I own a position, this is not investment advice.

Bastide is a French small cap that has a real track record of compounding in the medical services sector.

Here is the last 12 years track record of 18.5% EBIT CAGR.

History

It started out of this classic Renault 4L in 1977.

According to the company’s website, Guy Bastide, a pharmacist from Nimes, started near a mining basin in the nearby city of Ales, Southern France, where coal miners were often affected by a respiratory disease.

At the hospital, patients were mentally suffering in this environment out of the home, missing their old home. Home treatment was recently allowed and the miners would prefer this home treatment surrounded by their families, and get better results. Guy bastide would drive his “4L” on the roads to deliver oxygen bottles to the miners in their homes.

It was not until 1983 that Bastide saw its second agency in Ales. Four years later, another one was opened, then it accelerated strongly, expanding in the same region.

Today the company is still based in Nimes and has not moved to Paris or a main city.

In 1997, the company went for a listing in the stock exchange. Guy Bastide found that the geographic expansion was too slow, and he did not have enough resources.

With more resources, the company started to acquire other companies and expand the range of home medical services (other therapies). It started to reach a scale where it was a partner of choice at the national level for these services.

In 2005, Vincent Bastide, the son, took commands. To accelerate growth, franchises were opened.

In 2018 the group started venturing abroad, with acquisitions in Spain, the UK, Switzerland, Belgium.

The Bastide family owns 55% of the shares. The company put in place employees stock programs.

