FAT PITCH value: Real estate as a service

IWG PLC

Your writer used to own as a value investor the Japanese conglomerate Softbank.

Softbank, controlled by Masa Son, comprised on a stake in Alibaba, Sprint, Yahoo Japan, Softbank Japan (A telecoms company). It used to and still trades at a large discount to NAV.

Masa Son is often ridiculed by value investors for buying some dog walker app for maybe 4 billion USD or for buying Wework at 47 billion USD.

Masa Son on the other hand was a visionary in building Yahoo Japan, in building the Japanese telecom carrier with a vision for the Iphone before there was an Iphone.

He also bought into Alibaba when it was a startup, with a bit of luck and instinct. Recently he had a great vision on AI and wanted to merge ARM with NVIDIA and effectively own a large stake in NVIDIA. I really think that Masa Son has amazing vision, but sometimes overpays or sometimes have bets that don’t work, which is part of venture and growth investing.

Masa Son invested and burned billions of dollars in WeWork, the company that put coworking on the forefront of the coworking revolution. Was he stupid? No, and yes, but not totally. Burning the billions he did. However the vision and comments he had on coworking and on the Wework model were not stupid, and still stand in my opinion.

-Cost reduction for companies, flexibility.

-employes satisfaction.

-Simplicity for companies.

-Expertise by WeWork not matched by small and medium businesses.

-Network effect similar to a marketplace.

WeWork was ultra aggressive in terms of leases, capital investment, and debt, and as a result is distressed right now and the equity could turn to a zero. Softbank could bail it out and dilute it further. Today it is worth 120 million euros, very cheap for this brand, but a wall of debt and losses awaits the company.

On the other Hand, there is financially solid company with a net debt/ebitda of 1.6 (I do not include leases in debt and lease costs in ebitda. I blame this IFRS rule). It is the world leader in coworking, trading at a very reasonable valuation.

This IWG PLC, or International working group.

IWG owns Regus, the coworking leader as well as many other brands, acquired over the years.

It is still run by it’s founder, survived many downturns and that brings a wealth of experience for the company.

Business overview

The basic business is that IWG leases some office building and then sells flexible office space or coworking to individual and corporate clients, in the form of monthly payments for access.

There are however many brands and also a marketplace business.

The most interesting part of the core business is the way the locations are operated.

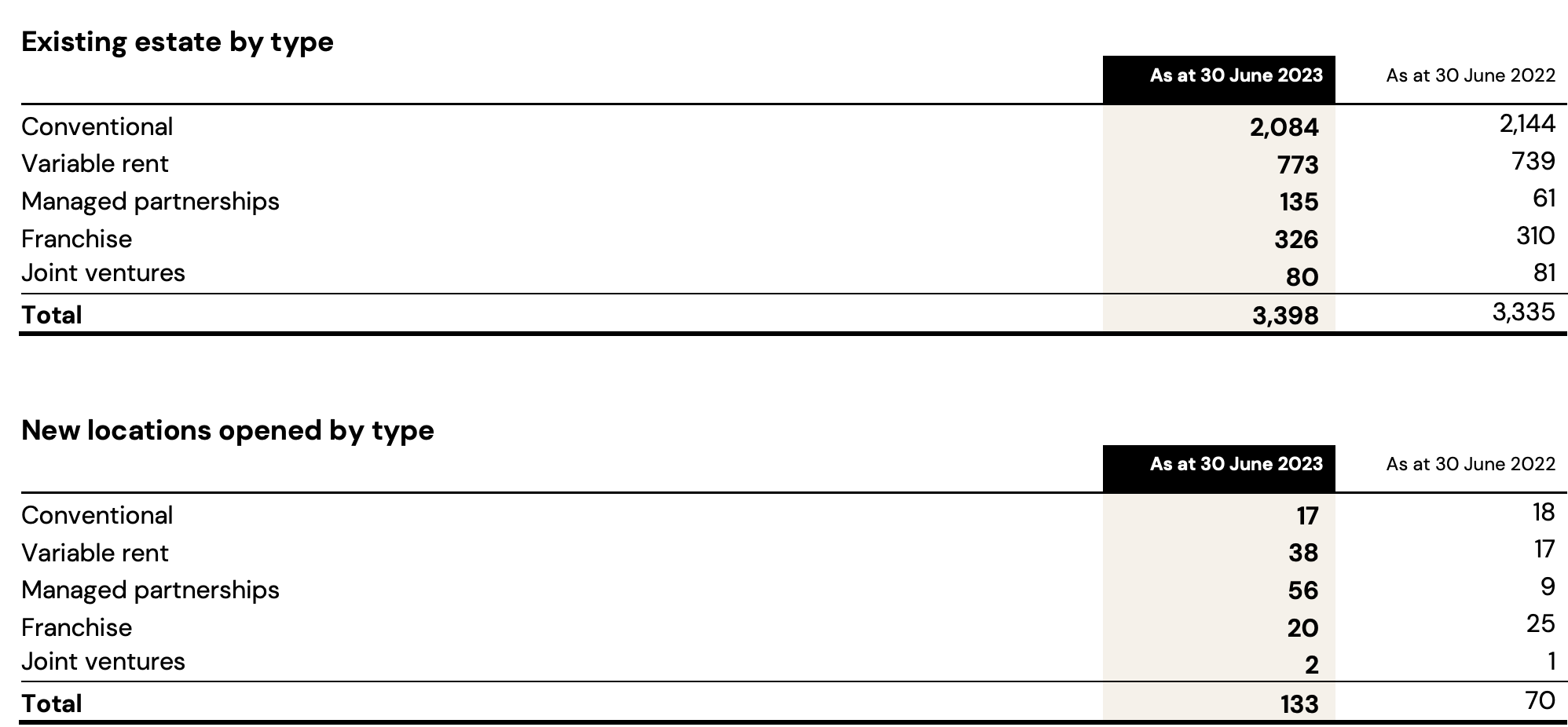

You got leases taken by IWG (“conventional”) and Franchise business. In The Franchise business, also called Capital light, IWG puts no capital down and collects franchise fees in exchange for the company branding , relations, IT and know how.

