Annual 2023 portfolio letter

Hello everyone,

I did well again in 2023, not exceptionally well with 14%, but I think that we can call the year good when we are over 10%. What was cool is that last year I did not lose money as well, even made some, so the portfolio is cruising, despite a terrible environment for value.

I had my share of bad performers, mostly suffering from high rates in financial services like Intrum or some subprime lenders and a Reit, as well as leveraged company Bastide le Confort, but they had a low impact overall. I had a bigger share of excellent and cheap companies not moving up, stuck in limbo land. This is why I am very optimistic for the future.

I said in recent letters that I would stop selling positions. I did only one sale in the quarter, and have zero planned. Investing has become more philosophical, more long term, now that covid value dislocations are over. As the portfolio is starting to reach a decent size for me, I feel more scared to do big changes and prefer to let it grow slowly but surely.

It feels so much better to operate like this, and I get closer to the essence of investing. If a company is not doing well this year, no big deal, it will shine in another environment next year. If a company is doing well this year, perfect, it compensates for the rest. If the stock price runs very high, I know that it will digest or go back down in the future, and if a company is too depressed, I know it will come back. I don’t feel richer or poorer in both cases.

The portfolio is set to spit even more dividends in 2024, as many companies are reaching their leverage target. It gives me more reinvestment opportunities and more chances to become independent one day. It grounds me to the realities of the underlying businesses more than stock prices. It is also great to see holdings with the capital returns to shareholder phase entering maximum force in 2023-2024.

The case for dumb value.

Growth investing is complex and difficult. It requires amazing analytical skills and foresight. Ability to differentiate a good business with great ROIC from a business having a short time boost or a moat under future pressure.

Good growth investors will do very well in the next decade. No doubt about that. I also have some growth companies. But many people think that they are good growth investors until they fall. Growth traps hit harder than value traps. People who own growth traps (20+ PE and stagnating profits) will get bad results.

Themes that worked changed brutally in the past years between Nasdaq growth and value. My sentiment and the data makes me think that it’s about to switch brutally towards value and EMs, while the few growth companies that can thrive in any environment will be doing ok. I had the same sentiment about value vs growth in 2021.

The pendulum switched again towards growth in 2023, and there is so much value in cheap stocks that I think that it is unnecessary to go for the fairly valued great companies.

Since the 2008 crisis and 2020, value stocks (see for example Arcelor Mittal, Bank of Ireland, Repsol, Petrobras, CK Hutchison, Fiat/Stellantis, Cenovus Energy) have reinforced their balance sheet greatly. They were over exposed, over leveraged and with over ambitious strategies in 2008 and sometimes also in 2020.

They have been tightening belts, closing under-performing assets and paying down debt since. Many are now hitting the dividend and buyback buttons hard.

So, lately, there is not much thinking to do. Just get dumb and get dumb value, at least for a portion of your holdings.

Favour companies that combine dividends and buybacks, or dividends for EMs. The energy/EM space is pretty good for that. That will provide good returns from yields alone.

I think that after this letter, I will make shorter letters focusing on the portfolio. The growth to value imbalance will no longer be extreme like now and there will be nothing of such nature to mention. But yes, a lot of companies in the US are terribly overvalued again like they were in 2021.

Performance details

I have calculated an average of my ideas published and they returned about 5% versus 12% for the SP500 at the same time, with some deep value ideas and financials not performing at all. So it is underperforming.

My portfolio did better, because of weighting, reinforcements, and other stocks not written up directly like Kaspi, IMS or Fairfax, mentioned in my updates.

Since 2019 when I moved abroad and opened this brokerage account, I averaged 12.5% versus 15.3% for the SP500. An awesome result for the SP500.

I think that, looking at the differences in valuations, value and international will probably crush the SP500 from now on. But, as long as I continue to quietly do over 10% a year, I am satisfied. If the SP500 does over 15% a year from now for ever, good for the people. I highly doubt it. My current earnings yield is probably high single digit, offering a good floor.