Business

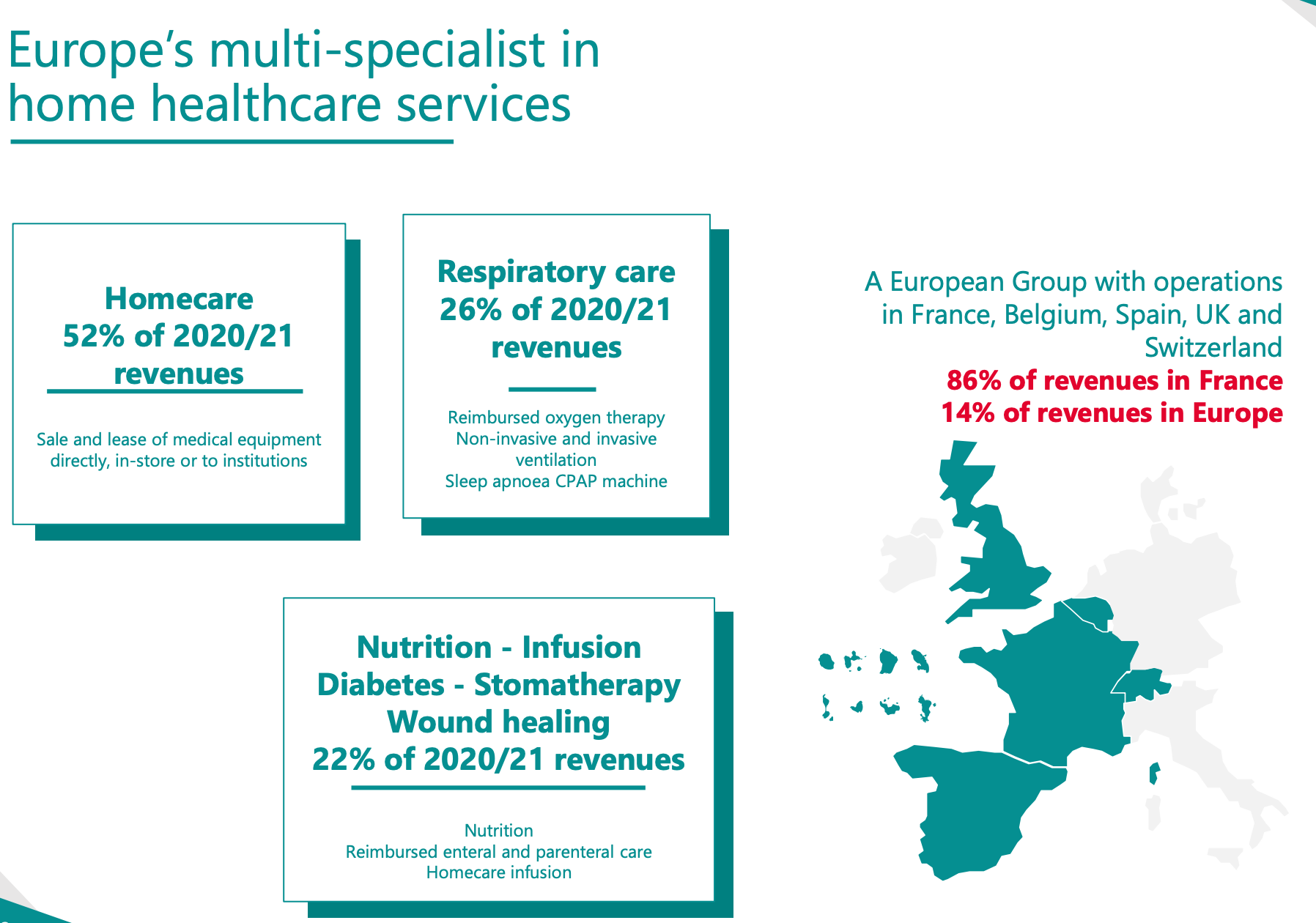

The investors presentation is clear. I will use it to describe the business.

What is interesting, is that the home care division includes an ecommerce division with 26 million euros of sales last year, boosted it is true by the pandemic, from 11 million the year before.

Homecare: The leased or bought products are special chairs or beds or wheelchairs for elderly people to help them live better. The products when bought by Bastide, are under capex because they are large. When the company is growing, they are profitable growth investments. When it is a maintenance replacement, this is maintenance capex to be deducted from operating cash flow. However we will see later that this is complicated. Most of these products are refunded by the French social security

Respiratory and other segments have services where the social security is refunding/covering for the customer. Due to this, the company has to accept the price that social security pays. Lately, there have been many price reductions.

