First Pacific - South East Asia at a double bargain

Updated: Oct 12 - Article reorg for clarity on Dec 18, but no new data added.

Introduction

First pacific is a holding company listed in Hong Kong.

Its particularity is that it has no business in Hong Kong or China.

It trades at a P/E ratio of 3.6 when I annualise the recurring profit. I think I must be wrong somewhere because it is way too cheap.

The NAV per share is 6.54 HKD and it trades at a 68% discount to NAV.

Its holdings are the three main holdings and a few smaller ones.

Indofoods: Noodles, agriculture and food mostly in Indonesia.

MPIC: Infrastructure in the Philippines

PLDT: Largest Telco in the Philippines

The smaller ones are Philex (gold mining) and a Power Plant in Singapore. It has a sugar company in the Philippines. They do minor contribution.

Analysis of the three main segments.

A-a few words on Indofoods:

Indofoods is 38% of Gross asset value.

I analysed/introduced Indofoods here

. It is a growing, dominant, extremely defensive food company at 8 PE ratio, 10 PE when I wrote the article, 8 now. Its worth 2.5 times this.

B-A few words on PLDT: Leading telco in the Philippines. It has a good track record of slowly growing revenues and results recently, despite new entrants in the market, and management is confident in the future. They do a lot of Capex to capture revenue opportunities, like 4G, 5G and the broadband/home business. Owns a majority stake in PayMaya, a still unprofitable fast growing Ewallet 40 million registered users. So, I read some analysis on risk of new competition, but they seem to still grow and be confident. It is a question mark. PayMaya is a long term positive.

C-A few words on MPIC: Diversified Philippines infrastructure holding company with hospitals, roads, water, rail, and more, listed and ran for shareholders return, The business saw reduced earnings from covid19, so its future earnings power is higher. It is under regulatory pressure like infrastructure business can be, but remains very defensive and pays a stable dividend. Metro Pacific Investments Corp trades at a PE of 8.5.

So here is a discount on the discount when we look at discount to NAV. Personally I prefer looking at P/E ratio rather than NAV, I like to look at my pro rata profit and remove market valuations which are sentiment based.

No signs of distress

Ok it must be indebted right, or have some hair?

No, there is some debt, but no big problem.

Here is the excerpt from the H1 Results:

CONTRIBUTION FROM OPERATIONS RISES 26% TO US$249.2 MLN.

RECURRING PROFIT UP 38% TO US$209.5 MLN, 10-YEAR HIGH.

NET PROFIT UP 80% TO US$181.0 MLN VS. US$100.6 MLN.

TURNOVER ON TRACK TO SET RECORD HIGH FOR FULL YEAR.

INTERIM DISTRIBUTION RAISED 29% TO 9.0 HK CENTS/SHARE.

ENTERING 12 TH CONSECUTIVE YEAR OF 25% MINIMUM PAYOUT RATIO

This is totally ridiculous. There is no other word. The stock has reacted well to this improvement since covid lows (where profits were impacted but not hugely), up from $1.50 HKD to $2.75 HKD (Dec 18-$2.92 HKD) , so it is not hated, but it has a long mountain to climb back.

Lets look at track record and management

-The company is controlled by Anthony Salim, and Salim group, one of Indonesia largest conglomerate.

- They raised capital in 2009 (lows at around $3 HKD, didn't look further, maybe they had excess debt. 1 for 5.

-They raised capital inn 2013 at $8,10 HKD a share. Maybe stock was overvalued or fairly valued. 1 for 8.

I see no problems with these raises. If the stock is cheap, it reduces risk and gives us a good signal to participate, if the stock is expensive, you just let them do it and use the cash.

B. Inner dealing in Indofood

He is not very liked by the local shareholder base due to inner dealings like last year when Indofoods CBP bought a company he controls, Pinehill, for $3 B USD. That could be a reason for the discounts on the companies he controls.

Indonesian tycoon Salim wins close shareholder vote on controversial $3 billion deal

By Alun John 3 MIN READ HONG KONG (Reuters) - Indonesian tycoon Anthony Salim narrowly won shareholder backing on Friday for a $3 billion takeover transaction between companies he controls, overcoming criticism about the deal’s valuation and questions about corporate governance.

Where the skeptics right to criticize? One year later, we have the proof below in the results of the subsidiary Indofoods CBP results, with nice revenue growth outside of Indonesia.

