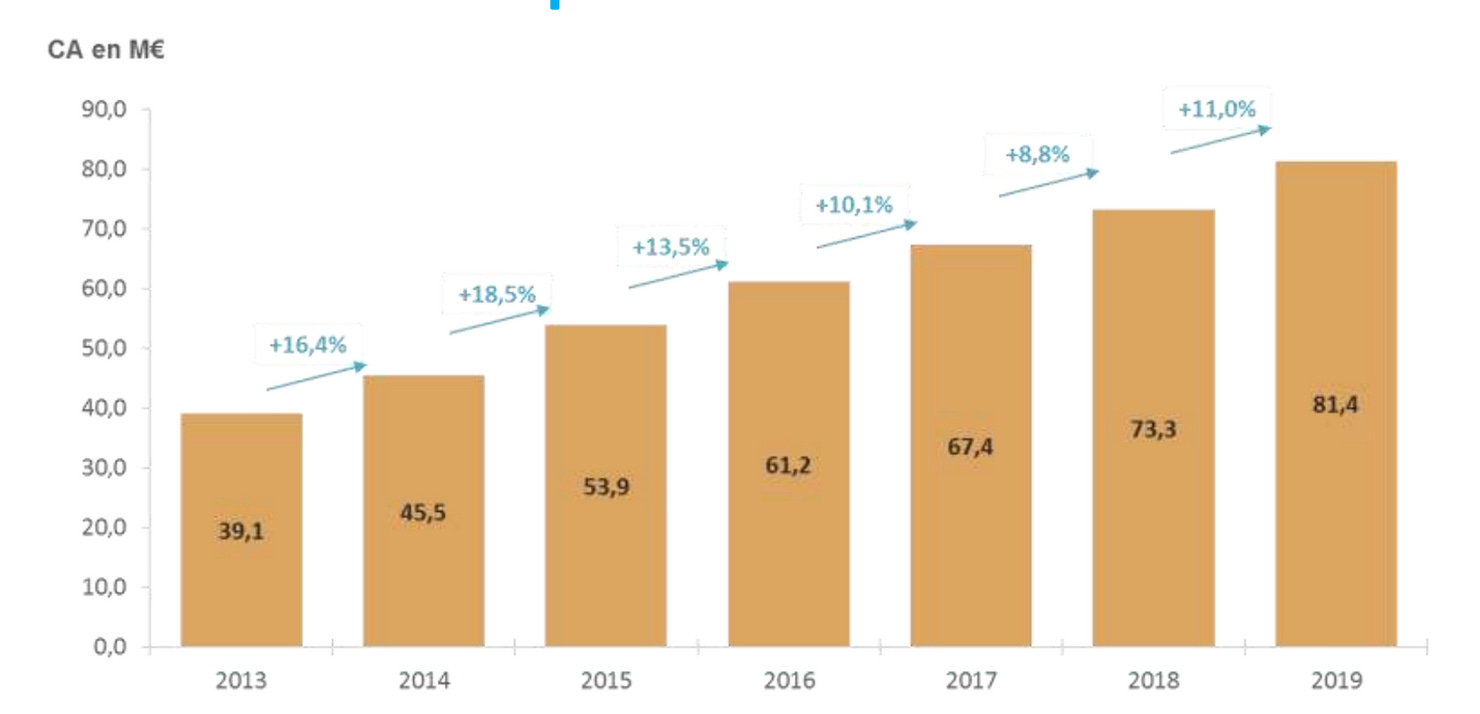

Steady growth in Revenue and Ebitda, and Cash flows during all the years until covid hit.

Restarting to growth in 2021.

Revenue growth.