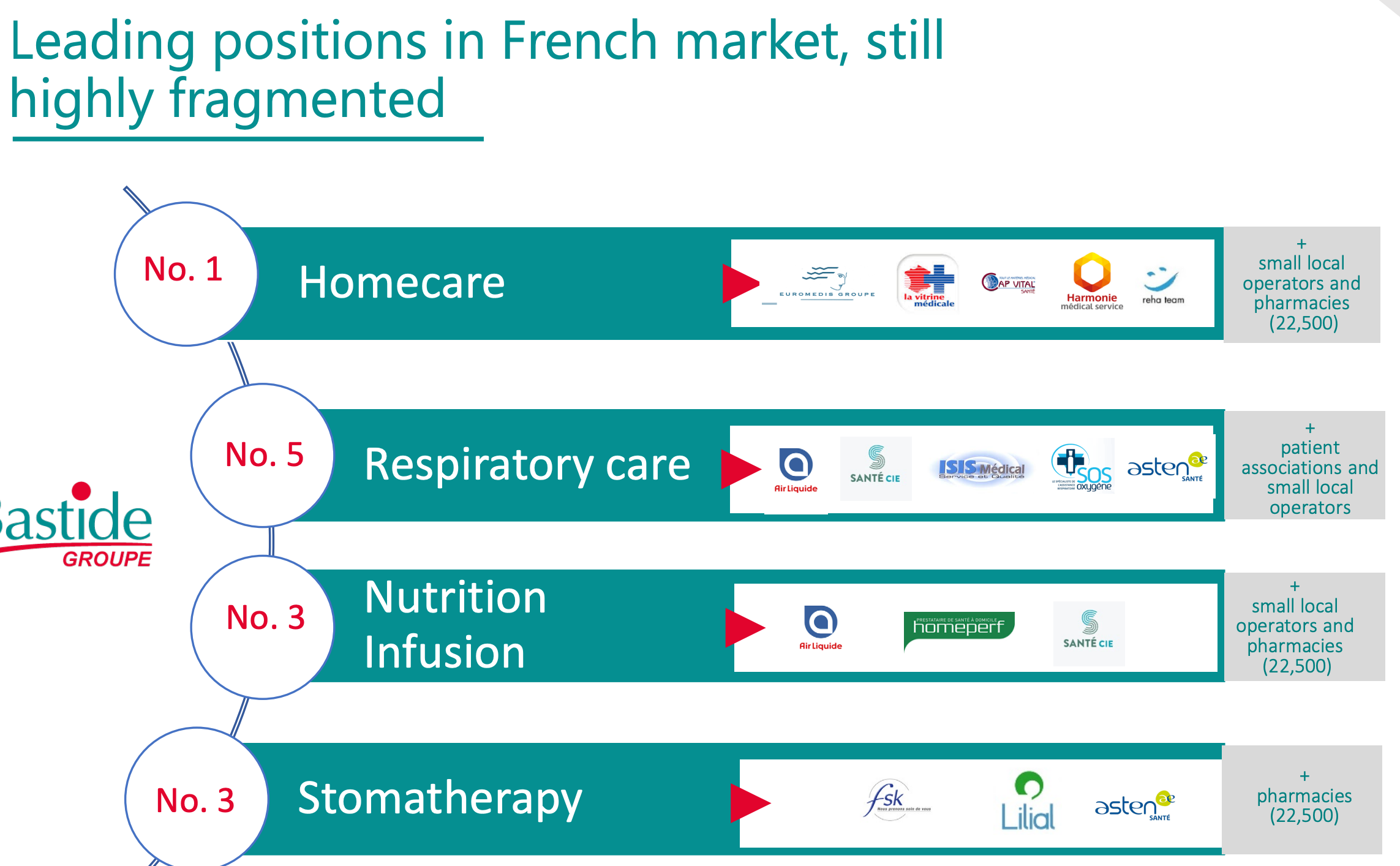

Competitive landscape:

A big characteristic of home medical services is that there are many very small companies to be acquired.

But there are also large players in Respiratory and Nutrition, notably Air Liquide, a multinational with a 74B market cap.

Growth by acquisitions

Bastide reinvests nearly all their cash flow into acquisitions. The fact that the market is fragmented allows for plenty of small acquisitions, which is a very profitable strategy. The company uses leverage to constantly acquire. It is a roll up. It was a roll up before the word roll up existed! It did over 50 acquisitions in the past 10 years.

In the last financial year, they did 8 acquisitions for a yearly revenue of 21 million euros. They do not disclose the profits, but we can look at the cash flow statement to get an idea of the price paid.

So could be 16.5 millions for 21 millions of revenue

If we consider the recent Ebit margin of 8.3% as a base, they paid a 10X Ebit multiple. That is using assumptions thought, but that is what we have.

Next, on January 5, 2022, they announced two acquisitions, the main one below, which is a great further push into ecommerce.

The acquisition strategy, the large number of targets plus organic growth allows Bastide to produce regular and fast growth.

Fueled by debt

The company keeps acquiring and uses debt to grow faster. Its current Net “borrowings to EBITDA*” is a ratio of 3.2. The debt is below 3.5 permitted by bank covenants (with a possible overshoot to 4). They maintain in constantly in range as they keep acquiring.

Business trends

Organic Growth (ex acquisitions).

2021 Q1=-0,1% (tough comps)

2021: +13.6% (covid)

2020: +13.7% (covid)

2019: +6.8%

2018: +5.4%

2017: +7%

The UK region: They bought Baywater and Intus in 2017 in the UK, which had combined revenues of 28.5 ME in 2017. In 2019 it grew to 30,4 M€ for Baywater, in 2020 34 M€, and 2021 34.9 M€. As the company bid for new regions and renewals, the prices were from a lower base. In 2021 the company incurred extra costs to increase the growth in the UK.

Prospects: They aim to grow revenue to 500 millions with acquisitions for this year and beat the operating margin of 8.3% for the past year. The plan for 2022 is to Return to growth in the UK and strong potential in Spain. In theory they will reach 42m in EBIT. This is despite hard comparable base due to covid organic growth in the past two years for Covid.

Risks - Regulatory price reductions:

This affects a large part of the business, that have services or prices covered by social security.