ICBP’S FIRST SEMESTER 2021 FINANCIAL RESULTS

• Consolidated net sales increased 22% to Rp28.20 trillion • Income from operations increased 36% to Rp6.36 trillion • Core profit increased 25% to Rp3.95 trillions

and its not just a recovery from a covid through, as last year, this business was strong.

CBP’S FIRST SEMESTER 2020 FINANCIAL RESULTS

• Consolidated net sales grew 4% to Rp23.05 trillion • Income from operations increased 22% to Rp4.68 trillion • Core profit increased 21% to Rp3.16 trillion

(First Pacific H1).

Indofood, the world’s largest maker of wheat instant noodles and the biggest food company listed in Indonesia, saw its contribution rise 31% to a record high US$122.9 million versus US$93.8 million a year earlier on surging growth in its noodles business following the acquisition of Pinehill Company Limited (“Pinehill”) in end-August 2020, a noodle maker based in Africa, the Middle East and Southeast Europe, and double-digit external sales growth at all four Indofood businesses – Consumer Branded Products, the Bogasari flour and pasta division, Agribusiness, and Distribution.

These results are a smash, They trickled into Indofoods and First Pacific. Therefore the acquisition and related party transaction was at least not bad for shareholders, and most likely very good.

On alignment with shareholders, First Pacific is actively buying back shares, and Indofoods pays a good dividend.

By owning both, I am covering two positions of the group structure, in case one entity gets a better treatment, and also for diversification.

-Acquisitions:

-First Pacific had some badly timed acquisitions of Natural resources companies in 2008, 2010, 2013. After this we had a natural resources down cycle.

-First Pacific bought Australian consumer goods company Goodman Fielder in 2015, sold it cheaper in 2019, because the debt ratio of the holding company was a bit too high.

-so we can say that the prior track record was not very good.

-A long time ago, it made good investments: 1998–2000: Acquired PLDT in the Philippines and Indofood in Indonesia.

Refocus on core holdings

The good news is that First Pacific recognised errors in past acquisitions and has decided to focus on mostly growing it's 3 core holdings.

-Indofoods

-PLDT

-MPIC

Together these 3 Holdings are 90% of NAV, 10% is natural resources. Natural resources rebounded in 2021 with the gold producer Philex Mining positive results.

Leverage: Net Debt to GAV ratio at 27%, Gearing at 80%Net Debt to GAV ratio at 27%, Gearing at 80%. It is a bit high, but they have no problems refinancing it and I am expecting GAV to grow a lot with EM sentiment risk on shift once covid is business as usual, and it is becoming like this.

Summary:

In the end, we got an company that made some mistakes in its acquisitions in the past, but did survive and come out stronger, and is now an incredibly cheap company with very good quality assets of a defensive nature, where the management is confident about the future (increased dividends). I hold a large position, I have held it for a few years now and I am only slightly positive + good dividends.

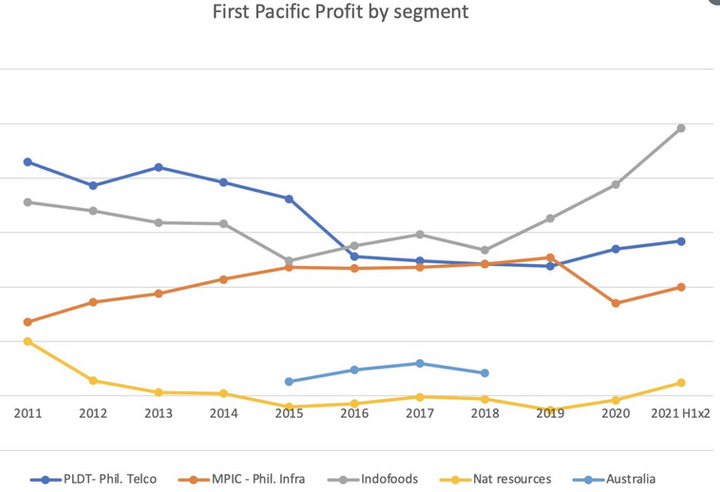

Appendix: Past underperformance reasons

Notes I left on twitter to explain past underperformance

1-PLDT suffered from competition (2013-2016) and switch to data vs voice and SMS before stabilising

2-Natural resources went to the cave

3-Indofoods results hit by Rupiah depreciation (2011-2015)

4-MPIC was steady until Covid

5-doubtfull cap allocation (Australia)

6-debt

Conclusion:

-Indofoods and MPIC should be able to lift the company going forward despite PLDT, even if PLDT declines like in the past. PLDT could bring value from PayMaya fintech.

-MPIC yet to recover toll road and passengers numbers post covid.