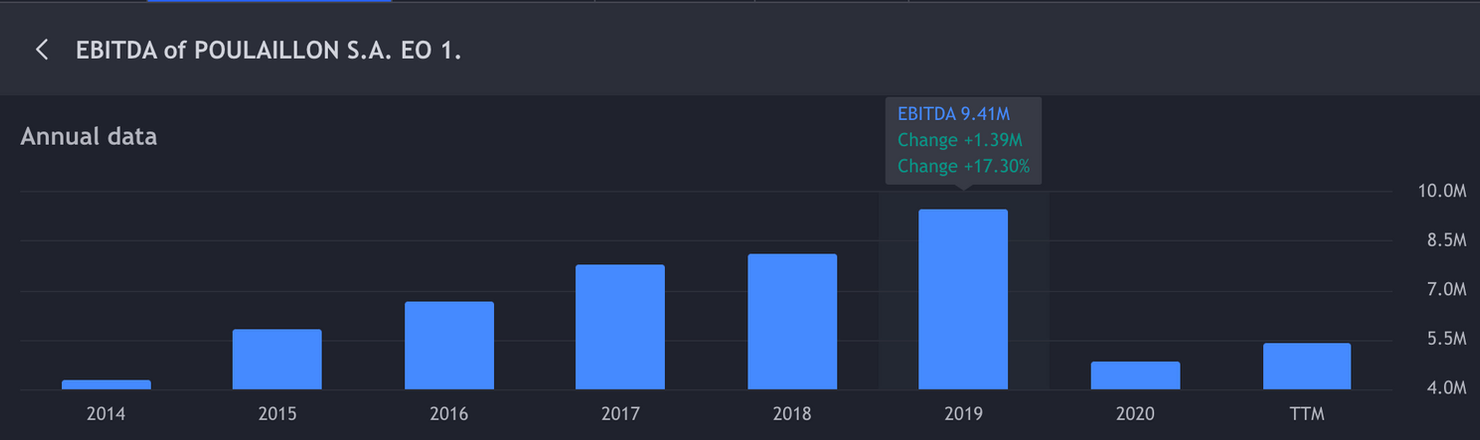

EBITDA:

(the TTM is outdated, it is now higher)

Valuation

All the financials are in French, so you have to believe me on these, and if you want to buy it, I suggest you get them translated first. Even in French they are not very easy, due to depreciation and exceptional items.

The company depreciates a lot, so the net result is not very relevant and we have to look at cash flow. That is one problem and an opportunity for French small caps investors because Frankly, a lot are limited financially and only look at net result.

The company invests in growth (new restaurants and factory lines) so we must look at operating cash flow, and not FCF.

the company communicates around EBITDA a lot. But it has some debt and therefore it is not the best indicator, while pretty good.

Market cap 23M.

2019 pre covid

EBITDA: 9M

Operating cash flow ex working capital: 7.2M

Last EBITDA 3.6M for H1 2021, or 7M anualised.

Operating cash flow ex working Capital: 4.2M. I think there is a 1 million exceptional result here, so about 3 millions or 6 millions annalised.

And that includes nearly 1 million of losses from water.

Price/Cash flow aka real earning power POST covid= 3.8

Price/Cash flow aka real earning power PRE covid= 3.2

At this price, you get a long term little compounding machine and a company whose products are close to my heart!

Bon App!

Update on H1 2022 calendar earnings. Sales up versus 2019 but profit and ebitda margins still lower than pre covid which is disappointing.

Got an update from management, mostly increase in staff costs due to job market (the company will do better in bad times), and delay in increasing prices corresponding from input inflation.

I received great feedback on maintenance capex, D&A, and leases since I published this article.

From the cash flow statement, we must deduct 1.5 millions of leases. I now learned how it works under the new accounting rules. Although some of these leases are investments because they are in a let to own scheme, It is better to simply remove 1.5 millions from the earnings power estimate.

For maintenance capex and D&A. Well at least for now, the investments detailed in the annual report are not maintenance, they are new stores, store expansions and new factory lines. I do not want to deduct these as a real cost.

In theory, maintenance capex equals to D&A-leases will be due in X years. In my opinion this is not a guarantee, and due to the growth capex, in that X years, even if that maintenance capex is due, the FCF will be much higher, because we will get : much much higher cash flow from ops Minus higher maintenance capex.

But I should also have estimated a small maintenance capex cost at minimum for the current year.

At the end the thesis is still intact, but it is not that cheap. it is still very cheap.

6 millions - 1.5 millions leases - 1 million estimate maintenance capex = 3.5 with covid

with vaccine passport now and reopening, I hope for 1-2 millions more cash flow or lets say 5.

market cap 23 millions

P/E=6.5

P/E with vaccine passport and partial reopening: 4.6 or 5 to average.

The feedback I received made me growth as an investor and it is very valuable to me. Thanks!