2016: 0.35 ME revenue impact

2017; no info

2018-2019: extra 4.6M capex, plus lower prices: -2,7ME Ebit impact

2020: 2.6 ME revenue impact

2021: 5 ME revenue impact. This affected the UK and global margin went down “Decline in contribution in the United Kingdom Impact of the price reduction under new 10-year contracts New 10-year economic cycle with an expected gradual recovery in margins (volume and savings effects)”

2022: Estimated negative impact of around €4m on 2021-2022 revenues

The company is usually able to offset the price reductions very well through scale:

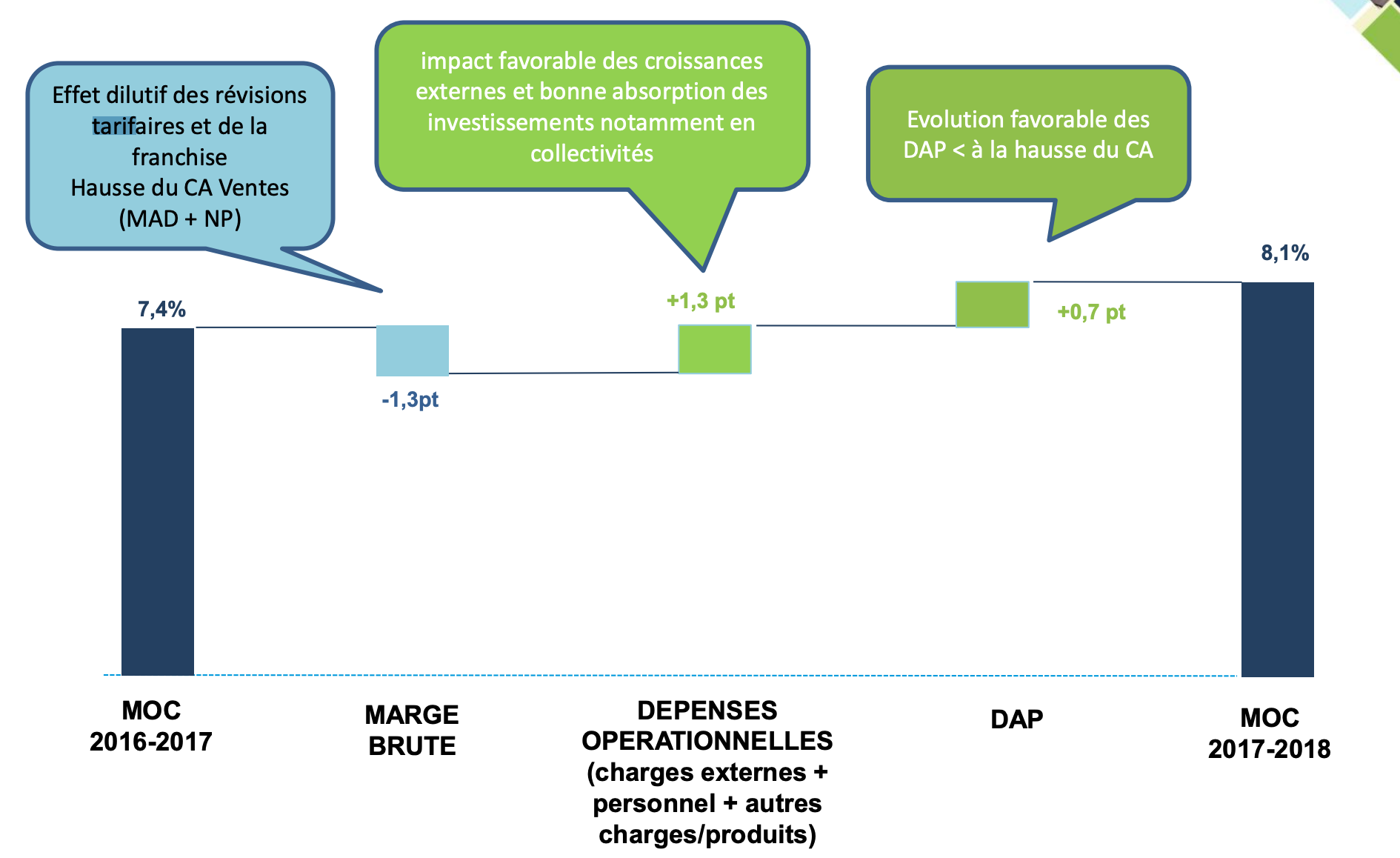

MOC is Marge Operationelle Courante or Operating Margin

-1.3 points due to prices and franchises. +1.3 points due to positive impact from acquisitions and good absorption of investments, +0,7 points D&A growing slower than revenue.