The conventional business carries risks if the money it can extract from the coworking is less then the rent it pays, as it can happen in a downturn. A good protection is that IWG has perfected and derisked the model over the years: the subsidiaries are ring fenced and the leases in one location cannot affect the parent company if the location entity cannot pay them.

A good summary is this table.

For new deals signed, the company is shifting the efforts on capital light business. Note a delay between centre openings and new deals signed, which will take effect in 2024.

The reporting is not clear, and Managed partnership is a form of capital light as well as franchise. Variable rent is not described clearly. I would assume that it goes up or down based on IWG revenue in order to adjust in line with it.

The company offers the following to building owners as part of the Franchise agreement (https://www.iwgplc.com/en-gb/develop-a-location)

“You’ll benefit from immediate sales and marketing, design and fit-out support, rapid occupancy, with no long void periods, and a whole host of other benefits.”

Here is what the company has to say in the H1 report about the growth strategy.

Our focus has been and will continue to be on expansion through partnerships. Less than 15% of deals we have signed this year are company-owned (comprises of owned buildings, fully conventional and/or variable leases). As a result, we are continuing to improve the quality of our portfolio as we grow our global network. We are well positioned to continue to grow given that we still have 26.3% of centre capacity remaining which we can use to grow revenues at low marginal cost with minimal further investment.

What is interesting is that 382 out of 400 deals signed in H1 2023 are capital light.

From a geographical point of view, it comes from EMEA 49%, America 40% and Asia for the rest.

Digital business:

Then we have the Digital or “Worka” Revenue.

These are basically digital platforms like EasyOffices.com to book workspaces.

In 2022, IWG bought the Instant Group, which operates instantoffices.com, then proceeded in merging its digital assets with Instant Group.

https://coworkinginsights.com/iwg-announces-merger-of-digital-assets-with-the-instant-group/

“The Instant business has grown by 25% Compound Annual Growth Rate in the last 5 years, has award winning digital marketing capabilities and provides solutions to 45% of the FTSE 100 and 40% of the S&P 500.”

The company says that it will develop its own app, Worka, to bring all it’s locations and brands as an easy to book marketplace, with over 30,000 locations. However to this date, nothing has been released.

More surprising, 3 out of the 4 brands listed under Worka in the annual report 2022 are now dead URLS. There is something disappointing but probably a focus on Worka and Instantoffices.com

Worse, the annual report is absolutely TERRIBLE at explaining what the Instant Group is and what worka is. Instantoffices.com is not even mentioned in the annual report. The Instant Group also presents itself as a consulting solution on it’s website, but there is no details on the annual report.

In terms of profitability, H1 2023 saw 35% EBITDA growth to £62m (H1 2022: £43m), or 31% of company EBITDA. IWG is very much a tech company.

Market

IWG predicts that it will grow by 600% by 2030.

According to a report from The Business Research Co., a market research and intelligence firm, the global coworking industry is likely to see a 17% annual growth, reaching more than $30 billion in 2026.

According to CommercialEdge, shared space has an overall market penetration of 1.7% of office space, with the majority of coworking locations concentrated in the top markets. Manhattan has the highest volume of flexible office spaces, with 291 locations amounting to 13.8 million square feet, representing 2.8% of stock.

Source: https://www.yardikube.com/blog/demand-for-flex-continues-to-rise/

These are enormous numbers so there is potential.

Valuation:

Using the information chart below on the cash flow, I have calculated a 95 million pounds cash flow for H1, or about 190 million for the whole year. This is close to the company estimate of 109 million for H1 2023. The working capital was only +10 million positive, making 170 million for the whole year.

This puts the company on a price to real earnings of 7.5 with the current market capitalisation of 1.28 Billion pounds. This is cheap.

Note that the company has the full cash flow statement that is hard to understand because of the IFRS 16 and lease treatment, giving a huge operating cash flow of 717 million pounds before deducting lease payments.

Another way to look at the valuation is looking at Adjusted EBITDA that deducts leases, which is 198 million pounds for the half, less 95 million for Tax & Finance costs and Maintenance capex (chart above), gives us about 100 million of earning power for the half, or 200 for the year, excluding FX movements and Other.

This again puts us in the 6-7 times.

Which in this market is nothing, because many opportunities trade at this valuation.. but it is interesting.

Opportunities:

Increase in occupancy (73% at the end of 2022)

Increase in trends of coworking and flexible working.

Capital returns as debt gets paid down.

Risks:

Recession that will reduce the rates and the occupancy.

But it could increase occupancy if the recession make many business downsize.

Conclusion

This is just a quick overview:

For full thesis I recommend the interviews of Sven Lorenz:

and with Yaron Naymark, both on the Yet another value podcast. They know IWG much more than me.

Note: this is not financial advice, but my opinion on the company. Anyone should do their own due diligence to confirm a company thesis presented and form their independent opinion.

How is this a fat pitch? You repeatedly mentioned about the opacity of the annual report & the difficulty to calculate certain metrics. If anything, this is an easy pass.

This writeup, unlike your previous ones, is pretty disappointing.

Interesting revisit. Hard times currently. Thus, how likely (true) maintenance Capex is as low as presented and designated growth Capex does not include a good portion of maintenance Capex?