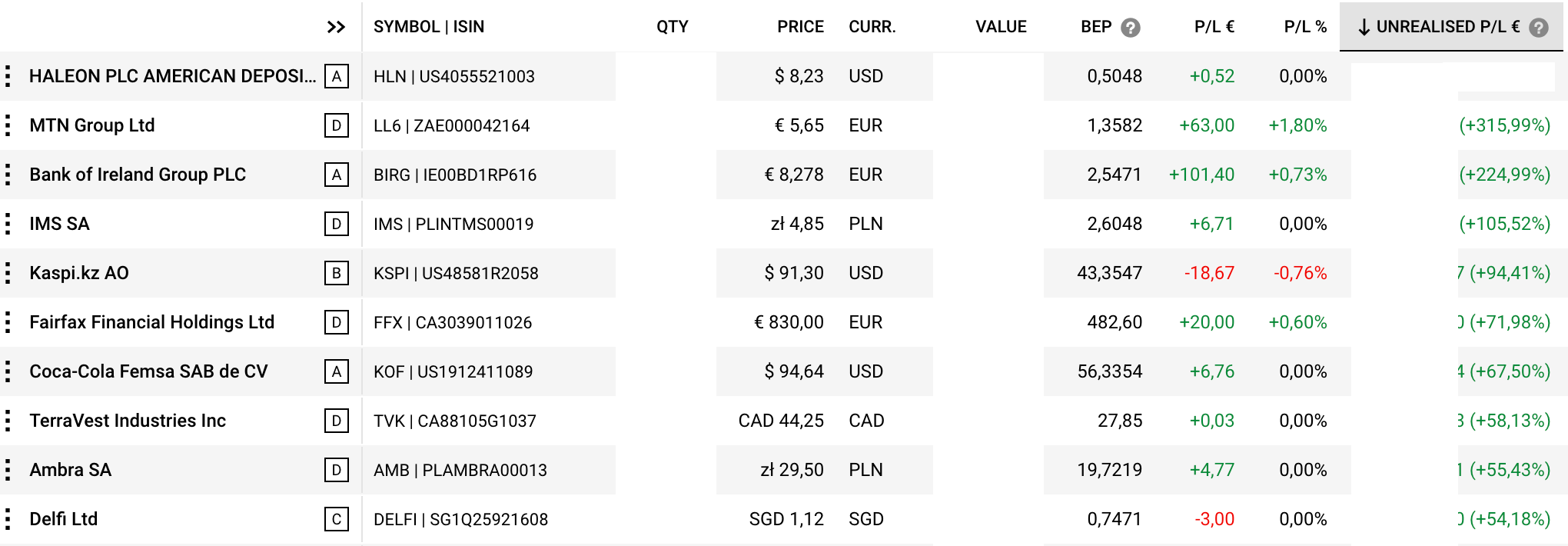

Significant performers ex dividends: (Haleon is a spin off to be ignored where I don’t have a significant profit).

Covid lows buys MTN Group and Bank of Ireland remain unbeaten. For these stocks I am in dividend extraction mode and I expect larger payouts in 2024.

The rest is mostly high quality stocks (IMS is a sensory and audio marketing company), Ambra a beverage company. These are two Polish companies.

Coca Cola Femsa and MTN show that buying EMs at a good time pays off. Delfi is an

idea, another EM stock at good prices.Now the worst performers ex dividends, where I think future value will bounce back.

Some stocks linked to Japan smalls (hated), Leverage (hated), the wrong EMs (Bangladesh) and DMs with sleepy management in China (CK Hutchison - UK).

For some reason, the losses are much less than the gains in absolute amounts, that is a great thing about investing.

Full portfolio below with a summary of each idea in the premium section:

Subscribing gets you

15 more unique ideas

Full portfolio with diversified 50+ mostly EM/small value ideas.

Monthly watchlist and ideas updates

Watchtlists in Koyfin with over 200 Emerging and Hidden champions stocks (free with Koyfin)