(2018)

2020 -0,1 points for prices, -0.6 points for new growth initatives and +0,6 points for product mix.

The company says “proven model to absorb the impact of price reductions”. I do not really like businesses affected by price reductions. But the benefit of the doubt has to be given to Bastide because they have historical performance to back it up and they are optimistic about the prospects. They explain that they absorb price reduction with procurement centralisation and volume, as well as administrative efficiency. There is a limit to this because the government needs investment in organic growth in homecare to save on hospitals costs.

FINANCIALS

Valuation 1=Net profit

The company made a profit of 14.3 million last year, on a market cap of 368 millions. This makes a PE of 25.7 Definitively not cheap.

But there are non recurring expenses by year:

Looking at the annual report, they are mostly non cash or donations.

Translated, it gives this.

Adding back the things in green:

= €4480M for 2021, I get 19.2m Net profit, and Adjusted PE ratio of 19

=€1401M for 2020, I get 14m Net profit. And net profit growth is then 37 from 2020 to 2021.

Valuation 2=FCF

The real operating cash flow is 54 million euros when we do not add back leases. After this, they do 46 million euros of capex. The FCF left is only 8 million Euros. This must be because of growth capex to support the organic growth.

Ex Working Capital and Ex acquisitions:

FCF 2019= 9m

FCF 2020= 6m

FCF 2021= 8m

So we get a P/FCF of 46 which is very expensive. We have to consider that there is many organic growth included in the capex.

CAPEX 2019=34m. Capex/revenues=10%

CAPEX 2020=40m Capex/revenues=10%

CAPEX 2021=49m Capex/revenues=12%.

Looking at the notes, most of the capex is tools and technical installations for 39 millions. The D&A is lower than this at 28 millions. So the company has less FCF than net income for this.

In the text below from a old earnings release, the company makes it clear that capex is fueling organic growth.

Ces flux couvrent largement les investissements opérationnels de l’exercice (hors croissance externe) qui s’élèvent à 34,8 M€ (dont 4,6 M€ ponctuels sur les appareils pour l’apnée du sommeil). Le Groupe démontre sa capacité à autofinancer sa croissance organique.

The D&A period on rented medical equipment is 14 years, and they increased it to 14 years after setting up a maintenance unit. It does not seem aggressive but more appropriate to the reality of the assets duration.

Conclusion

I will not use EV/EBITDA or EV/EBIT as I do not really like these metrics (Same as Berkshire) which do not reflect economic ownership, capex or taxes, and the business is capex intensive.

I would not use FCF or the cash flow statement to value Bastide, there are too many growth investments and it is too complex. That was my error when I first bought it.

A good error because I already doubled my money :)

Now I will use the adjusted EPS.

If the company keeps compounding at the average of 18.5% the EBIT, in 10 years, adjusted net profit will be €105m. Let’s be pessimistic and say €80m.

Growth will then maybe slow down to 15% a year and the adjusted PE will be 20. It should be valued higher but lets keep it at 20 with maybe low level of communication on the adjusted PE.

Pessimistic scenario

Market cap would be 1600m versus 368m on a very conservative valuation. The CAGR will be nearly 15.8%.

Normal scenario

the Adjusted net profit will be €105m, and the PE will be 25, which is fair for such a growth machine.

Market cap would be 2625 versus 368 now or a 21.7% CAGR.

The business and company is very defensive in the growing market of healthcare. The company pays a little dividend. It seems able to compensate for price reductions by using scale and procurement savings. After publishing the article in the French Substack, I got some good feedback on Inflation risk from the local investors. It is a risk if costs (wages, products) increase a lot but prices are capped by the government. I think that the margins should be somewhat protected because the governments need home care to develop with organic growth in order to save money on hospital care.

I have it in the portfolio because the company is well managed and not too expensive, and defensive in a recession. I could swap if I find a safer equivalent CAGR if bastide share price rises a lot.

Analyst note:

https://www.lerevenu.com/bourse/bourse-5-actions-acheter-en-ce-debut-2022-selon-portzamparc objective 58 Euros.

Are you adding at current prices? It seems it has been caught in the pharma malaise!